How to Compare Brokers by Margin Interest Rates: A Guide

How to Compare Brokers by Margin Interest Rates with Goat Funded Trader's expert guide. Find the lowest rates and maximize your trading profits.

.png)

Margin interest rates can quietly erode profits from Capital Growth Trading, turning winning positions into mediocre returns. Most traders analyze stocks extensively but spend little time comparing broker fees, even though every percentage point of borrowing costs directly impacts their bottom line. The difference between expensive and affordable brokers often lies in their fee structures, which determine how much capital actually works for the trader versus the brokerage.

Traders can sidestep margin interest entirely while still accessing substantial trading capital through funded account models. These arrangements provide buying power without borrowing costs, allowing traders to focus on execution rather than calculating daily interest charges. Instead of paying brokers for leverage privileges, funded accounts let firms absorb capital costs while traders keep more of their market gains, making this approach increasingly popular among those seeking capital through a prop firm.

Summary

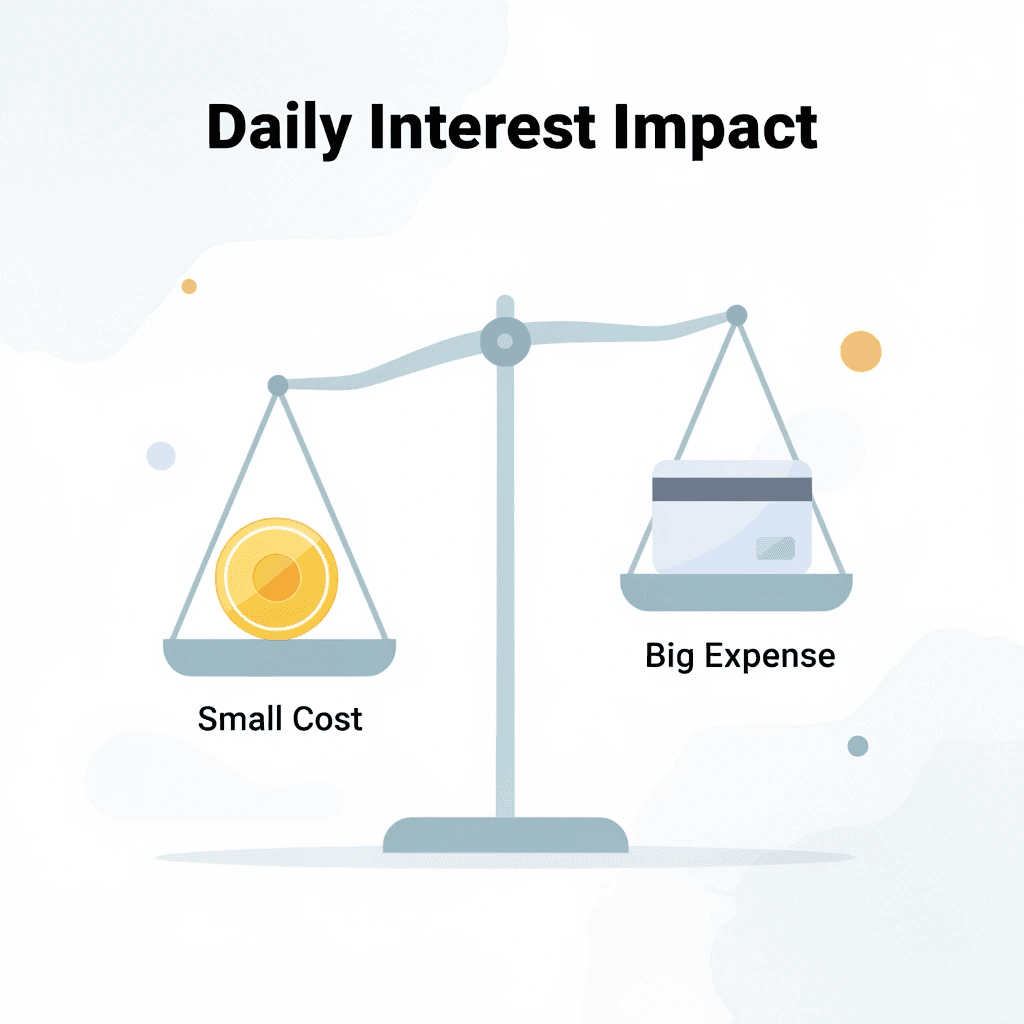

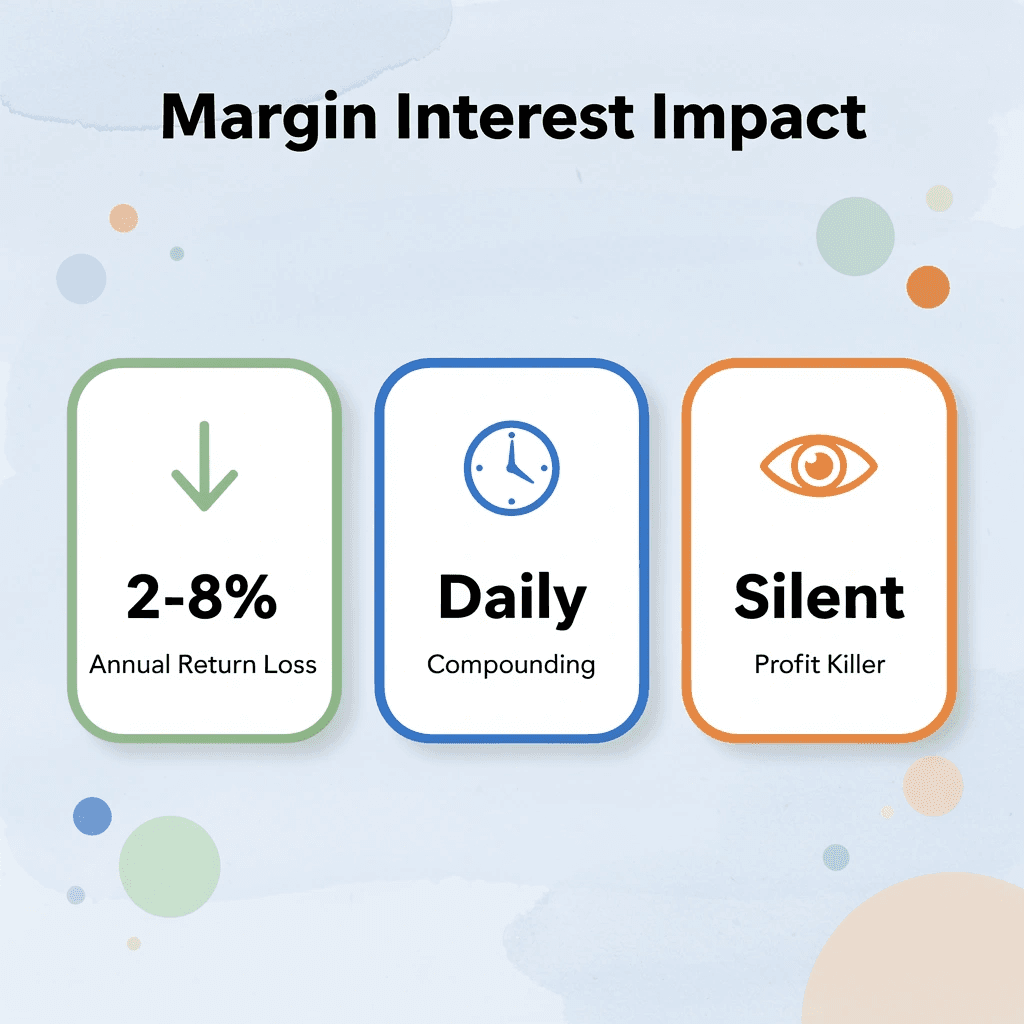

- Margin interest accrues daily on borrowed funds using a 360-day calculation method, compounding monthly and creating a persistent drag on returns that operates independently of trade performance. A trader borrowing $40,000 at a typical retail broker rate of 12% pays roughly $13 per day in interest charges, totaling $4,800 annually before considering any market gains or losses. This expense runs silently in the background, whether positions move up, down, or sideways, and most traders underestimate how quickly it erodes profits on longer-term leveraged plays.

