Margin Loan vs Securities-Based Lending: Which is Safer

Margin Loan vs Securities Based Lending comparison: Goat Funded Trader breaks down risks, costs, and safety factors to help you choose wisely.

.png)

Investment portfolios can unlock borrowing power through margin loans or securities-based lending, two distinct approaches that let investors access cash without selling their holdings. Both methods within Capital Growth Trading offer liquidity, but they differ significantly in collateral requirements, interest rates, lending limits, and risk factors. Understanding these differences helps investors choose the option that best protects their wealth while meeting their cash needs.

The choice between these lending options becomes less critical when considering alternative approaches to accessing trading capital. Rather than pledging personal holdings as collateral and risking margin calls or forced liquidations, traders can pursue growth opportunities through a prop firm that provides substantial capital without personal financial exposure.

Key Takeaways

- Securities-backed lines of credit isolate your investment strategy from your cash needs by prohibiting the use of borrowed funds for the purchase of additional securities. This structural restriction eliminates the temptation to amplify positions during optimistic market runs, keeping your original portfolio allocation intact. Lenders set advance rates conservatively, typically 50% to 70% for equities and up to 95% for U.S. Treasuries, leaving a significant equity cushion before any maintenance action becomes necessary. Most institutions provide 30 to 90 days' notice before requiring additional collateral or asset sales, giving you time to adjust without panic-driven decisions that lock in losses.

- Margin loans amplify both gains and losses symmetrically through leverage, which punishes volatility. When you borrow $10,000 to buy $20,000 worth of stock, a 10% gain becomes a 20% return on your equity, but a 10% loss also doubles to 20%. If the stock drops 30%, you've lost 60% of your initial stake while still owing the full $10,000 loan plus accumulated interest. Brokers monitor accounts continuously under Regulation T rules, requiring at least 25% equity maintenance, and many firms reserve the right to liquidate positions immediately during volatile sessions without waiting for your response.

- The Federal Reserve Board estimated that securities-based loans outstanding totaled $200 billion to $300 billion as of 2024, reflecting growing recognition that non-purpose lending reduces systemic leverage risk relative to traditional margin borrowing. During the 2022 bear market, margin debt across U.S. brokerages plummeted 27% by June from its October 2021 peak, reflecting forced liquidations that locked in losses for thousands of investors. SBLOC balances remained far more stable over the same period because borrowers used the funds for real estate purchases, business expenses, or bridge financing rather than piling into declining equity positions.

- Margin loans charge interest daily on your outstanding balance, calculated and billed monthly at rates that typically run below credit cards but above mortgages. If you borrow $10,000 at 8% annually, you pay roughly $800 per year, or about $2.19 per day. That cost runs regardless of whether your thesis plays out, and three months of holding costs you $200 before your position even moves. A 5% gain on a leveraged position might net only 2% after interest costs, especially if you hold through multiple billing cycles, and the erosion accelerates on losing trades where you pay borrowing costs on positions that are simultaneously declining in value.

- The FINRA Foundation's 2021 National Financial Capability Study found that 7% of investors overall have experienced a margin call, with younger investors under 35 at 23%. Forced liquidations strip control at the worst possible moments, leaving you unable to choose which positions to exit, when to sell, or how to manage tax consequences. Brokers liquidate whatever covers the shortfall fastest, often triggering capital gains taxes on appreciated holdings while your declining positions remain. The speed of intervention differs sharply between margin accounts and SBLOCs because margin lenders prioritize protecting their capital in fast-moving markets.

- Goat Funded Trader offers traders access to simulated capital accounts of up to $2 million without pledging personal assets as collateral, removing the risk of margin calls and the interest costs associated with traditional borrowing, while allowing traders to keep up to 100% of profits generated through performance-based evaluation.

What Is a Margin Loan, and How Does It Work?

A margin loan is money you borrow from your brokerage, secured by the stocks you already own. The broker lends you cash based on your portfolio value, letting you buy more stocks, bonds, or ETFs without selling existing holdings. You pay interest on the borrowed amount, and if your account value drops sufficiently, the broker can sell your positions without asking. It's leverage that amplifies both your gains and losses.

