Can I Borrow Against My Stocks Without Selling in 2026?

Can I borrow against my stocks? Goat Funded Trader explains securities-based lending options, rates, and risks to unlock portfolio value in 2026.

.png)

Successful investors often face a common dilemma: needing immediate cash while holding valuable stock positions they don't want to sell. Liquidating investments to access funds means missing out on future gains and potentially triggering unwanted tax consequences. Securities-based lending offers a solution by allowing investors to borrow against the value of their portfolios while keeping their positions intact and continuing to benefit from market appreciation.

Traditional margin loans and portfolio credit lines provide one option, though many traders encounter restrictive requirements or unfavorable terms from conventional brokers. Rather than borrowing against personal holdings, funded trading accounts offer an alternative way to access capital and expand trading opportunities through a prop firm.

Summary

- Securities-based lending typically allows investors to borrow 50% to 70% of their portfolio value without selling shares, but this strategy requires substantial existing wealth to access. Most lenders set minimum portfolio thresholds between $100,000 and $250,000, meaning the tool only works for investors who have already accumulated significant assets. That creates a fundamental barrier: you need capital to access capital.

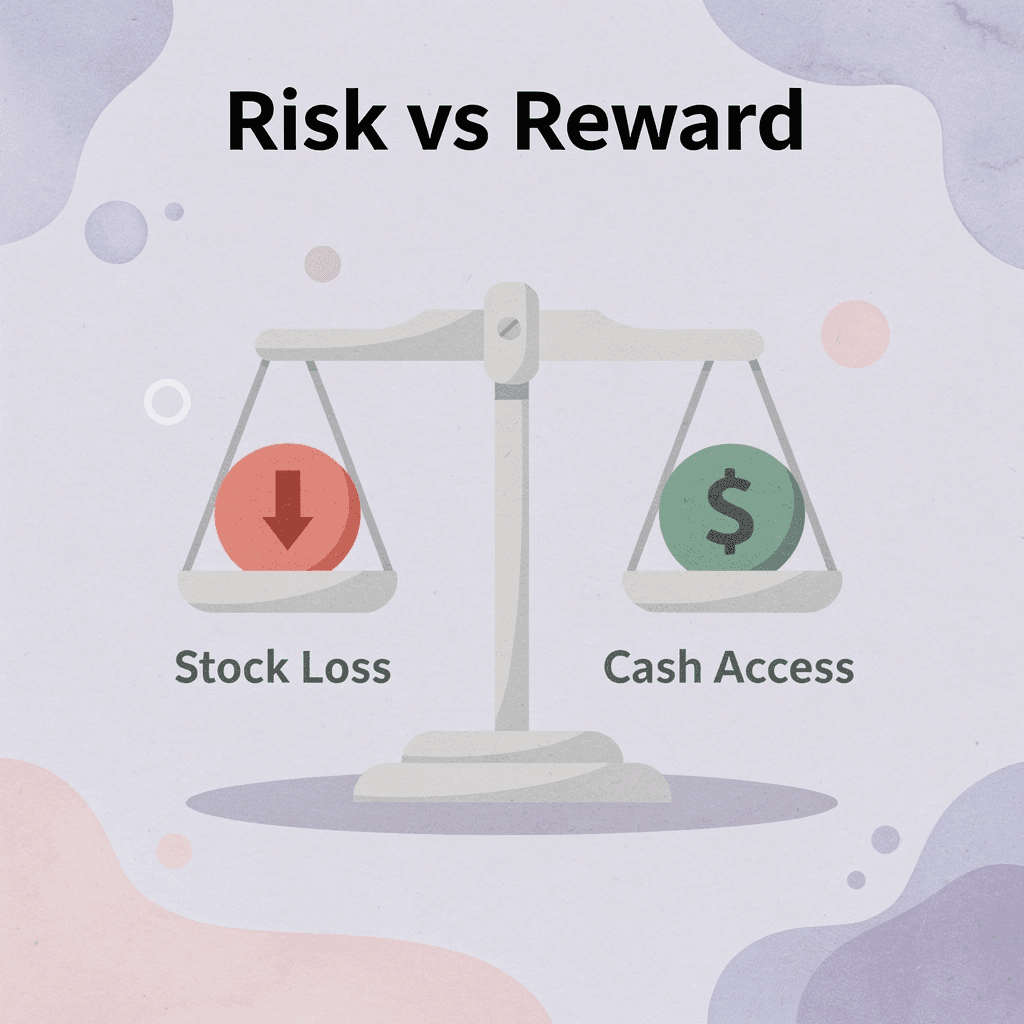

- Market volatility creates forced liquidation risk that borrowers cannot fully control. A 20% portfolio decline can push a comfortable 40% loan-to-value ratio to a dangerous 50% overnight, triggering margin calls that demand cash infusions within 24 to 48 hours. Missing that deadline means automatic liquidation of your holdings at depressed prices, often locking in losses precisely when recovery might be near and triggering capital gains taxes that can reach 30% on appreciated positions.

