How Is Margin Interest Calculated? All You Need to Know

How is margin interest calculated? Goat Funded Trader explains the formulas, factors, and strategies to minimize your trading costs effectively.

.png)

Margin trading amplifies buying power by allowing traders to borrow funds from brokers, but those borrowed funds come with interest charges that can significantly impact profits. Brokers calculate margin interest using specific formulas and daily compounding methods that many traders don't fully understand. These calculations determine how much traders pay for leveraged positions, making it crucial to grasp the mechanics before committing capital. Understanding margin interest helps traders make informed decisions about when leverage makes financial sense.

Calculating margin interest involves daily rates applied to borrowed amounts, with costs accumulating quickly on extended positions. Smart traders learn these formulas to avoid surprise charges that erode returns. For those seeking substantial capital without interest concerns, partnering with a prop firm provides access to trading capital while retaining a significant share of the generated profits.

Summary

- Margin interest accrues every single day on borrowed funds using a 360-day year calculation, which means a $20,000 loan at 10% annual rate costs $5.56 daily or roughly $167 monthly before compounding. Most traders discover this reality only after seeing unexpected charges appear in their account, often when positions are already underwater. The cost runs silently, whether your trade thesis proves correct or not, and unpaid charges roll into your debit balance each month to generate interest on interest.

- Broker rate structures vary dramatically based on balance size and platform choice. M1 Finance charged 3.99% in 2026, while traditional firms routinely exceed 10% for smaller balances, and a single percentage point difference on a $50,000 loan costs $500 annually. Brokers tier their rates to reward larger loans with lower percentages, so consolidating positions at competitive providers instead of splitting across multiple accounts can drop you from 8% to 6% and save $600 per year on a $30,000 debit balance.

- Margin requirements and margin interest operate simultaneously but serve completely separate functions in leveraged accounts. Requirements determine how much you can borrow (typically 50% at purchase) and trigger forced liquidations when equity falls below maintenance thresholds of 25 to 30%. Interest charges you for the privilege of borrowing that money every single day, compounding monthly and eroding returns even on winning trades held too long. Traders who fixate on interest rates while ignoring requirement ratios get blindsided by margin calls during routine pullbacks.

- Short holding periods reduce total interest paid but cannot eliminate the charge entirely. A swing trade needing three weeks to reach the target on a $20,000 borrowed position at 8% costs $200 in financing alone, turning what looks like a $1,200 gain into $1,000 net after borrowing costs. Interest stops only when your debit balance reaches zero through sales, cash deposits, or security transfers, forcing traders to treat borrowed funds as a temporary and expensive tool rather than permanent capital.

- •Traders may lose up to 50% of their initial investment when margin interest and volatility combine, illustrating how borrowing costs amplify losses beyond position performance alone. The compounding effect creates a double drain where falling equity pushes accounts closer to margin calls while rising debit balances from unpaid interest generate additional daily charges on money already lost.

- Goat Funded Trader addresses this by providing simulated capital accounts up to $2 million with no personal debit balance, which removes the need for daily interest calculations and lets traders keep 80% to 100% of profits under transparent risk rules, rather than managing compounding borrowing costs.

What Is Margin Interest in Trading, and How Does It Work?

Margin interest is the daily cost you pay to borrow money from your brokerage to trade. Once you use margin, your broker becomes your lender, and interest accrues on that borrowed balance regardless of whether your positions gain or lose value. Most traders discover this when unexpected charges appear in their account, often while positions are already losing money.

💡 Example: If you borrow $10,000 on margin at 8% annual interest, you'll pay approximately $2.19 per day in interest charges, regardless of whether your trades are profitable.

⚠️ Warning: Margin interest compounds daily, meaning the longer you hold leveraged positions, the more it eats into your potential profits or amplifies your losses.

The Mechanics Behind the Loan

When you open a margin account, you enter into a lending relationship in which your securities serve as collateral. According to Charles Schwab, you can borrow up to 50% of your account balance to buy additional securities. To control $10,000 worth of stock, you deposit $5,000 and borrow the rest. The broker holds your portfolio as security, and as long as your equity stays above the 25% minimum maintenance requirement, the loan remains active. Interest compounds daily and posts to your account monthly, with no fixed repayment schedule.