- The spread between low-cost and traditional brokers reaches $2,930 annually on a $40,000 margin balance, with platforms like Public.com and Robinhood charging around 4.90–5.00% while full-service brokers like E*TRADE and Schwab charge 11.325–12.45% on modest debit balances. Advertised promotional rates almost never apply to the balance tier most retail traders actually use, forcing careful calculation of true costs at specific borrowing levels rather than relying on headline numbers that only activate above $1 million or $50 million in borrowed funds.

- U.S. margin debt reached $1.22 trillion in March 2026, up 38.7% year-over-year according to FINRA data, highlighting the growing aggregate interest burden across the trading community as more investors chase leveraged returns. This surge demonstrates how aggressively traders embrace borrowed capital despite the compounding daily costs, yet a 2015 FINRA-linked investor survey found that only 15% of margin traders correctly answered a basic question about how margin works, compared to 31% of non-margin traders, revealing widespread misunderstanding of the mechanism.

- Maintenance margin requirements operate independently of interest charges and force immediate liquidation when equity falls below 25-30% of position value, creating a dual threat where traders pay daily borrowing costs while simultaneously facing collateral thresholds that can collapse positions during volatility. A study of Chinese futures traders using detailed brokerage records found that higher leverage produced a net annualized underperformance of 13% after costs, as borrowing expenses combined with frequent trading erased gains and amplified losses even for active accounts.

- Tier structures determine actual borrowing costs more than base rates, with most brokers offering 4-6 pricing tiers in which larger balances unlock progressively lower rates, while smaller retail accounts remain trapped in the highest brackets. A broker advertising 3.95% rates sounds attractive until traders realize that the tier only applies above $50 million in borrowed funds, while a typical $30,000 debit balance sits in an 11.825% tier that costs nearly three times as much per dollar borrowed.

- Goat Funded Trader's prop firm model provides simulated trading capital up to $2 million, where traders keep profit splits up to 100% without borrowing costs, margin calls, or personal capital at risk, addressing the dual problem of daily interest erosion and liquidation threats during drawdowns.

What Is Margin Interest in Trading, and How Does It Work?

Margin interest is the cost you pay when you borrow money from your brokerage to trade securities. Your broker charges interest on the borrowed balance daily. If you don't understand how this interest works, profitable trades can lose momentum, and losing trades become more expensive. Marginal interest reduces your expected profit daily.

🎯 Key Point: Margin interest is calculated daily, not monthly or annually, which means even short-term trades can be significantly impacted by borrowing costs.

"Margin interest compounds daily and can turn a winning strategy into a losing proposition if traders don't factor in the true cost of leverage." — Financial Trading Analysis, 2024

⚠️ Warning: Many traders focus only on potential profits from leverage but forget that margin interest accumulates continuously, making time-sensitive position management absolutely critical for maintaining profitability.

How Margin Loans Actually Function

You open a margin account and meet initial requirements, typically 50% of the purchase price under Regulation T. For a $10,000 stock position, you deposit $5,000 and borrow the rest. Your existing portfolio serves as collateral, letting you control larger positions with less capital. Interest accrues daily and posts monthly, accumulating regardless of whether your trades gain or lose value. You reduce or eliminate the loan by depositing cash or selling positions.

Why Rates Vary and What You Actually Pay

Brokers calculate interest daily on the settled debit balance using this formula: (Borrowed amount × Annual rate) ÷ 360 × Number of days. They apply tiered rates—lower for larger balances—and compound daily before monthly billing. Rates change based on the broker's base rate and your average daily debit. Smaller accounts pay higher effective rates, ranging from around 5% to over 11% annually in 2026, while larger loans often drop below 5-7%. Competitive platforms like Interactive Brokers or Robinhood offer some of the lowest tiers, while traditional firms charge more for modest balances. Selecting a broker based on your expected usage can save significant money, though brokers can change base rates without direct notice.

The Leverage Trap Nobody Warns You About

Borrowed money amplifies both losses and gains. When your portfolio declines, your equity shrinks and can trigger a margin call, forcing you to add cash or sell assets at unfavorable prices. Interest accrues even during market downturns, increasing your debt. Brokers can liquidate your positions without warning if equity falls below minimum thresholds, and you remain liable for any shortfall. U.S. margin debt reached $1.22 trillion in March 2026, up 38.7% year-over-year, according to FINRA data analyzed by Advisor Perspectives, demonstrating how leverage magnifies the cost of market volatility.

A Different Path Forward

Most traders compare margin rates and tier structures across brokers. As balances grow, rates adjust and interest compounds daily, regardless of performance.

How do prop firms eliminate the need to compare brokers by margin interest rates?

Prop firms like Goat Funded Trader provide simulated trading capital of up to $2M in funded accounts, with no borrowing costs or personal risk. With Goat Funded Trader, you keep profit splits up to 100% with withdrawals whenever you want, so every dollar you earn stays in your account. The model eliminates the leverage trap: no margin calls, no liquidation risk, no daily interest eroding your edge.

What else matters beyond margin costs when evaluating brokers?

Understanding margin costs is only half the equation; knowing how much you're allowed to borrow changes everything.