- Interest costs on securities-based loans range from 4% to 8%, floating with benchmark rates, so carrying costs rise when markets become unstable. These charges accumulate regardless of trading performance, draining returns and compounding over time. Borrowers pay for access to capital whether they generate profits or not, and variable rates eliminate predictability in long-term planning.

- Diversification across sectors and asset classes does not eliminate the risk of margin calls during broad market declines. The 2020 crash and 2022 bear market both demonstrated how correlation spikes when fear dominates, with diversified portfolios still dropping 30% or more in weeks. Conservative borrowing ratios only delay the problem rather than solve it, since volatility does not ask permission before arriving.

- Lenders prioritize speed and liquidity over tax efficiency or strategic timing when executing forced sales. Borrowers receive no input on which positions get sold or at what price, meaning concentrated positions intended for long-term holding can disappear in minutes. The sale proceeds reduce the loan balance, but the damage to portfolio composition and tax situation remains permanent, with recovery taking far longer than riding out a temporary drawdown with adequate cash reserves.

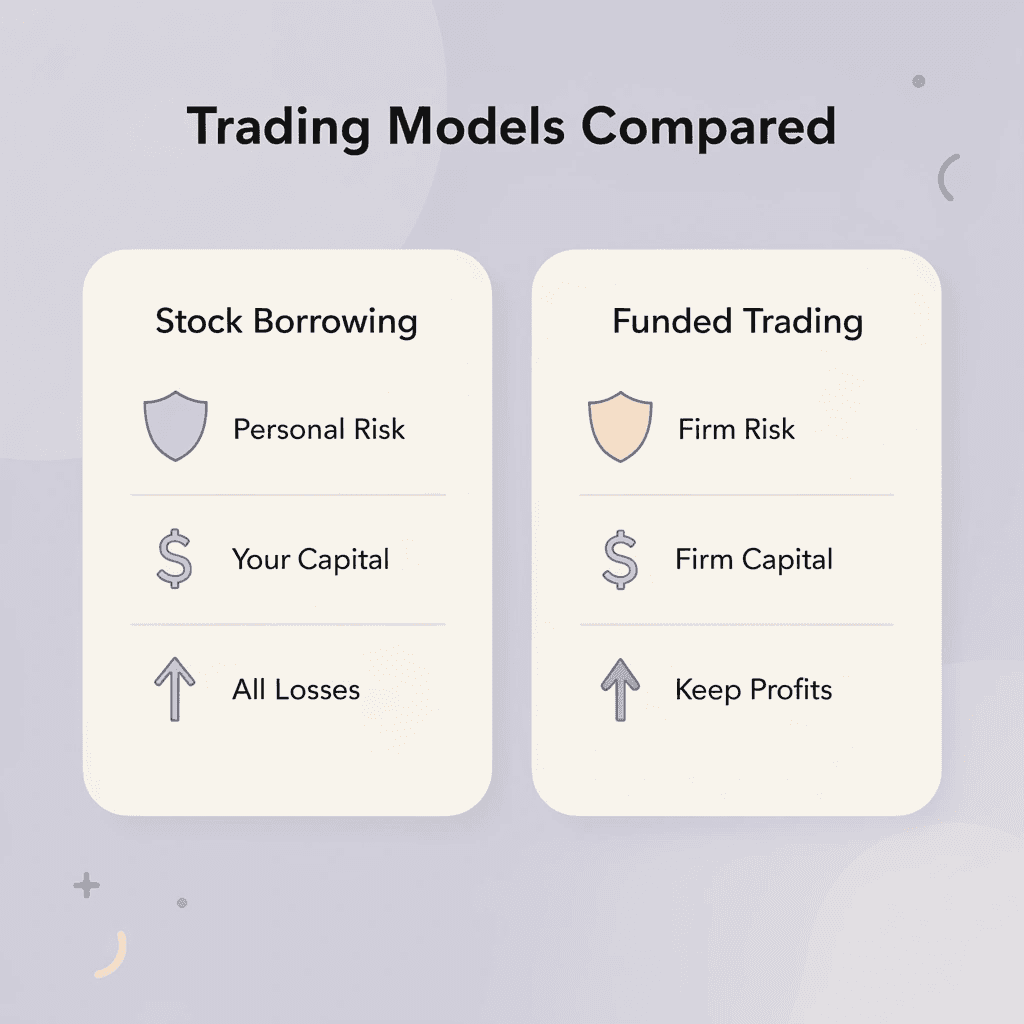

- Goat Funded Trader addresses this by providing up to $2 million in simulated trading capital through performance evaluations rather than collateral requirements, letting traders pursue opportunities without pledging personal holdings or managing margin calls during volatile periods.