How Brokers Calculate Your Daily Cost

Brokers use a straightforward formula: take your borrowed amount, multiply it by the annual interest rate, divide by 360, then multiply by the number of days. If you borrow $5,000 at an 8% annual rate, you pay roughly $1.11 per day—$33 per month or $400 annually—whether your trade wins or loses. Rates are tiered: a $5,000 loan costs 10% annually, while a $100,000 loan drops to 6%. Since compounding happens daily before the monthly bill arrives, your actual cost exceeds the stated rate.

Why Rates Swing and What That Means for You

Competitive platforms like Interactive Brokers or Robinhood offer rates as low as 5% for larger balances, while traditional brokers charge over 11% for smaller accounts. Your rate depends on your debit balance tier and the broker's base rate, which shifts with market conditions. Brokers can adjust rates without warning: a trade opened at 7% might cost 9% three months later. Choosing a broker based on your margin usage can mean the difference between paying $400 or $700 annually on the same $5,000 loan.

How does borrowed capital amplify trading risks

Borrowed money amplifies both losses and gains. A 10% portfolio drop reduces your equity and pushes you closer to a margin call, where the broker forces you to deposit cash or sell positions at the worst possible time. Interest accrues as your account value declines, increasing your debt as your equity falls. Brokers can sell your holdings without warning if your account falls below maintenance levels, and you remain liable for any remaining debt after the sale.

What alternatives exist to margin interest structures

For traders focused on growing performance without daily interest charges, prop firm structures offer an alternative. Funded accounts through Goat Funded Trader provide access to substantial capital while letting you keep a significant share of the gains you generate. The cost structure shifts from daily compounding interest to performance-based splits, keeping your edge focused on execution rather than borrowing costs.

How is margin interest calculated versus borrowing rules

Understanding margin interest is only half the equation; the real confusion starts when traders mix up the cost of borrowing with the rules governing how much they can borrow.

What Is the Difference Between Margin Interest and Margin Requirements?

Margin interest charges you for borrowing money; margin requirements determine how much you're allowed to borrow. One is a recurring expense that accrues daily on your loan balance. The other is a regulatory threshold that sets minimum equity levels and triggers forced liquidations when those levels are breached.

🔑 Key Takeaway: Margin interest is the cost you pay for leverage, while margin requirements are the rules that govern how much leverage you can use.

"Understanding the distinction between margin costs and margin limits is essential for managing leveraged positions effectively." — Financial Trading Fundamentals

⚠️ Warning: Confusing these two concepts can lead to unexpected costs and forced liquidations that could have been avoided with proper planning.

How do initial requirements determine your borrowing limits?

When you open a leveraged position, Charles Schwab enforces a 50% margin requirement at purchase, meaning you must provide half the money yourself. If you buy $40,000 worth of stock, you deposit $20,000 and borrow the rest. Brokers may raise this requirement on volatile stocks. The requirement acts as a gatekeeper, preventing excessive risk.

What happens when maintenance requirements kick in?

After you buy, maintenance requirements take over. Your equity must remain between 25% and 30% of the current market value, depending on broker rules. If your equity falls below that floor, you receive a margin call demanding immediate cash or collateral. If you fail to comply, the broker liquidates your holdings without warning, often at the worst possible prices.

How does margin interest drain capital over time

Interest on borrowed money accrues daily based on your balance, regardless of investment performance. If you borrow $15,000 at 8% per year, you pay $3.29 daily—approximately $1,200 annually. Holding that position for six months while the market remains flat costs $600 in interest before any profit materializes. The charge compounds monthly, reducing your returns even when your trade thesis proves correct.

Many traders focus on interest rates but ignore requirement ratios, then get surprised by margin calls during normal market drops. Others watch their account value closely but underestimate how interest reduces gains on winning trades held too long. Both mistakes stem from treating these tools as equivalent when they operate on different timelines and produce different results.