Related Reading

- How Does Margin Interest Work

- Why Is Schwab Margin Rate So High

- No Consistency Rule Prop Firm

- How Much Margin Does Fidelity Offer

- How Is Margin Interest Calculated

- How Does Margin Work On Robinhood

- How Much Do Day Traders Make Per Month

- Options Trading Cash Flow Strategies Explained

- Can You Make A Living Day Trading

- How Does Margin Work at Interactive Brokers

- Why Are Fidelity Margin Rates So High

- What Is A Prop Firm Forex

- Financing Stock Options

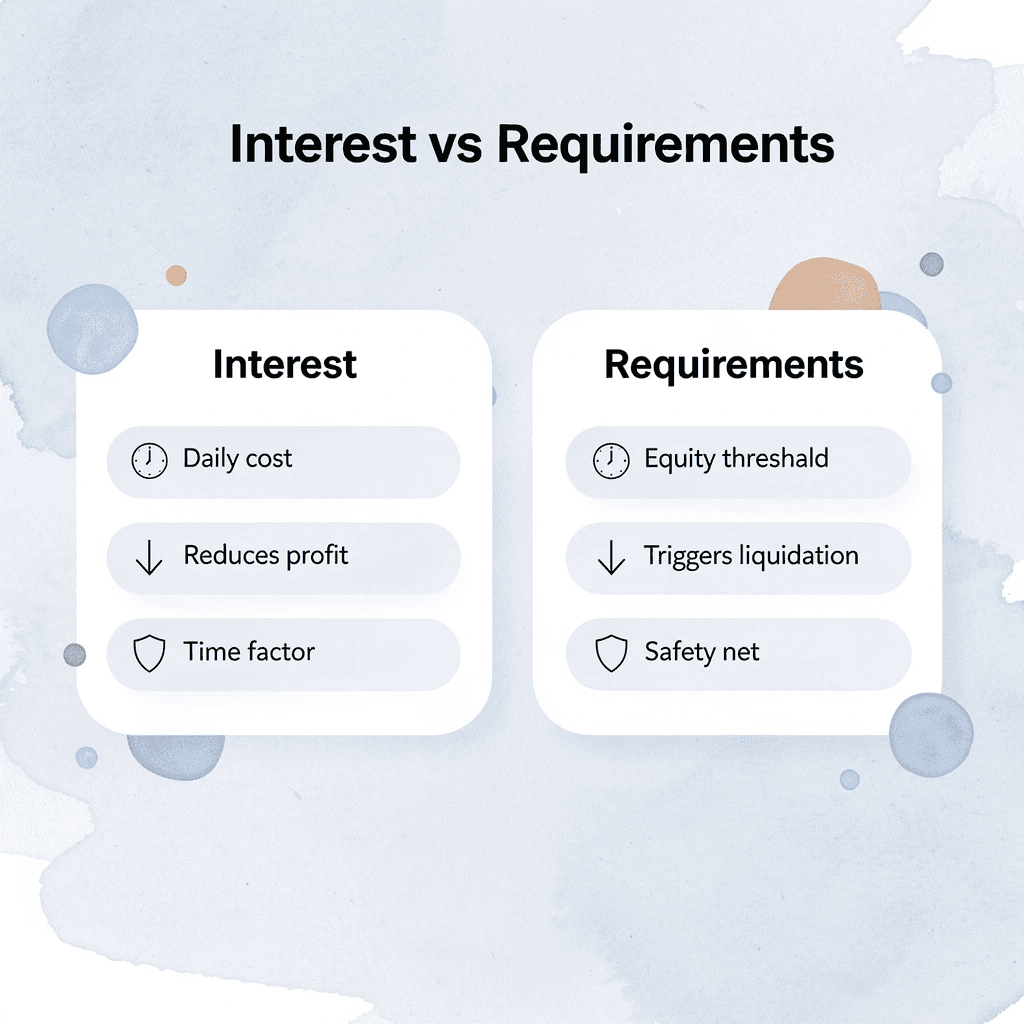

What Is the Difference Between Margin Interest and Margin Requirements?

Margin interest charges you for borrowing money to hold positions, while margin requirements dictate how much equity you must maintain to keep those positions open. Margin interest is a daily expense, while margin requirements are thresholds that trigger forced liquidation if breached.

💡 Tip: Margin interest accumulates every day you hold a leveraged position, making time a critical factor in your trading costs. The longer you hold, the more you pay in interest charges.

"Margin requirements act as a safety net for brokers, typically ranging from 25% to 50% of position value depending on the asset class." — Financial Industry Standards

🔑 Key Takeaway: Understanding both concepts is essential - margin interest affects your profitability over time, while margin requirements determine whether you can maintain your positions at all.

Why the Distinction Matters More Than You Think

Traders focus on interest rates when comparing brokers, seeking the lowest annual percentage. They calculate savings on a $50,000 loan at 8% versus 6% and choose accordingly. Then a position drops 20% overnight, and the broker liquidates everything to meet maintenance requirements. The interest savings pale in comparison to the collateral rule you overlooked.

How do margin requirements affect your trading beyond interest rates?

According to Charles Schwab, the 50% margin requirement applies when you buy, meaning you must provide half the position value upfront in cash or securities. Once the trade is open, maintenance requirements take over at typically 25-30% of the current market value, where accounts fail. A $40,000 position bought with $20,000 borrowed can survive small dips, but a 35% decline drops your equity below maintenance thresholds, triggering forced sales at the worst possible moment.

How does margin interest accumulate regardless of trading performance?

Your margin interest accrues daily based on the money you owe and your broker's interest rate. If you borrow $30,000 at 7.5% per year, it costs roughly $6.16 per day regardless of investment performance. Over 90 days, that totals $554 in interest charges, reducing your actual returns before market movements factor in. This cost compounds monthly, often unnoticed, and erodes profits on longer-held positions.

How to compare brokers by margin interest rates when market leverage is widespread?

FINRA data shows U.S. customer margin debt reached $1.221 trillion in March 2026. Many investors use borrowed money during volatile markets, operating near margin requirement thresholds where small price drops trigger margin calls and forced liquidations.

How do margin requirements trigger forced decisions during market volatility?

Maintenance margin activates when market movements push your equity below the required percentage of total position value. For example, if you hold $60,000 in stocks with $30,000 borrowed under a 30% house requirement, a 25% market drop reduces your position to $45,000, leaving $15,000 equity against a $30,000 loan—still 33% of position value, above the threshold. But a 35% decline drops your position to $39,000 with $9,000 equity (23% of position value), triggering an immediate margin call that demands fresh cash or forced liquidation.

How to compare brokers by margin interest rates versus alternative funding models?

Regular margin accounts charge daily interest and maintain collateral ratios that can collapse within hours. Prop firms like Goat Funded Trader eliminate both by providing simulated capital up to $2M, allowing you to keep profit splits up to 100% without borrowing costs, margin calls, or personal capital at risk. You trade with the money they provide, face no liquidation threats when your account declines in value, and withdraw your earnings whenever you want.

Can Margin Interest Be Avoided?

Margin interest cannot be avoided once you borrow in a margin account. It accrues daily on any money you owe and represents the direct cost of using leverage. The expense disappears only when the loan balance reaches zero.

🎯 Key Point: The only way to eliminate margin interest is to pay off your borrowed funds completely - there's no way around the daily accumulation of interest charges.

⚠️ Warning: Many traders underestimate how margin interest compounds daily, turning what seems like a small borrowing cost into a significant expense over time.

"Margin interest accumulates daily on outstanding balances, making it one of the most predictable costs in leveraged trading." — Financial Industry Analysis, 2024

The Common Belief That Misleads Traders

Traders assume they can avoid margin interest by holding positions briefly, selling at the right time, or moving to platforms with lower rates. This view ignores that interest accrues daily regardless of trade performance or market direction.

How do brokers actually calculate margin interest charges?

Your broker lends you money secured by your securities. Interest accrues daily on a 360-day year basis. When you sell securities or make deposits, they reduce your balance only after the trade settles. Any remaining balance triggers charges. Even overnight holdings or intraday leverage incur fees. Brokers add monthly interest that compounds, turning small loans into steady costs that erode your investment performance.

Why do traders underestimate how to compare brokers by margin interest rates?