What Does It Mean to Borrow Against Stocks?

Borrowing against stocks means using your investment portfolio as collateral to obtain a loan or line of credit. This provides access to cash without selling your shares. You pledge eligible securities—stocks, bonds, ETFs, mutual funds—held in a taxable brokerage account. The lender provides 50% to 70% of their value for equities. Your investments remain in your account, continue earning returns, and stay positioned for long-term growth while you use the borrowed money for nearly any purpose.

💡 Tip: Securities-based lending allows you to access liquidity without triggering taxable events from selling appreciated stocks.

"Lenders typically offer 50% to 70% of portfolio value for equity securities as loan-to-value ratios." — Financial Industry Standards

🔑 Takeaway: This strategy lets you maintain your investment positions while accessing capital for opportunities or expenses.

How Securities-Based Lending Works

You approach a lender with your portfolio details, and they evaluate your holdings based on asset type, liquidity, and volatility. Charles Schwab reports that investors can typically borrow up to 50% of the value of eligible securities, with more stable assets like Treasuries commanding higher percentages. Approval occurs within days with minimal paperwork. You draw what you need, pay interest only on the borrowed amount, and repay the principal on your own schedule while pledged securities remain under separate custody.

Why Investors Choose This Path

This strategy unlocks liquidity without disrupting your investment plan or triggering capital gains taxes. Your portfolio remains fully invested and compounding, avoiding the permanent loss of future growth from selling appreciated assets. Interest rates are lower than those of unsecured personal loans or credit cards because the loan is backed by marketable securities. You access funds on demand and repay without prepayment penalties, making it ideal for bridge financing, large expenses, or time-sensitive opportunities.

The Risks You Cannot Ignore

Market volatility creates the main danger. When your portfolio value drops, your collateral shrinks, which could trigger margin calls demanding immediate cash or additional securities. Forced liquidations occur when prices are already low. Interest costs accumulate over time, and variable rates can rise unexpectedly. This tool suits short to medium-term needs, not endless borrowing, and you must maintain reserves beyond minimum requirements to handle market changes without forced sales.

How do prop firms offer an alternative to borrowing against personal holdings?

Most investors borrowing against stocks already own substantial portfolios—they need existing wealth to access this liquidity. Prop firms like Goat Funded Trader flip that model by providing trading capital based on demonstrated skill rather than existing assets, letting traders pursue opportunities without pledging personal holdings or risking forced liquidations during market turbulence. But what happens when you want that cash flow without parting with ownership?

Related Reading

- Why Are Fidelity Margin Rates So High

- How Much Do Day Traders Make Per Month

- Can You Make A Living Day Trading

- How Does Margin Interest Work

- How Does Margin Work On Robinhood

- Financing Stock Options

- How To Compare Brokers By Margin Interest Rates

- How Is Margin Interest Calculated

- How Does Margin Work at Interactive Brokers

- How Much Margin Does Fidelity Offer

- What Is A Prop Firm Forex

- Why Is Schwab Margin Rate So High

- No Consistency Rule Prop Firm

- Options Trading Cash Flow Strategies Explained

Can I Borrow Against My Stocks Without Selling Them?