What do margin debt statistics reveal about market risk

FINRA data shows U.S. customer margin debt stood at $1.221 trillion in March 2026, reflecting widespread use of borrowed money despite market volatility. This level indicates many investors operate near margin requirements, where small market drops trigger calls and forced sales.

How do prop firms eliminate margin interest calculations

Prop firms like Goat Funded Trader remove both interest charges and the stress of maintenance requirements. Our platform lets you trade simulated capital without borrowing costs or forced liquidations, keeping up to 100% of the profit you generate. Your focus stays on execution and strategy, not managing debt ratios or calculating daily interest drag. But even if you eliminate interest entirely, one question remains: have you escaped leverage costs altogether?

Related Reading

- What Is A Prop Firm Forex

- How To Compare Brokers By Margin Interest Rates

- How Does Margin Work On Robinhood

- How Much Do Day Traders Make Per Month

- No Consistency Rule Prop Firm

- How Does Margin Work at Interactive Brokers

- Financing Stock Options

- How Much Margin Does Fidelity Offer

- Why Are Fidelity Margin Rates So High

- Options Trading Cash Flow Strategies Explained

- Can You Make A Living Day Trading

- Why Is Schwab Margin Rate So High

- How Does Margin Interest Work

Can Margin Interest Be Avoided?

Margin interest cannot be avoided once you borrow in a margin account. It builds up every single day on any money you owe and only goes away when you pay back the full loan balance.

🎯 Key Point: The daily compounding nature of margin interest means that every day you delay repayment increases your total borrowing costs.

"Margin interest accrues daily and compounds over time, making it one of the most expensive forms of investment financing available to retail traders." — Financial Industry Regulatory Authority (FINRA)

⚠️ Warning: Unlike credit card interest, which may offer grace periods, margin interest starts accumulating immediately upon borrowing and continues 24/7 until the entire balance is repaid.

The Common Belief That Misleads Traders

Traders assume they can avoid margin interest by holding positions briefly, selling at the right time, or switching to platforms with lower rates. This view ignores how interest accrues daily regardless of trade performance or market direction.

Why the Belief Falls Apart

Your broker lends you money secured by your securities. Interest accrues daily based on a 360-day year. When you sell securities or make deposits, they reduce your debt only after the trade settles. Any remaining balance incurs fees, even if you hold the borrowed money overnight.

How does compounding interest impact trading performance?

Interest compounds monthly, turning small loans into steady performance drags. Traders can lose up to 50% of their initial investment when margin interest and volatility combine, demonstrating how borrowing costs amplify losses beyond the position's underlying performance.

Why do traders underestimate how margin interest is calculated?

A 2015 FINRA-linked investor survey in an SEC staff working paper found that only 15% of margin traders answered a basic question about how margin works correctly, compared to 31% of non-margin traders. This knowledge gap leads traders to underestimate the accumulation of costs.

What do real trading records reveal about borrowing costs?

A study of Chinese futures traders using brokerage records found that higher leverage produced 13% net annualized underperformance after costs, as borrowing expenses and frequent trading erased gains and amplified losses. Broker rate comparisons reveal standard margin rates at major firms ranging from 5% to over 11%, with many retail accounts facing 10%+ tiers. A $50,000 debit at 10% generates $5,000 in annual interest, a fixed drag that short-term trades rarely outrun after taxes and slippage.

Practical Ways to Minimize Margin Interest

Put enough cash in your account to cover positions fully and trade only in cash accounts to avoid borrowing costs. Use margin only for short-term opportunities where expected gains exceed daily interest charges. Pay down debit balances immediately after selling rather than letting them accumulate. Compare rate levels across brokers and move larger balances to the lowest-rate brokers. Platforms like Goat Funded Trader eliminate the stress of interest charges and maintenance requirements. Our platform lets you trade simulated capital without borrowing costs or forced liquidations, keeping 100% of the profit you generate.