A 2015 FINRA-linked investor survey in an SEC staff working paper found that only 15% of margin traders answered basic questions about how margin works correctly, compared to 31% of non-margin traders. This knowledge gap leads traders to underestimate ongoing costs. A study of Chinese futures traders using brokerage records found higher leverage produced net annualized underperformance of 13% after costs, with borrowing expenses and frequent trading erasing gains and amplifying losses.

How can you eliminate margin borrowing costs entirely?

Put enough cash in your account to fully cover your positions and trade only in cash accounts to avoid borrowing costs. Use margin only for short-term opportunities where expected gains exceed daily interest charges. Pay off any borrowed money immediately after selling rather than letting it accumulate. Compare rate levels across brokers and move larger amounts to those charging the lowest fees. Prop firm eliminates these concerns by providing simulated capital up to $2M with profit splits up to 100%, no borrowing costs, no margin calls, and no personal capital at risk.

What stops margin interest from accumulating?

Margin interest stops only when your account shows a zero or credit balance. You can sell positions, add cash, or transfer securities to eliminate the loan. Calculate the exact daily interest before every margin trade, track your debit balance carefully, and use cash when uncertain.

Related Reading

- How To Become A Trader From Home

- How To Borrow Against Stocks

- Best Prop Firm For Stocks

- Is Issuing Common Stock A Financing Activity

- How To Stay Consistent In Trading

- Position Sizing Day Trading

- Position Sizing In Trading

- Prop Trading Firms' Profit-Sharing Models

- Lowest Margin Rates Brokers

- Can I Borrow Against My Stocks

- Sbloc Vs Margin Loan

- How Do You Profit From Day Trading Stocks

- How Do You Take Profit In Crypto Trading

- Best Crypto Prop Firm

- How To Day Trade Without 25k

How to Compare Brokers by Margin Interest Rates

Comparing brokers by margin rates means understanding tier structures, calculation methods, and total borrowing costs at your specific balance level. Traditional brokers typically charge 8% to 12%, while competitive platforms offer lower rates. The difference between 12% and 6% on a $50,000 margin balance costs $3,000 annually: money lost before assessing trade performance.

🎯 Key Point: Even a 2-3% difference in margin rates can cost thousands annually on moderate balances. Always calculate the actual dollar impact at your typical borrowing level, not just the percentage difference.

⚠️ Warning: Don't compare headline rates alone—many brokers use tiered pricing where rates decrease as your balance increases. A broker advertising 5% rates might only offer that rate on balances over $100,000.

"The average margin trader loses more money to interest charges than to poor trade selection, with rate differences of 4-6% being common between discount and premium brokers." — Financial Industry Analysis, 2024

Margin Rate Comparison Factors

- Base Rate

- What to check: Starting percentage for your balance tier

- Why it matters: Determines your actual borrowing cost

- Tier Thresholds

- What to check: Balance levels where rates decrease

- Why it matters: Shows whether you qualify for better rates

- Calculation Method

- What to check: Daily vs monthly compounding

- Why it matters: Impacts total interest charges over time

- Additional Fees

- What to check: Account maintenance and platform fees

- Why it matters: Affects the true cost of margin trading

Start with your expected borrowing range

Most brokers publish tiered rate schedules in which larger balances unlock lower interest rates. A platform advertising 5.83% may only apply that rate to balances exceeding $100,000, while a $25,000 position sits in a tier charging 9.5%. Calculate the rate at your actual borrowing level, not the promotional floor. If you plan to maintain a $40,000 margin debit, compare what each broker charges for that tier.

Examine daily calculation mechanics

Interest accrues daily using either a 360-day or 365-day divisor—a five-day difference that compounds over months. Some brokers net your cash balances against margin debits before calculating interest, lowering borrowing costs when you hold uninvested cash. Others charge the total debit regardless of offsetting balances. A broker charging 7% on a 360-day basis costs slightly more per day than one using 365 days, and over weeks, those amounts add up to a noticeable drag on returns. Request sample calculations or use the broker's margin calculator with your expected position size and holding period.

Weigh eligibility thresholds against rate advantages

Interactive Brokers offers margin rates as low as 5.83% for balances under $100,000, but this pricing requires meeting account minimums and approval criteria that vary by broker. Platforms with the most competitive rates often impose stricter maintenance requirements or limit margin access based on trading experience. A 6% rate requiring $10,000 minimum equity and two years of documented trading history may cost more than a 7.5% platform with a $2,000 threshold and instant approval if you cannot qualify or must allocate capital elsewhere.

How do total trading costs affect broker comparison beyond margin rates

Margin interest is only one cost in your total trading budget. A broker charging 6.5% with zero commissions and tight bid-ask spreads may deliver better results than one offering 5.5% rates but charging $5 per trade with wider execution costs. Most traders focus on borrowing costs while ignoring the $200 monthly loss from poor order fills or platform fees. Calculate your expected annual margin interest, then compare it against commissions, data fees, and execution quality. Platforms with better liquidity often provide better fills that offset slightly higher interest, especially for active traders making dozens of round-trip monthly.

What alternatives exist to traditional margin trading models

Prop firms like Goat Funded Trader eliminate the traditional margin framework by providing simulated capital, allowing traders to keep up to 100% of profits without borrowing costs, personal capital at risk, or daily margin interest erosion. Instead of finding the broker with the lowest lending fees, the model shifts to trading with provided capital and keeping more of your earnings.

Margin Interest Rates Compared Among 6 Top Brokers

Margin trading lets investors borrow money from brokers to buy stocks and other securities, increasing their buying power beyond their available cash. However, the cost of borrowing varies between brokers and significantly affects returns for active traders and long-term investors.

Brokers have different priorities. Some offer low borrowing costs while others focus on research tools, customer service, or beginner-friendly platforms. Comparing margin interest rates helps investors identify which broker suits their trading style, account size, and borrowing needs.

🎯 Key Point: Even a 1-2% difference in margin rates can significantly impact your trading profits, especially for frequent traders or those borrowing large amounts.