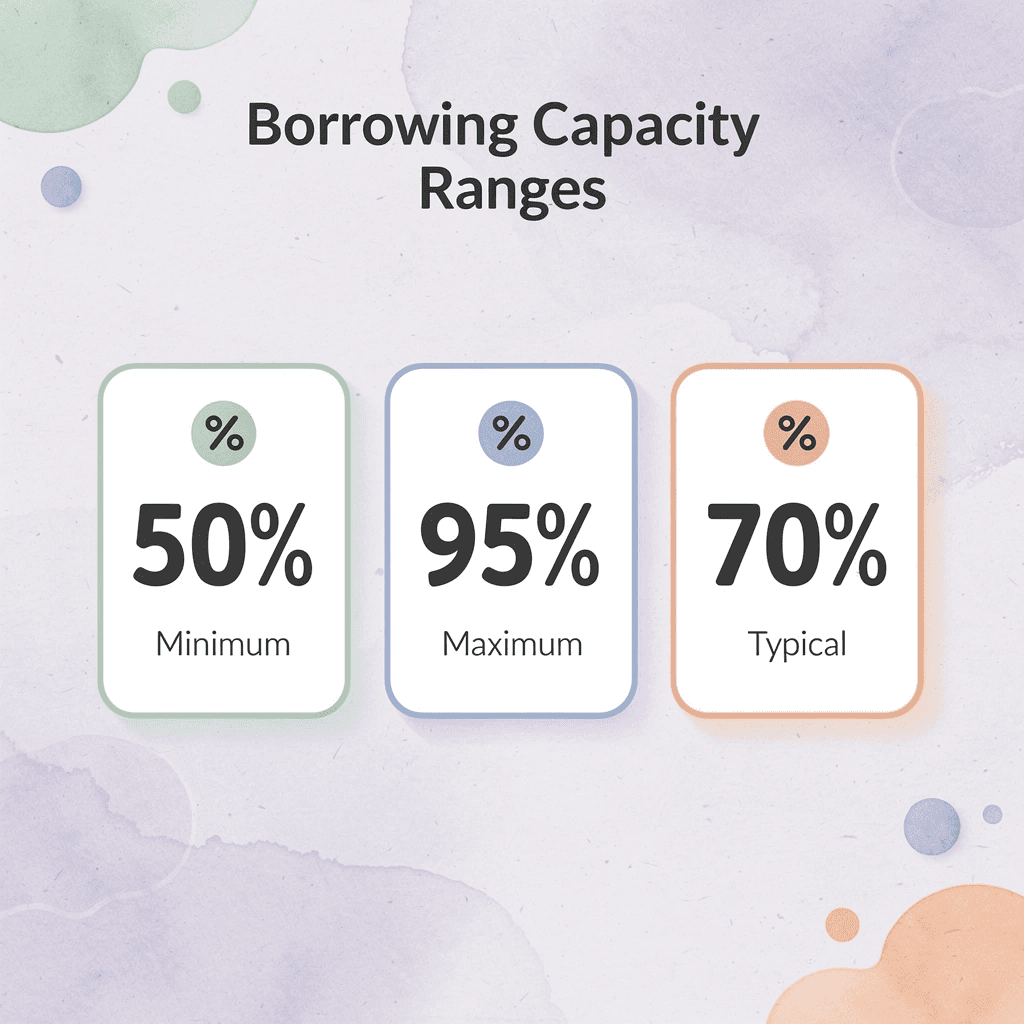

You can borrow money against stocks through securities-based lines of credit. You pledge your portfolio as collateral while your positions remain in your account, earning dividends and capturing appreciation. You can borrow 50% to 95% of portfolio value, depending on volatility and liquidity. You can draw funds immediately, pay interest only on what you use, and repay on your schedule without triggering capital gains taxes or disrupting your investment thesis.

"You can typically borrow 50% to 95% of portfolio value depending on volatility and liquidity." — Financial Research, 2016

🔑 Key Takeaway: Securities-based lending allows you to access liquidity without selling your investments, preserving your long-term positions while avoiding immediate tax consequences.

💡 Tip: This strategy works best for diversified portfolios with blue-chip stocks or ETFs, as these typically qualify for the highest borrowing ratios and lowest interest rates.

Who Qualifies for This Type of Lending?

Lenders look for investors with large, diverse taxable brokerage accounts that hold well-known stocks, investment-grade bonds, ETFs, and mutual funds. Most require a minimum portfolio value between $100,000 and $250,000, though private banks may ask for more. You need a steady income to cover interest payments and a strong credit history. Holdings in risky small-cap stocks or illiquid securities reduce your borrowing capacity, as lenders protect themselves against price declines that erode collateral value.

How Interest Rates and Terms Compare to Traditional Loans

Rates typically run between 4% and 8%, moving with benchmark indexes like SOFR or prime, since your pledged securities reduce the lender's risk. This beats unsecured personal loans at 10% to 15% or credit cards at 20% and higher. Most lines carry no origination fees or prepayment penalties, giving you flexibility to draw and repay as cash flow allows. The tradeoff is variable rates: if benchmarks climb, your carrying cost rises accordingly.

When This Strategy Makes Sense for Active Traders

Access to traditional capital requires pledging substantial personal assets as collateral, exposing you to personal financial risk and limiting growth potential. Prop firms like Goat Funded Trader grant access based on demonstrated skills rather than net worth, letting you pursue opportunities without risking your own money or facing margin calls during market volatility.