When Margin Interest Disappears Completely

Margin interest stops only when your account shows a zero or credit balance. Sell positions, add fresh cash, or transfer securities to eliminate the loan. This forces traders to treat borrowed funds as temporary, expensive capital. Calculate exact daily interest before every margin trade and track your debit balance carefully. The real question is how to measure the cost to you on a daily basis.

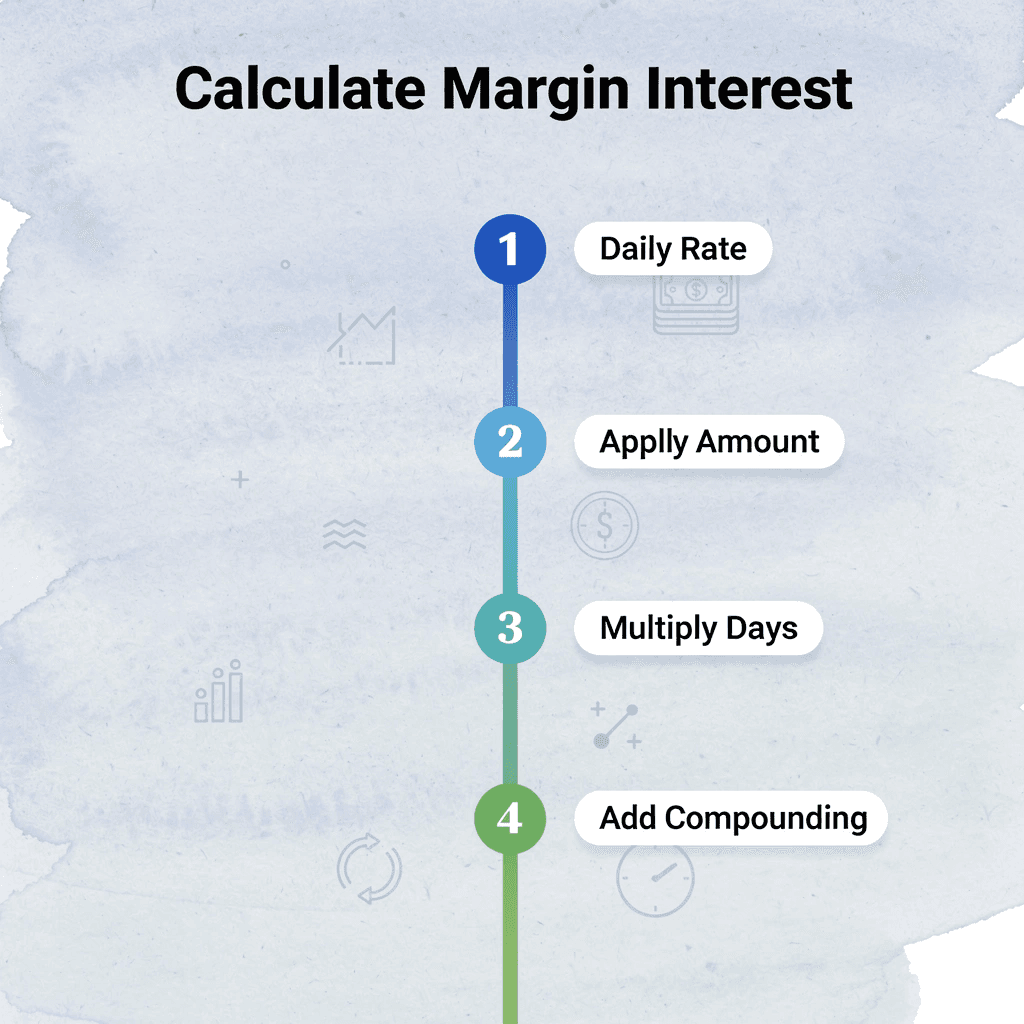

How to Calculate Margin Interest Step-by-Step

To calculate daily interest, multiply the amount you borrowed by the yearly interest rate, divide by 360, then multiply by the number of days you hold the position. Daily interest compounds if you don't pay it, meaning it gets added to what you owe and then earns interest on top of that. Most brokers charge you once a month, but the costs accumulate daily.