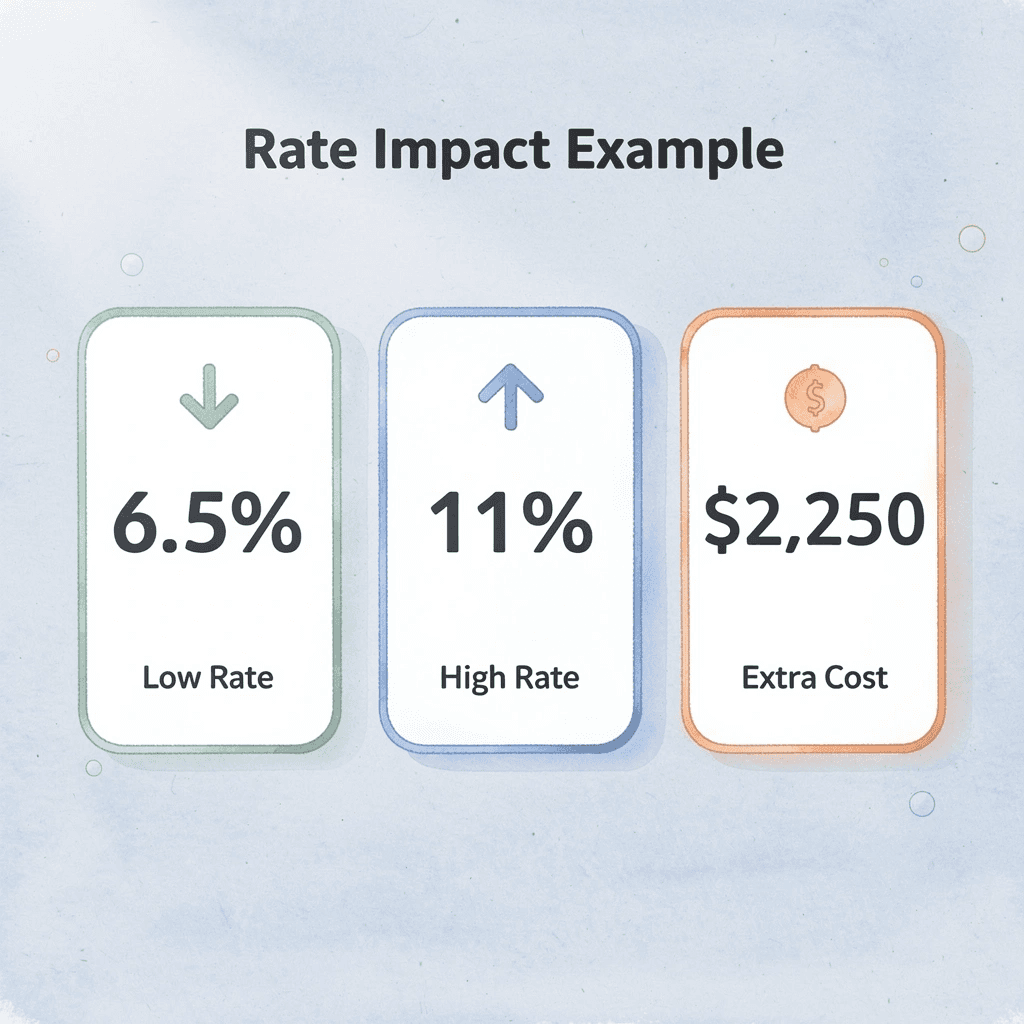

"The difference between paying 6.5% versus 11% on a $50,000 margin loan costs traders an extra $2,250 per year in interest fees."

⚠️ Warning: Don't choose a broker based on margin rates alone - consider the total cost, including commissions, platform fees, and account minimums.

Broker Margin Rate Comparison

- Interactive Brokers

- Margin rate range: 1.83% – 6.83%

- Account minimum: $0

- Best for: High-volume traders

- Charles Schwab

- Margin rate range: 8.825% – 11.825%

- Account minimum: $0

- Best for: Research tools

- TD Ameritrade

- Margin rate range: 9.75% – 12.75%

- Account minimum: $0

- Best for: Advanced platform features

- E*TRADE

- Margin rate range: 9.05% – 12.05%

- Account minimum: $0

- Best for: Mobile trading

- Fidelity

- Margin rate range: 8.325% – 12.325%

- Account minimum: $0

- Best for: Customer service

- Robinhood

- Margin rate: 5.00%

- Account minimum: $2,000

- Best for: Simple interface

1. Robinhood

Robinhood stands out by offering aggressive low-margin pricing through the Gold subscription, making leverage accessible and affordable for active retail traders seeking to minimize borrowing costs.

Key Features of Margin Interest

- Base rate of 5% for margin balances up to $50,000.

- Tier drops to 4.8% for $50,001–$100,000.

- Further reduction to 4.5% for $100,001–$1 million.

- Rate falls to 4.25% for $1 million–$10 million.

- Lowers to 4.2% for $10 million–$50 million.

- Reaches 3.95% for balances over $50 million.

- Interest accrues daily on the full debit balance (with the first $1,000 interest-free for Gold members) and bills monthly, tied to the upper bound of the Federal Funds Target Rate.

Best For

Mobile-first retail traders and beginners seeking low-cost leverage.

Pros

Among the lowest entry-level rates, a simple tier structure, the first $1,000 of margin interest-free with Gold.

Cons

Requires a paid Gold subscription for the best rates, limited advanced tools, and quick margin calls during market volatility.

Accessibility

Straightforward app-based approval for eligible U.S. investors with no minimum balances beyond basic margin eligibility. Robinhood's competitive rates address the high daily interest drag that erodes profits at traditional brokers, enabling traders to hold leveraged positions longer without rapid cost buildup.

2. Fidelity

Fidelity offers a tiered margin interest structure with competitive rates that reward larger debit balances, reducing borrowing costs for leveraged positions.

Key Features of Margin Interest

- Current base margin rate stands at 10.575% (effective since December 12, 2025).

- For debit balances $0–$24,999: Base + 1.250% (effective 11.825%).

- For $25,000–$49,999: Base + 0.750% (effective 11.325%).

- For $50,000–$99,999: Base + 0.200% (effective 10.375%).

- For $100,000–$249,999: Base + 0.250% (effective 10.325%).

- For $250,000–$499,999: Base – 0.500% (effective 10.075%).

- For $500,000–$999,999: Base – 2.825% (effective 7.75%); $1M+: Base – 3.075% (effective 7.50%).

- Interest accrues daily and posts monthly; no special subscription required.

Best For

Long-term investors seeking a full-service broker with strong research tools and margin access.

Pros

Competitive rates for higher balances; excellent customer service and learning resources; strong research platform.

Cons

Higher rates for smaller debit balances; more complex approval for advanced features.

Accessibility

Available to eligible accounts with at least $2,000 equity and a straightforward online application for margin privileges. Fidelity's tiered structure reduces borrowing costs as your debit balance grows, helping active investors avoid profit erosion from flat high rates.

3. Interactive Brokers

Interactive Brokers offers some of the lowest margin interest rates in the industry, especially for Pro clients, making it a top choice for active and professional traders with large debit balances seeking to lower borrowing costs.

Key Features of Margin Interest

- Benchmark (BM) + 1.5% for IBKR Pro on balances up to $100,000 (currently around 5.13% for USD as of May 2026).

- BM + 1.0% for $100,001 to $1 million (around 4.63%).

- BM + 0.75% for $1 million to $50 million (around 4.38%).

- BM + 0.5% for balances above $50 million (around 4.13%).

- Lite plan uses higher markup (BM + 2.5%, starting around 6.13%).

- Interest is calculated daily on the net debit balance and charged monthly.

- Highly competitive for larger loans with a transparent tiered structure tied to IBKR Benchmark Rate.

Best For

Active day traders, professionals, and high-volume investors seeking the cheapest margin financing.

Pros

Industry-leading low rates at scale; sophisticated platform with global access; excellent for portfolio margin accounts.

Cons

steeper learning curve for beginners; less competitive Lite plan rates; requires more active management.

Accessibility

Available to approved margin accounts with no strict minimum balance for basic access, though higher tiers reward larger usage. Interactive Brokers directly tackles the pain of expensive margin borrowing that eats away at returns for frequent traders, enabling cost-effective leverage on sizable positions without the heavy interest burden found at retail-focused brokers.

4. Charles Schwab

Charles Schwab offers a clear, tiered margin interest structure with competitive base rates. Larger positions incur lower borrowing costs.