Tax Implications You Cannot Ignore

Borrowing against your stocks helps you avoid paying capital gains tax immediately, keeping your cost basis unchanged and deferring taxes until you sell. You can deduct the interest only if you use borrowed funds for qualified investment purposes, with deductions limited to your net investment income. Interest on borrowed funds used for personal expenses, real estate, or business ventures is not deductible. Consult a tax advisor before borrowing, as the IRS scrutinizes these transactions closely and thorough record-keeping is essential.

Maintenance Calls and What Triggers Them

When the market drops sharply, your collateral value falls below the lender's requirement, triggering a maintenance call. You must deposit more cash or securities within 24 to 48 hours. If you don't, the lender sells your holdings at low prices to restore the loan-to-value ratio. This forced sale locks in losses when the market might recover, turning a temporary price drop into permanent damage. Diversifying across asset types, borrowing conservatively, and maintaining cash reserves can mitigate this risk, though the threat remains.

Can I Lose My Stocks When Borrowing Against Them?

Yes, you can lose your stocks when borrowing against them. If the market moves against you and you fail to meet a margin call, the lender can sell your shares without your permission to recover the money you borrowed.

⚠️ Warning: When you use stocks as collateral, you're essentially putting your ownership at risk. The lender has the legal right to liquidate your positions if your account falls below maintenance requirements.

"Margin calls can force investors to sell their stocks at the worst possible time - when prices are already falling." — Financial Industry Regulatory Authority (FINRA)

🔑 Takeaway: Stock-backed borrowing is not a guaranteed way to access cash. The forced sale risk means you could lose your investment positions precisely when you least want to sell them - during market downturns.

The Control You Think You Have

When you pledge stocks as collateral, you give the lender certain rights during stressful market times. You still own the stocks and receive dividends, but the lender has first claim on them if the loan-to-value ratio falls below the agreed limit. Many traders believe they control when any sale occurs because their name appears on the account statement. However, the maintenance agreement stipulates otherwise. When collateral value drops and you cannot restore the ratio by adding cash or securities, the lender sells immediately to protect their position, not yours.

What Triggers Forced Sales

Lenders recalculate your portfolio value daily, sometimes multiple times during volatile trading sessions. A 20% market drop can push your loan-to-value ratio from a comfortable 40% to a dangerous 50% overnight, crossing the maintenance threshold that triggers a margin call. You then face a narrow window, typically 24 to 48 hours, to deposit cash or transfer additional securities. Missing that deadline means automatic liquidation of holdings the lender selects, often starting with the most liquid positions, regardless of your tax situation or long-term strategy. SmartAsset notes that forced sales can trigger a 30% capital gains tax on appreciated positions, compounding the financial damage beyond the lost shares.

Why Diversification Does Not Eliminate Risk

Spreading your portfolio across different sectors and asset classes reduces the risk of concentration in a single stock. However, diversification cannot prevent margin calls when the entire market declines. The March 2020 crash and the 2022 bear market both demonstrated how correlations increase during periods of market fear.

Diversified portfolios dropped 30% or more in weeks, triggering widespread margin calls across thousands of accounts. A 30% loan-to-value ratio becomes a 43% ratio after a 20% portfolio decline, and volatility arrives without warning.

What alternatives exist when you can borrow against your stocks

Traders seeking capital have two choices: risk their own money by taking out loans secured by current assets, or demonstrate strong trading skills to earn funding without risking personal holdings. Platforms like Goat Funded Trader offer practice accounts where strong performance unlocks real funding, eliminating the need for high net worth and the risk of forced liquidation to cover losses.

The Liquidation Process Itself

When the lender initiates forced sales, you lose control over which positions are liquidated and at what price. The process prioritizes speed and liquidity over tax efficiency or strategic timing. Concentrated positions you planned to hold for years vanish in minutes. Losses that might have recovered over months become permanent. Recovery from forced liquidation takes considerably longer than recovery from a temporary drawdown managed with adequate cash reserves. But what if you could access the capital you need without risking your portfolio?

How to Borrow Against Stocks Without Selling: A Step-by-Step Guide

Securities-based lending lets you use stocks, bonds, and ETFs as collateral to obtain a line of credit without selling your positions. You retain your full market exposure, collect dividends, and access cash within days. The process requires a minimum account size, typically $100,000 or more, and depends on which assets qualify and how lenders calculate your borrowing capacity.

🎯 Key Point: Securities-based lending allows you to unlock liquidity from your investment portfolio while maintaining your complete market position and dividend income.