💡 Pro Tip: Always track your daily interest costs to avoid surprises on your monthly statement. The compounding effect can significantly increase your total borrowing costs over time.

⚠️ Warning: Many traders underestimate how quickly margin interest accumulates. Even a low daily rate can become a substantial cost when positions are held for weeks or months.

Find Your Exact Debit Balance

Your debit balance is the exact dollar amount you owe the broker at the end of each trading day. Log in to your account and find this number in the balances or margin section. It changes as positions move, dividends are posted, or you deposit cash. A trader who borrows $30,000 to buy shares sees that balance drop to $25,000 after depositing $5,000, reducing daily interest immediately. Check this number before market close each day, as overnight price swings can shift it by morning.

Confirm Your Interest Rate Tier

Brokers publish tiered rate schedules that drop as your debit balance grows. A 12.25% annual interest rate applies to certain balance ranges, though smaller loans carry higher effective rates while six-figure balances qualify for discounts. Check your account settings or rate disclosure page for your exact tier. Rates adjust when market conditions shift, or your balance crosses a tier threshold.

Apply the 360-Day Formula

Take your debit balance, multiply it by the annual rate as a decimal, divide by 360, then multiply by the number of days outstanding. A $20,000 loan at 10% annual interest costs $5.56 per day: (20,000 × 0.10) ÷ 360 × 1. Hold that position for 30 days, and you owe $166.67 in interest before any trades close. Brokers use a 360-day year instead of 365 for simplicity, which slightly raises the effective daily rate. Run this formula each time you enter a margin trade to see the true cost before profit projections.

Track Monthly Posting and Compounding

Interest accrues daily but appears on your statement monthly. Unpaid charges are added to your balance and begin accruing interest, creating a cycle that accelerates your costs.

How does compounding affect your margin interest calculations?

A trader who ignores $200 in monthly interest for three months sees the unpaid amount grow from $600 to $618 as it compounds. Track your month-to-date interest in the account summary and pay it down before the statement closes to prevent compounding.

What alternatives exist to avoid margin interest entirely?

Prop firm accounts eliminate margin interest by providing traders with simulated capital, no personal money at risk, and no borrowing costs. Our platform lets traders focus on execution and profit splits. Skilled traders can grow to $2M in buying power without the accumulating debt that drains performance in standard brokerage accounts. Calculating margin interest keeps you honest about leverage costs, but knowing the daily burn rate matters only if you act on it before compounding takes over.

Related Reading

- How To Become A Trader From Home

- Position Sizing In Trading

- How To Borrow Against Stocks

- How To Day Trade Without 25k

- Sbloc Vs Margin Loan

- Lowest Margin Rates Brokers

- Is Issuing Common Stock A Financing Activity

- Best Prop Firm For Stocks

- How Do You Take Profit In Crypto Trading

- Best Crypto Prop Firm

- Prop Trading Firms' Profit-Sharing Models

- How To Stay Consistent In Trading

- Position Sizing Day Trading

- Can I Borrow Against My Stocks

- How Do You Profit From Day Trading Stocks

6 Smart Strategies to Manage Margin Interest Efficiently

Smart traders treat margin interest as a cost they can control rather than a tax for using leverage. The strategies below help cut borrowing costs without sacrificing the power of margin.