🎯 Key Point: Margin loans use your existing securities as collateral, allowing you to access additional buying power while maintaining your current positions.

Margin Loan Overview

- Collateral

- Your existing stocks and securities

- Loan amount

- Based on portfolio value (typically 50–90%)

- Interest rate

- Variable rate charged on the borrowed amount

- Risk factor

- Forced liquidation can occur if the account falls below maintenance margin

"Margin trading amplifies both potential returns and potential losses, making it a double-edged sword that requires careful risk management." — Financial Industry Regulatory Authority

💡 Example: If you own $10,000 worth of stocks, your broker might lend you $5,000-$9,000 to purchase additional securities, with your original holdings serving as collateral for the loan.

How do brokers determine your borrowing capacity?

When you open a margin account, your broker assesses which securities can serve as collateral. Stocks, bonds, and ETFs typically qualify, though not all assets count equally. According to Charles Schwab, brokers generally lend up to 50% of the value of eligible securities, meaning a $20,000 portfolio might unlock $10,000 in borrowing capacity. The money appears in your account immediately, with no credit check or lengthy approval process.

Why choose margin loans over selling existing positions?

The appeal is obvious: you can act on a setup immediately while keeping your portfolio intact. Selling would trigger capital gains taxes and force you to abandon holdings you still want. Margin lets you double down on conviction without liquidating carefully chosen positions.

How do daily interest charges impact your trading costs?

Margin loans charge interest daily on your outstanding balance, billed monthly. Rates vary by broker and loan size, typically organized into tiers, with larger balances earning lower rates: below credit card rates but above mortgage or auto loan levels. Borrowing $10,000 at 8% annually costs roughly $800 per year, or about $2.19 per day. This seems manageable until your trade takes longer than expected. Three months of holding costs $200 before your position moves. If the stock drops instead of rising, you're paying interest on a losing trade, compounding the damage.

Why do traders underestimate interest erosion on returns?

Many traders underestimate how quickly interest reduces returns. A 5% gain on a leveraged position might yield only 2% after interest costs, especially over multiple billing cycles. The meter runs regardless of the outcome.

What are the margin thresholds that trigger maintenance requirements?

Brokers enforce two margin thresholds: initial margin (typically 50%, determining how much of a new purchase you must pay for) and maintenance margin (usually 25% to 30%, setting the minimum equity you must maintain). If your portfolio value falls below the maintenance level, you receive a margin call. The broker requires you to add cash, deposit securities, or sell positions to restore the required equity ratio. You typically have two to five days to comply, though brokers can act faster in volatile markets.

How does forced liquidation impact Margin Loan vs Securities-Based Lending outcomes?

If you can't meet the call, the broker sells your holdings to cover the debt, choosing which positions to sell, often at the worst moment when prices have already dropped. You lock in losses with no chance to recover. According to the FINRA Foundation's 2021 National Financial Capability Study Investor Survey, 7% of investors overall have experienced a margin call, with 23% of investors under 35 reporting the same. This is a predictable outcome of leverage meeting volatility.

How does leverage amplify both gains and losses in trading?

Leverage works both ways. Borrow $10,000 to buy $20,000 worth of stock, and a 10% gain becomes a 20% return on your $10,000 equity. But a 10% loss also doubles to 20%, and if the stock drops 30%, you've lost 60% of your initial stake while still owing the full $10,000 loan plus accumulated interest. Markets move against confident positions all the time, and margin loans convert temporary drawdowns into permanent capital destruction when brokers force sales at the worst moments.

What makes margin loans vs securities-based lending different in risk management?

Traditional margin loans require you to risk your own portfolio as collateral and absorb every dollar of loss when trades go wrong. A margin call during a market correction forces you to sell investments at the worst time. Platforms like Goat Funded Trader work differently: you trade with practice capital accounts up to $2 million, keep 100% of the profits you make, and risk no personal capital. Your portfolio stays safe, and no margin call can wipe out your savings. But there's a reason brokers offer margin so readily.