"Securities-based lending provides investors with immediate access to capital while preserving their long-term investment strategy and market exposure." — Financial Planning Association, 2024

⚠️ Warning: Most lenders require a substantial minimum account balance of $100,000 to $250,000 to qualify for securities-based lending programs, making this option primarily available to high-net-worth investors.

Stock / Securities Loan Feature Overview

- Minimum account size

- $100,000 – $250,000 required

- Eligible securities

- Stocks

- Bonds

- ETFs

- Funding timeline

- 3–7 business days

- Market exposure

- 100% maintained throughout the loan period

Start with Portfolio Assessment

Review your taxable brokerage accounts to identify qualifying securities. Lenders prefer liquid, diversified holdings like blue-chip stocks, investment-grade bonds, and broad-market ETFs. Concentrated positions in a single stock, thinly traded securities, or restricted shares face stricter limits or exclusion. Retirement accounts don't qualify because IRS rules prohibit using tax-advantaged assets as collateral for loans. If your portfolio falls below the minimum threshold or holds mostly illiquid positions, adjust your holdings or explore alternative sources of capital before applying.

Compare Lenders and Terms

Contact your current brokerage first, as established relationships often unlock faster approvals and better rates. Compare their offerings with those of private banks, affiliated lenders, and specialized firms. Focus on three variables: interest rates (typically tied to SOFR or prime), advance rates (the percentage of portfolio value you can borrow), and maintenance requirements (the collateral threshold that triggers margin calls). According to J.P. Morgan, most lenders set a 50% loan-to-value ratio for equities, though bonds and Treasuries may qualify for higher percentages. Request detailed documentation on how quickly the lender issues margin calls and what notification window you'll receive if markets decline.

Complete the Application

Submit your application with portfolio statements, identification, and basic financial information. The lender assigns a lending value to each holding based on liquidity and volatility, then calculates your total credit limit. Approval moves quickly because your securities back the loan, not your credit score. Sign the securities-based lending agreement, which outlines your borrowing capacity, interest terms, repayment flexibility, and the lender's rights if collateral falls below maintenance thresholds. Your pledged assets are transferred to a separate account, where the lender monitors their value in real time.

Draw Funds and Monitor Collateral

Move cash to your checking account when you need it for non-securities purchases. Interest accrues only on what you owe, so borrow only what you need to handle normal market changes.

Watch your loan-to-value ratio using the lender's online portal, as market drops recalculate your available credit daily. If market swings push your ratio above maintenance thresholds, you'll receive a margin call requiring you to add cash, securities, or repay part of the loan within 24 to 48 hours.

Answering margin calls quickly prevents the lender from selling your holdings without permission, but the pressure to act fast during market stress creates genuine worry for borrowers who lack a sufficient cushion.

What alternatives exist to borrowing against your portfolio?

Most investors believe borrowing against stocks is their only way to access capital without selling, but that approach still puts personal wealth at risk. Prop firm offers traders a different model in which proven skill unlocks access to simulated capital accounts of up to $2 million, with profit splits reaching 100%.

Instead of pledging your portfolio as collateral and managing margin calls, you earn trading capital through performance evaluations that assess your strategy and risk management. This shift removes personal financial exposure while preserving your ability to grow wealth through active trading. But what happens when the market drops faster than you can respond?

Related Reading

- How To Day Trade Without 25k

- Is Issuing Common Stock A Financing Activity

- Best Prop Firm For Stocks

- How To Become A Trader From Home

- How Do You Profit From Day Trading Stocks

- How To Borrow Against Stocks

- How Do You Take Profit In Crypto Trading

- Best Crypto Prop Firm

- Lowest Margin Rates Brokers

- Sbloc Vs Margin Loan

- Position Sizing In Trading

- Prop Trading Firms' Profit-Sharing Models

- Position Sizing Day Trading

- How To Stay Consistent In Trading

How Goat Funded Trader Acts as a Safer Alternative to Borrowing Against Stocks

Borrowing against stocks moves market risk directly to your personal wealth. Goat Funded Trader changes that by providing up to $2M in simulated trading capital through performance evaluations. You trade the firm's capital under clear risk rules, keep 80–100% of profits, and the firm absorbs all losses. Your portfolio remains protected: no margin calls threaten your holdings, and forced liquidation from market swings cannot occur.

🎯 Key Point: With Goat Funded Trader, your personal assets remain completely protected from trading losses, eliminating the catastrophic risk that comes with stock-secured borrowing.

"You trade the firm's capital under clear risk rules, keep 80-100% of profits, and the firm takes all losses." — Goat Funded Trader Risk Model

🔑 Takeaway: This model transforms trading from a wealth-threatening activity into a pure opportunity - you get substantial capital to trade with zero personal financial exposure.