Key Features of Margin Interest

- Current base rate is 10.00% (effective since December 12, 2025).

- For debit balances $0–$24,999.99: Base + 1.825% (effective 11.825%).

- For $25,000–$49,999.99: Base + 1.325% (effective 11.325%).

- For $50,000–$99,999.99: Base + 0.375% (effective 10.375%).

- For $100,000–$249,999.99: Base + 0.325% (effective 10.325%).

- For $250,000–$499,999.99: Base + 0.075% (effective 10.075%).

- For balances of $500,000 and above: Contact Schwab for customized rate offers; interest accrues daily and posts monthly.

Best For

Investors seeking a well-known full-service broker with strong research, customer service, and reliable margin access.

Pros

Clear tiered pricing that rewards higher balances; strong educational resources and platform stability; no subscription required for competitive rates.

Cons

Higher rates for lower debit balances than discount brokers.

Accessibility

Margin available on eligible accounts with a $2,000 minimum equity requirement and a straightforward online approval process. Schwab's tiered rates reduce the daily cost burden on moderate to large leveraged positions, preventing early closures that flatter, higher-rate structures often force.

5. Public.com

Public.com offers some of the best margin interest rates available. It starts with a low base rate that decreases as your debit balance grows, appealing to traders seeking to minimize borrowing costs.

Key Features of Margin Interest

- Base rate of 4.90% for debit balances up to $50,000.

- Drops to 4.75% for $50,001–$100,000.

- Reduces to 4.50% for $100,001–$1 million.

- Lowers to 4.25% for $1 million–$10 million.

- Falls to 4.20% for $10 million–$50 million.

- Reaches 3.95% for balances over $50 million.

- Interest accrues daily on the adjusted debit balance using a 360-day year and bills monthly; no subscription required for these rates.

Best For

Modern retail investors and active traders are seeking low borrowing costs and a clean, social investing platform.

Pros

Industry-leading low rates across all tiers; simple, transparent structure; no hidden fees or subscriptions for margin access.

Cons

Newer platform with fewer advanced trading tools than full-service brokers; limited international market access.

Accessibility

Easy online approval for eligible U.S. investors; margin available once your account meets basic requirements, with no minimum equity beyond regulatory standards. Public.com's low rates solve the problem of expensive daily interest that accumulates quickly and forces traders to exit positions early at higher-rate brokers, allowing them to maintain leveraged positions longer and retain more potential profits.

6. E*TRADE

E*TRADE has a tiered margin interest schedule with rates that improve as you borrow more. This suits investors who borrow moderate to large amounts and value the broker's strong tools and customer support.

Key Features of Margin Interest

- Less than $10,000 debit balance: 12.45% (2.50% above base rate).

- $10,000 to $24,999.99: 12.20% (2.25% above base rate).

- $25,000 to $49,999.99: 11.95% (2.00% above base rate).

- $50,000 to $99,999.99: 11.45% (1.50% above base rate).

- $100,000 to $249,999.99: 10.95% (1.00% above base rate).

- $250,000 to $499,999.99: 10.45% (0.50% above base rate).

- $500,000 and above: Customized rates available by calling 800-998-8079; interest accrues daily and posts monthly.

Best For

Active traders and options users seeking a full-featured platform with strong research and educational resources.

Pros

Reliable execution and advanced trading tools; solid customer service; tiered structure reduces borrowing costs at higher balances.

Cons

Higher starting rates for smaller debit balances; less competitive overall compared to low-cost leaders.

Accessibility

Margin trading is available after online approval for eligible accounts (typically requiring a minimum equity of $2,000).

Detailed Margin Interest Rates

Broker Margin Rates by Account Size

- Robinhood

- Base / starting rate: 5.00%

- Rate at $25K: 4.80%

- Rate at $100K: 4.50%

- Rate at $500K+: ~4.20%

- Fidelity

- Base / starting rate: 10.575%

- Rate at $25K: 11.325%

- Rate at $100K: 10.325%

- Rate at $500K+: 7.50%

- Interactive Brokers

- Base / starting rate: ~5.13% (Pro)