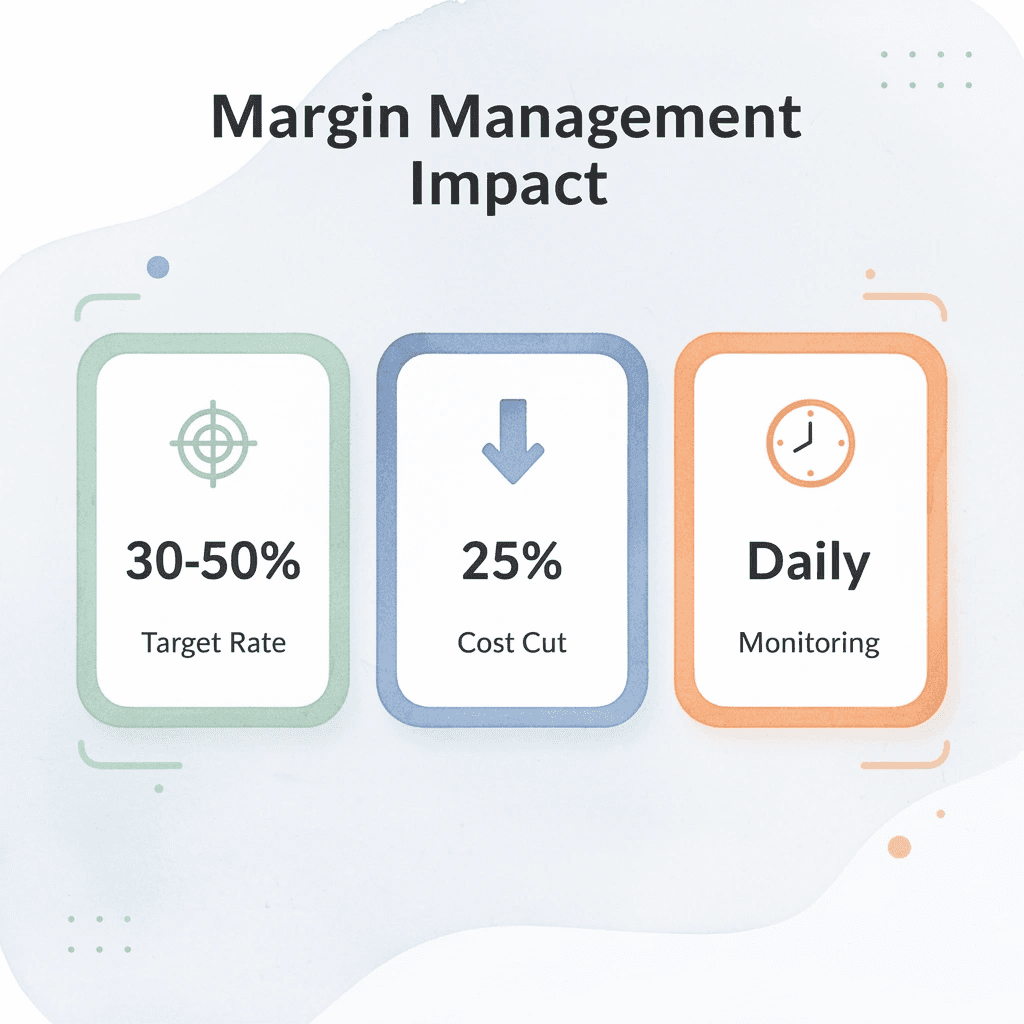

🎯 Key Point: The most effective approach is to monitor your margin balance daily and maintain a target utilization rate of 30-50% of your available margin. This keeps interest costs manageable while preserving your ability to capitalize on high-conviction opportunities.

"Successful margin management isn't about avoiding borrowing costs entirely—it's about optimizing the cost-to-opportunity ratio and keeping interest expenses predictable." — Trading Risk Management Study, 2023

⚠️ Warning: The biggest mistake traders make is treating margin interest like a fixed expense. Your borrowing costs compound daily, so even small delays in position management can turn a profitable trade into a break-even or losing proposition over time.

1. Select Brokers with the Lowest Tiered Rates

Margin rates vary significantly across platforms. M1 Finance charged 3.99% in 2026, Interactive Brokers around 5.33% for Pro accounts, and Robinhood near 5.05%, while traditional firms often charge more than 10% for smaller balances. A single percentage point difference on a $50,000 loan costs $500 annually. Check rate schedules every three months as base rates change, and move larger debit balances to the provider with the best rates.

How does consolidating balances reduce margin interest costs?

Brokers organize their rates by account size, offering better rates for larger loans. Combining a $30,000 position at one broker instead of splitting it across three accounts might lower your rate from 8% to 6%, saving $600 per year—enough to cover slippage on multiple trades.