Your Personal Assets Stay Completely Off the Table

Securities-based lending puts your stocks at risk during market volatility. Goat Funded Trader eliminates that danger: you never pledge collateral. Instead, you pass evaluation phases that test your strategy and risk management, then receive funded status with our capital. If a trade fails, you reset the evaluation for a small fee rather than having your holdings sold to cover a margin call. One model risks what you own; the other risks what you've earned access to through skill.

Fixed Risk Parameters Replace Unpredictable Margin Pressure

Margin lending creates moving targets: loan-to-value ratios shift daily, maintenance requirements change without warning, and gap-down opens can trigger liquidation before you react. Goat Funded Trader establishes transparent limits from the start: a 3% daily loss cap, a 6% maximum drawdown, and clear consequences for violations. You know exactly where the boundaries sit, and breaching them doesn't cost personal assets or trigger tax events—it simply pauses your account until you reset or adjust. This predictability lets you focus on execution rather than monitoring collateral ratios and interest accruals, which compound during drawdowns.

Capital Scales Without Increasing Personal Exposure

Traditional borrowing ties available capital to portfolio size, requiring either additional collateral or higher leverage risk to expand.

How does funded trading compare to borrowing against stocks for growth?

Goat Funded Trader's scaling plan grows your account from $10,000 to $2 million based on consistent performance, with no additional personal investment required beyond the initial evaluation fee. Each tier unlocks larger position sizes and higher absolute profit potential while maintaining the same protective risk rules. You build a trading career that compounds through skill rather than pledging more of your retirement accounts or taxable holdings.

What advantages do funded platforms offer over traditional borrowing?

Most traders borrow money, believing leverage is the only path to substantial returns. Platforms like Goat Funded Trader provide traders access to significant capital based on demonstrated trading ability rather than collateral. Our platform enables strategies across forex, stocks, indices, and crypto with tight spreads and fast execution, with withdrawals available every two weeks or within 24–48 hours on demand. Our model aligns incentives: you profit when you succeed, and you never risk your own capital when markets move against your position.

How do profit splits replace traditional borrowing costs?

Borrowing costs you money whether you win or lose. Interest accrues on the full loan balance, and your gains are reduced by financing charges that grow over time. Our Goat Funded Trader program pays you instead.

What returns can traders expect without debt obligations?

Profit splits start at 80% and reach 100% with add-ons, converting successful trades into withdrawable cash with no repayment schedules or debt service. A trader capturing $20,000 in monthly gains on a $200,000 account keeps $16,000 to $20,000, depending on the split structure, with no interest drag and no obligation to repay principal, since there is no loan. The economics work the opposite way: from paying to access capital to getting paid for using it well.

Related Reading

- Best Forex Prop Firm

- Best Margin Rates Brokers

- Margin Loan vs. Securities-Based Lending

- How Does A Margin Loan Work

- How to Become a Full Time Trader

- How To Trade Forex With A Prop Firm

- Forex Trading Strategies For Consistent Profits

- Options Trading Strategies For Consistent Income

- How To Get Profit In Option Trading

- Day Trading Strategies For Consistent Profits

- Trading Cash Flow

- Recommended Prop Trading Firms With Growth Plans

- Best Trading Strategies For Consistent Profits

Get 25-30% off Today - Sign up to Get Access to Up to $800K Today

Goat Funded Trader replaces collateral with performance. You gain access to up to $2 million in simulated trading capital by passing a structured evaluation that tests your ability to manage risk. Pass the challenge, and you receive a funded account where you keep 80 to 100 percent of every dollar you earn, with profits paid within 24 hours or guaranteed at $1,000 minimum. Your personal stock portfolio stays untouched, fully invested and compounding without liquidation risk.

🎯 Key Point: The evaluation sets clear boundaries: a 3 percent daily loss limit and 6 percent maximum drawdown. Break those rules, and you reset the challenge for a one-time fee that gets fully refunded once you pass and receive funding. No lender monitors your loan-to-value ratio. No margin clerk calls demanding you wire cash or sell shares. No forced liquidation of your holdings because the market dropped. You trade stocks, forex, ETFs, and crypto on MT5 with full freedom to hold positions over weekends, trade through news events, and scale without time limits.