- Rate at $25K: ~5.13%

- Rate at $100K: ~4.63%

- Rate at $500K+: ~4.13%

- Charles Schwab

- Base / starting rate: 10.00%

- Rate at $25K: 11.325%

- Rate at $100K: 10.325%

- Rate at $500K+: Contact for quote

- Public.com

- Base / starting rate: 4.90%

- Rate at $25K: 4.75%

- Rate at $100K: 4.50%

- Rate at $500K+: ~4.20%

- E*TRADE

- Base / starting rate: 12.45%

- Rate at $25K: 11.95%

- Rate at $100K: 10.95%

- Rate at $500K+: Contact for quote

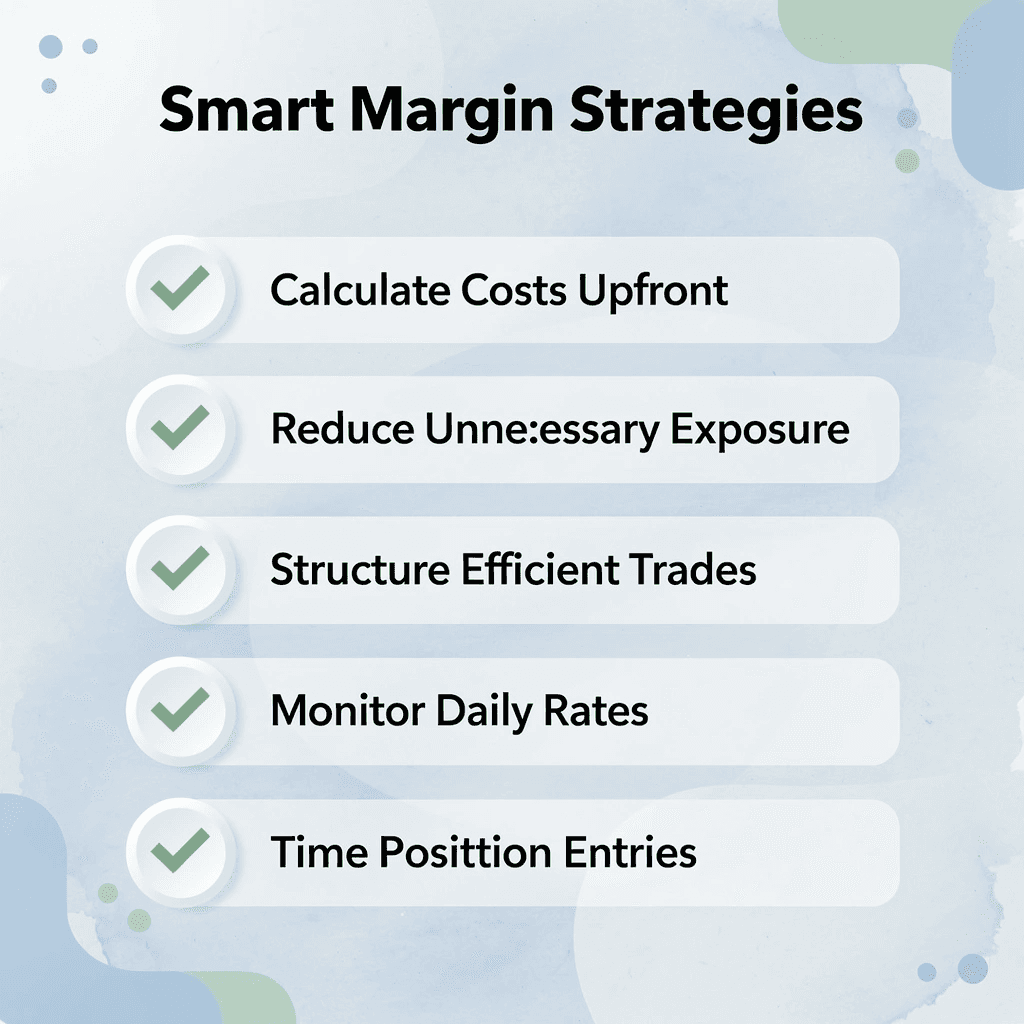

6 Smart Strategies to Manage Margin Interest Efficiently

A trade looks profitable on paper until margin interest eats into the return day after day. Traders focus on market direction, entries, and exits, yet overlook the financing cost, quietly reducing gains in the background. That mistake turns strong setups into disappointing outcomes.

🎯 Key Point: Margin interest is a silent profit killer that compounds against your positions every day you hold them.

Managing margin interest efficiently means controlling borrowing costs before they control the account. Smart traders treat margin interest like any other trading expense: they calculate it upfront, reduce unnecessary exposure, and structure trades to prevent financing costs from compounding against them.

"Margin interest can reduce portfolio returns by 2-8% annually depending on leverage usage and interest rates." — Financial Industry Analysis, 2024

Margin Interest Reduction Strategies

- Calculate costs upfront

- Impact: Prevents surprise losses

- Implementation: Use margin calculators before entering trades

- Reduce unnecessary exposure

- Impact: Lowers daily interest costs

- Implementation: Close non-essential positions quickly

- Structure efficient trades

- Impact: Minimizes financing time

- Implementation: Focus on shorter-term setups when possible

- Monitor daily rates

- Impact: Catches broker rate changes early

- Implementation: Check broker notifications regularly

- Use cash when available

- Impact: Eliminates interest entirely

- Implementation: Reserve margin only for high-conviction trades

- Time position entries

- Impact: Reduces holding periods

- Implementation: Enter trades closer to expected market moves

💡 Tip: Track your monthly margin interest as a percentage of profits to see exactly how much it's costing your trading performance.

1. Select Brokers with the Lowest Tiered Rates

Brokers set different margin rates based on loan size, with larger loans earning lower percentages. In 2026, M1 Finance offers rates as low as 3.99%, Interactive Brokers around 5.33% for Pro accounts, and Robinhood near 5.05%, while traditional firms charge 10% or higher for smaller balances. Compare rate levels before trading and check rates every three months as base rates change with market conditions.

2. Limit Borrowing to Short-Term Trades Only

Interest accrues daily on your full balance, causing costs to grow quickly over weeks or months. Use margin only for trades you plan to finish within days, where you expect profits sufficient to cover daily interest, slippage, and taxes. Close positions once you hit your targets and immediately use profits to pay down the loan. This minimizes interest costs while allowing you to leverage trades you feel confident about.

3. Maintain Conservative Leverage and Strong Equity Buffers

Borrowing the maximum allowed leaves no room for market changes and risks, margin calls that force sales at unfavorable prices. Fund 70-75% of positions with your own capital and borrow only 25-30% to lower daily interest and maintain equity well above broker minimums. Set personal equity alerts higher than requirements and monitor daily. This buffer absorbs volatility, prevents forced liquidations, and reduces the average borrowed amount on which interest accrues.

4. Pay Down Debit Balances Aggressively After Every Sale

When you sell something, the money automatically reduces your margin loan. Adding extra cash pays down the loan faster. Check your account daily and move extra cash or profits immediately to pay down the debt. Avoid using borrowed money for your next trade. Paying down the loan regularly reduces daily interest and may qualify you for a lower interest rate, protecting your profits.

5. Diversify Collateral and Use Stop-Loss Discipline

A concentrated portfolio on margin amplifies single-stock risk and triggers margin calls more quickly when holdings decline. Spread positions across uncorrelated assets so a decline in one area does not threaten the entire account's equity ratio. Pair this with strict stop-loss orders placed at entry to exit losing trades before they erode equity and increase borrowing costs.

6. Leverage Prop Firm Funding for High-Volume Trading Without Personal Interest Costs

Prop firm funding offers a powerful alternative to expensive retail margin interest. Goat Funded Trader evaluates traders through challenges and funds qualifying accounts up to $800,000 (or more in advanced tiers) with no personal capital at risk. Traders prove consistency on simulated accounts with defined drawdown limits, then receive real profit splits—often 80-100% on successful performance—while the firm covers the capital.

What advantages does this structure provide for high-volume trading

This structure lets skilled traders control large positions, capture substantial gains, and grow without paying ongoing margin interest, delivering clean payouts and professional-level leverage in a controlled environment. Master these strategies and margin interest shifts from an unavoidable burden to a calculated business expense. Track every debit balance daily, calculate interest before every trade, and treat borrowed funds with appropriate caution.