2. Limit Borrowing to Short-Term Trades Only

Interest compounds daily on the full debit balance, so holding leveraged positions for weeks turns small costs into significant drags. Restrict margin to intraday or swing trades you plan to exit within days, where expected gains exceed daily interest, slippage, and taxes. A $20,000 borrowed position at 8% costs $4.44 per day, or $200 in financing alone over 45 days.

How does closing positions quickly reduce margin interest costs?

Close positions fully after targets are hit and immediately use the proceeds to reduce the loan. Traders who roll borrowed funds into the next setup without paying down their balances create a compounding cycle in which interest charges on old trades bleed into new ones.

3. Maintain Conservative Leverage and Strong Equity Buffers

Borrowing the maximum allowed leaves no room for market changes and risks, margin calls that force sales at unfavorable prices. Fund 70 to 75% of positions with your own capital and borrow only 25 to 30% to lower daily interest and maintain equity well above maintenance requirements. Set personal equity alerts higher than broker minimums and monitor daily. The buffer absorbs volatility and prevents forced liquidations.

What alternatives exist when margin interest becomes too expensive

When retail margin interest becomes too expensive for steady growth, prop firm funding offers an alternative. Traders demonstrate consistent performance on practice accounts with set loss limits, then receive real profit splits (often 80 to 100%) when they perform well, with Goat Funded Trader providing the capital. This lets skilled traders manage large positions and grow without paying ongoing margin interest.

4. Pay Down Debit Balances Aggressively After Every Sale

When you sell a position, the money automatically reduces your margin loan. Depositing extra cash accelerates repayment. Check your account daily and apply any extra cash or profits directly against the loan. Avoid using borrowed money to start new trades; paying down the loan regularly reduces your daily interest charge and can move you into a lower interest rate tier. Here's an example: A trader who reduces a $40,000 loan to $25,000 by depositing $15,000 upfront cuts daily interest from $8.77 to $5.48 at 8%, saving over $100 monthly. This savings accumulates over time, protecting profits instead of surrendering them to the broker.

5. Diversify Collateral and Use Stop-Loss Discipline

A concentrated portfolio on margin amplifies single-stock risk and triggers margin calls more quickly when holdings decline. Spread positions across uncorrelated assets so declines in one area don't threaten your entire account's equity ratio.

Why do stop-loss orders minimize how margin interest is calculated?

Pair this with strict stop-loss orders placed at entry to exit losing trades before they erode your capital and increase your effective borrowing cost. Disciplined exits keep the debit balance smaller for shorter periods. A trader who lets a losing position bleed for three weeks pays interest on borrowed funds that are actively losing value. Stop losses cut both the loss and the financing cost simultaneously.

6. Track Interest as a Line Item in Your Trading Journal

Most traders track entries, exits, and profit or loss, but ignore the financing cost inherent in leveraged trades. Add a column for margin interest paid per position, calculate it before entering the trade, and compare it against realized gains after closing. This visibility forces an honest evaluation of whether leverage improved returns or inflated position size while eroding net profit. When a $1,200 gain on a swing trade costs $180 in interest over two weeks, the setup's merit becomes questionable.

Why do profitable traders focus on true cost per trade?

Profitable traders know their true cost per trade, not just the headline number.

Related Reading

- Options Trading Strategies For Consistent Income

- Trading Cash Flow

- Recommended Prop Trading Firms With Growth Plans

- Best Trading Strategies For Consistent Profits

- Forex Trading Strategies For Consistent Profits

- Best Margin Rates Brokers

- How Does A Margin Loan Work

- How To Trade Forex With A Prop Firm

- Best Forex Prop Firm

- How To Become A Full-Time Trader

- How To Get Profit In Option Trading

- Margin Loan vs. Securities-Based Lending

- Day Trading Strategies For Consistent Profits

How Goat Funded Trader Helps Traders Manage Margin Interest Efficiently

Goat Funded Trader eliminates margin interest by providing simulated capital accounts up to $2 million after traders pass evaluation challenges. You trade firm capital with zero personal debit balance—no daily interest calculations, no compounding charges, and no erosion of profitable positions through financing costs. This shift from borrowing broker money to controlling funded capital removes the recurring expense that undermines leveraged strategies.