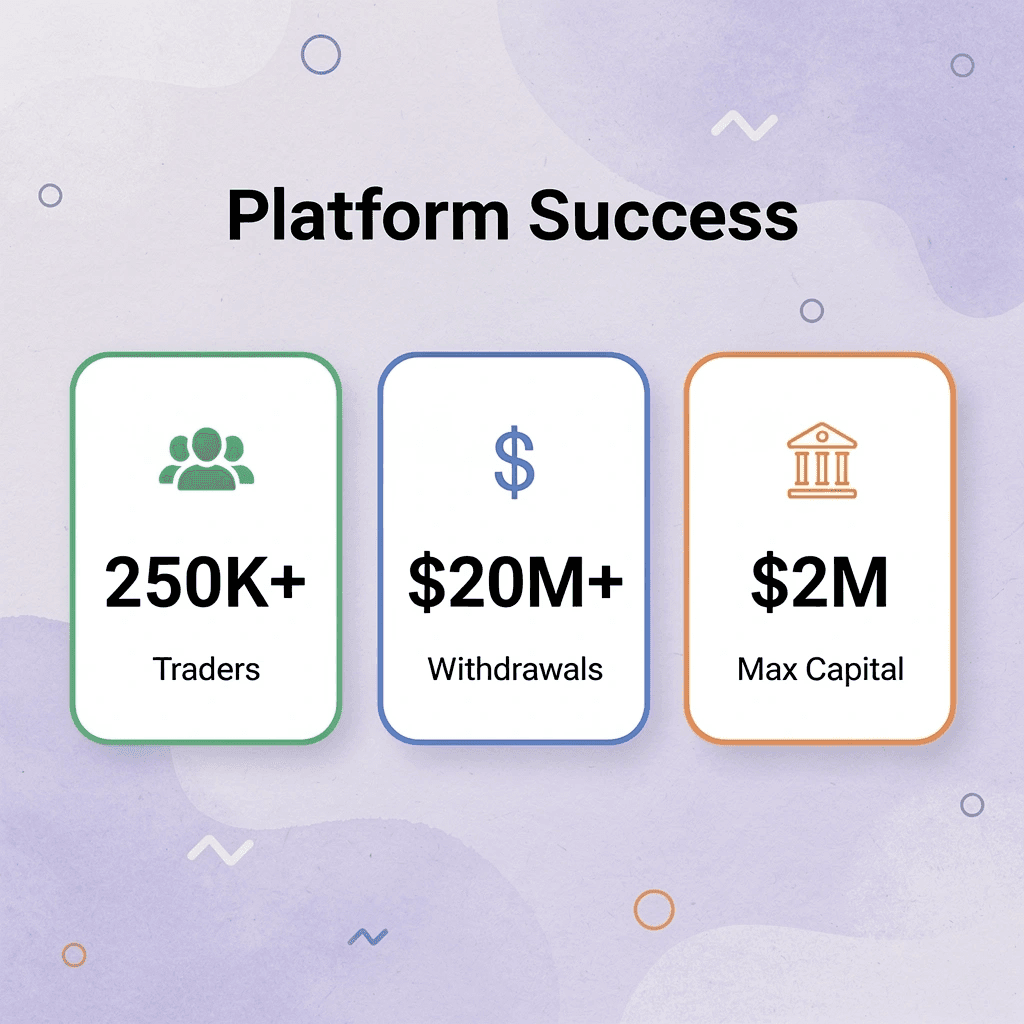

"Over 250,000 traders have joined the platform, and the firm has paid more than $20 million in real withdrawals." — Goat Funded Trader, 2024

An 8 percent monthly return on a $200,000 account puts $16,000 in your bank account with zero downside to your own capital. Your stock portfolio continues earning dividends and appreciation while you build a separate income stream with no interest expense, no repayment schedule, and no threat to your long-term wealth.

Traditional Trading vs Goat Funded Trader

- Capital at risk

- Traditional trading: Risk your own capital

- Goat Funded Trader: Risk simulated capital

- Downside protection

- Traditional trading: Margin calls & liquidation possible

- Goat Funded Trader: No forced liquidation (rule-based risk limits apply)

- Cost structure

- Traditional trading: Interest on borrowed funds (if using margin)

- Goat Funded Trader: No interest expense

- Capital access

- Traditional trading: Limited by personal funds

- Goat Funded Trader: Up to $2M access

- Profit retention

- Traditional trading: Keep 100% of profits

- Goat Funded Trader: Keep 80–100% of profits

🔑 Takeaway: Join Goat Funded Trader and access serious capital with real rewards and total protection. Use code FIRSTGFT for 50 percent off your first order. The one-time fee is fully refundable upon funding; no credit card is required to explore, and you can begin your evaluation in minutes.

Be Great and get the App

.webp)