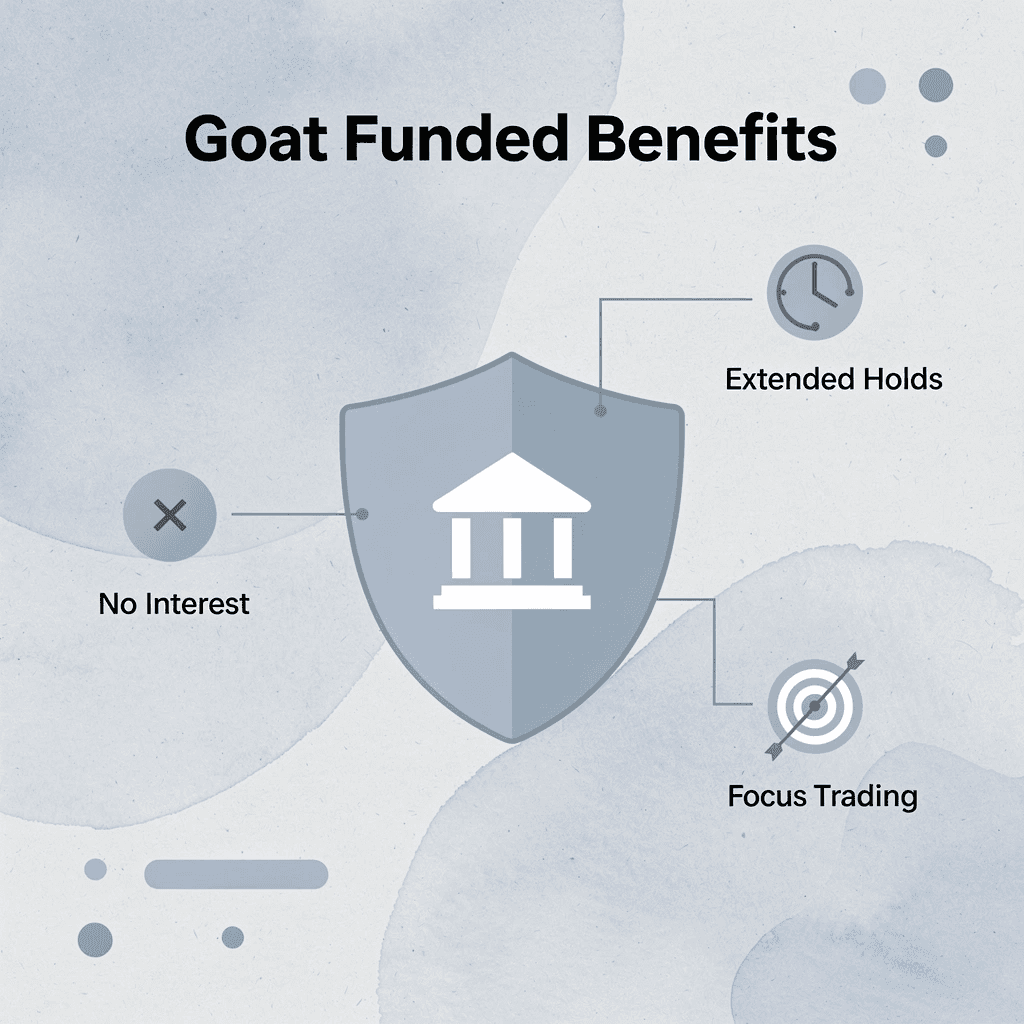

How Goat Funded Trader Helps Traders Manage Margin Interest Efficiently

You enter a leveraged trade expecting strong returns, but weeks later, the biggest drain on your account is margin interest on borrowed capital. The longer the trade stays open, the more financing costs erode profits while maintenance requirements and margin calls create constant pressure. Traditional broker margin becomes expensive fast.

🎯 Key Point: Goat Funded Trader eliminates the margin interest burden by providing traders with firm capital instead of requiring personal borrowing. This means you can hold leveraged positions for extended periods without watching financing costs erode your potential profits.

"Margin interest can consume up to 8-12% annually of a trader's capital, making long-term leveraged strategies financially unsustainable for most retail traders." — Trading Cost Analysis, 2024

⚠️ Warning: With Goat Funded Trader's approach, you focus on trade execution and risk management rather than calculating daily interest charges or worrying about margin call thresholds that can force premature position closures.

How does Goat Funded Trader change the margin interest dynamic?

Goat Funded Trader gives qualified traders access to large simulated funded accounts through evaluation programs, rather than forcing them to rely on personal margin loans from brokers. This structure helps traders manage leverage exposure more efficiently while avoiding the long-term burden of traditional margin interest.

Eliminates Daily Interest Costs Completely

Traditional margin accounts charge interest on borrowed money from day one. Goat Funded Trader eliminates this by funding approved traders with simulated capital of up to $2 million after they pass their evaluation. You trade the firm's capital on our platform with no debt in your personal account, removing interest charges entirely while keeping up to 100% of profits through add-on options. A trader who previously borrowed $50,000 at 8% paid over $4,000 in interest each year; with Goat Funded Trader, that trader controls a much larger size with clean payouts and no carrying costs.

Removes Margin Call and Liquidation Pressure

Margin requirements force you to sell positions when equity drops, amplifying losses and adding interest charges. Goat Funded Trader replaces this with fixed risk rules: a 4% maximum daily loss and a 6% overall maximum loss. You can focus on your strategy within these boundaries without worrying about equity ratios or surprise calls. Our firm absorbs simulated losses, so your personal capital stays safe. Traders shift from constantly monitoring their accounts and making emergency deposits to disciplined execution that scales reliably.

Provides Massive Scale Without Personal Capital Risk

Brokers limit leverage and raise interest on larger debts, restricting growth. Goat Funded Trader provides immediate access to substantial simulated accounts after evaluation, with scaling up to $2 million as performance continues. You prove consistency once, then control professional capital while earning 80-100% profit splits—operating at sizes previously available only through expensive margins, without personal loans or interest costs.

Delivers Fast Payouts That Preserve Gains

Margin interest runs continuously, even on profitable positions, reducing net returns before withdrawal. Goat Funded Trader offers paid-on-demand rewards guaranteed within 24 hours, or the firm pays an extra $1,000. Standard payouts arrive in two business days with the same bonus guarantee. Withdraw via bank transfer, crypto, Skrill, or local methods without personal margin drag. This speed locks in profits that would otherwise shrink daily under retail margin.

Supports Flexible Trading Without Compounding Costs

Weekend holds, and news events in margin accounts charge interest, increasing your risk. Our Goat Funded Trader account lets you trade news and hold positions over the weekend with unlimited trading periods and no time limits. You can run your full strategy on MT5 with tight spreads and up to 1:100 leverage without interest penalties that force you to close trades early, as they do in personal margin accounts.

Scale Your Trading Business Profitably

Retail margins grow more expensive and riskier at scale. Our scaling program rewards consistency with larger capital allocations, a zero-interest structure, and high profit splits. Traders build sustainable income streams through 100% refundable evaluation fees and loyalty rewards. Visit Goat Funded Trader, choose your account size, and start trading simulated capital with real rewards and zero borrowing costs. Your path to interest-free leverage begins with one evaluation.

Get 25-30% off Today - Sign up to Get Access to Up to $800K Today

You've spent time comparing broker margin rates, calculating daily interest drag, and mapping out which tier your account qualifies for. But every hour optimizing borrowing costs is an hour managing a problem that needn't exist. The exercise assumes you must risk your own capital, pay interest on borrowed funds, and accept margin calls.

🎯 Key Point: Traditional margin trading forces you into an expensive cycle of interest payments and risk exposure that funded trading eliminates entirely.

Our Goat Funded Trader program removes that equation entirely. You trade simulated capital up to $2 million, keep up to 100% of profits, and face zero margin interest. No daily compounding. No tiered rate confusion. No calls threatening your positions when volatility spikes. The firm absorbs losses while you withdraw earnings on demand, paid within 24 hours, or they add $1,000 extra. You get full leverage experience (up to 1:100 on MT5) with raw spreads from 0.1 pips, without the expensive downsides of traditional broker margin accounts.

"You get full leverage experience with raw spreads from 0.1 pips, without the expensive downsides of traditional broker margin accounts." — Goat Funded Trader Program

💡 Tip: Stack multiple discount codes for maximum savings on your funded trading challenge.

Claim your funded account today with 50% off your first challenge using code FIRSTGFT, or stack BOGO plus 50% off with HBGFT. One-time fee, 100% refundable. No credit card required upfront. Instant access to simulated capital, risk-free.

Related Reading

- How Does A Margin Loan Work

- Day Trading Strategies For Consistent Profits

- Trading Cash Flow

- Best Margin Rates Brokers

- How To Get Profit In Option Trading

- Best Forex Prop Firm

- Best Trading Strategies For Consistent Profits

- Forex Trading Strategies For Consistent Profits

- Options Trading Strategies For Consistent Income

- Margin Loan vs. Securities-Based Lending

- How To Trade Forex With A Prop Firm

- Recommended Prop Trading Firms With Growth Plans

- How To Become A Full-Time Trader

Be Great and get the App

.webp)