🎯 Key Point: With Goat Funded Trader, you never pay margin interest because you're trading the firm's capital, not borrowing money from a traditional broker.

"Trading with funded capital eliminates the daily erosion of profits through margin interest charges that can cost traders hundreds or thousands annually." — Proprietary Trading Industry Analysis, 2024

💡 Tip: The $2 million capital allocation means you can execute large position sizes without the interest burden that would make similar trades unprofitable with traditional margin accounts.

Zero Interest on Funded Capital

Traditional margin accounts charge interest the moment you borrow. Our simulated accounts at Goat Funded Trader require a minimum of $2,000 in equity to enter, then fund you with capital that carries no interest burden. A trader who previously borrowed $40,000 at a 9% annual rate paid $3,600 in financing costs each year. After funding with Goat Funded Trader, that same trader controls $100,000 or more with clean profit splits up to 100% and no deduction for carrying costs.

Fixed Risk Rules Replace Margin Calls

Margin accounts create cascading pressure through maintenance requirements and forced liquidations when equity drops. Our maximum loss thresholds are transparent: 4% daily drawdown limit and 6% total account drawdown cap. You know exactly where the boundaries are before entering any trade, with no surprise calls demanding emergency deposits. We absorb simulated losses beyond those thresholds, so your personal capital stays safe regardless of outcome. Traders shift from reactive scrambling to disciplined execution because the rules remain constant.

Fast Payouts Lock Gains Before Erosion

Margin interest compounds daily, reducing your net returns even on winning trades before withdrawal. Goat Funded Trader guarantees payment within 24 hours or pays you an additional $1,000, with standard payouts arriving in two business days. You can withdraw via bank transfer, crypto, Skrill, or local methods without margin drag cutting into your earnings. Every day, a profitable position sits in a traditional margin account, and financing costs erode your gains. Our funded accounts let you lock in realized profits immediately while keeping 80% to 100% of the total, depending on your selected add-on structure.

How do unlimited holding periods eliminate margin interest costs?

Weekend gaps and extended news events force margin traders into difficult choices: close early to stop interest buildup or hold through volatility while costs accumulate. Goat Funded Trader allows news trading and weekend positions with no time limits on funded accounts, so you execute full strategies without the interest penalty, pushing premature exits. A swing trade reaching the target in three weeks no longer costs you $200 in financing over that period. You trade the setup as designed, manage risk within firm parameters, and keep the entire profit when the position closes successfully.

Why does avoiding margin interest calculation reshape capital growth?

That decision—whether to spend the next year calculating daily interest or proving you can trade at scale without it—changes how capital grows in your account.

Get 25-30% off Today - Sign up to Get Access to Up to $800K Today

You now understand how margin interest builds up over time, how brokers charge different rates based on borrowing amount, and why daily charges affect the profitability of every trade you hold. The choice is simple: keep paying interest on borrowed money, or trade with money that costs you nothing.

🎯 Key Point: Margin interest can silently erode your trading profits through daily compounding charges that add up faster than most traders realize.

Goat Funded Trader removes margin interest entirely. Access up to $2 million in simulated capital, keep up to 100% of your profits, and withdraw earnings within 24 to 48 hours. No personal funds at risk. No daily interest eating into your positions. No margin calls forcing you to sell. Use code FIRSTGFT for 50% off your first challenge, or HBGFT for BOGO plus 50% off. One-time refundable fee. Instant access to apply everything you learned here.

"Access up to $2 million in simulated capital with no margin interest eating into your positions and keep up to 100% of your profits." — Goat Funded Trader Benefits

💡 Tip: Use promotional codes FIRSTGFT or HBGFT to maximize your savings on challenge fees while eliminating margin costs entirely.

Stop paying to borrow. Start trading with the leverage you deserve.

Be Great and get the App

.webp)