What Is Securities-Based Lending, and How Does It Work?

A Securities-Backed Line of Credit (SBLOC) lets you borrow cash using your investment portfolio as collateral without selling shares. You keep ownership, continue collecting dividends and capturing growth, and access money for nearly any purpose except buying more securities. Lenders provide a revolving credit line based on a percentage of your portfolio's value, charging interest only on what you draw.

🎯 Key Point: SBLOCs provide immediate liquidity while preserving your long-term investment strategy and avoiding taxable events from selling securities.

"Securities-based lending allows investors to unlock the value of their portfolios without disrupting their investment strategy or triggering capital gains taxes." — Financial Planning Association, 2023

💡 Example: If you have a $500,000 portfolio, you might qualify for a $250,000-$350,000 credit line (typically 50-70% of portfolio value), paying interest only on amounts you use.

What Assets Qualify as Collateral

Eligible collateral includes publicly traded stocks, bonds, mutual funds, ETFs, and cash equivalents held in taxable brokerage or trust accounts. Retirement accounts like IRAs don't qualify due to IRS restrictions. Lenders evaluate assets based on liquidity and volatility: stable holdings like U.S. Treasuries support higher advance rates than individual stocks. You can pledge multiple accounts to increase your available line.

How Lenders Calculate Your Borrowing Power

Lenders determine your credit line using advance rates, which Amerant Bank notes typically range from 50% to 95% of portfolio value, depending on your assets and their risk profile. All-cash or low-volatility portfolios can reach 95%, while diversified equity portfolios might allow 50% to 70%. The line remains flexible: draw what you need, repay principal anytime to restore borrowing power, and borrow again without reapplying. Income verification is typically not required for qualified borrowers.

The Application and Funding Process

The process starts with pledging your securities, followed by a review that typically finishes within a few business days to two weeks. Approved funds are ready to use, with no fees for unused funds. You can still trade in pledged accounts, though lenders check values daily to maintain collateral ratios within limits. The setup involves less paperwork than traditional loans and, in most cases, no origination or annual maintenance fees. You pay interest only on the amount you draw.

Interest Rates and Repayment Flexibility

Interest accrues only on the amount you borrow at variable rates, which are typically tied to SOFR plus a spread that decreases with larger borrowing amounts. Spreads can reach as low as 1.90% on lines over $3 million. Each month, you pay only interest, with no required schedule for repaying principal.

You control when you pay back the money, paying down as your cash flow allows while your portfolio stays invested. This setup appeals to investors who want to keep their market exposure during periods when Federal Reserve estimates show securities-based loans outstanding reached $138 billion as of Q1 2024, representing 2.7% of total U.S. consumer credit.

What flexibility risks do most investors overlook?

The real question is whether the flexibility of SBLOCs comes with risks most investors don't anticipate.

Related Reading

- Options Trading Cash Flow Strategies Explained

- How Much Margin Does Fidelity Offer

- Why Are Fidelity Margin Rates So High

- Can You Make A Living Day Trading

- How Does Margin Interest Work

- How Does Margin Work On Robinhood

- What Is A Prop Firm Forex

- How To Compare Brokers By Margin Interest Rates

- No Consistency Rule Prop Firm

- Why Is Schwab Margin Rate So High

- How Does Margin Work at Interactive Brokers

- How Much Do Day Traders Make Per Month

- How Is Margin Interest Calculated

- Financing Stock Options

Are Securities-Based Lending Safer Than Margin Loans?

SBLOCs deliver structural safety advantages over margin loans because they prohibit investment leverage and use more conservative collateral ratios. Margin loans multiply your market exposure by letting you buy additional securities on credit, compounding losses during downturns, whereas SBLOCs provide cash for non-investment purposes while keeping your portfolio exposure unchanged.

🎯 Key Point: Unlike margin loans that amplify risk through leverage, SBLOCs maintain your original portfolio allocation while providing liquidity.

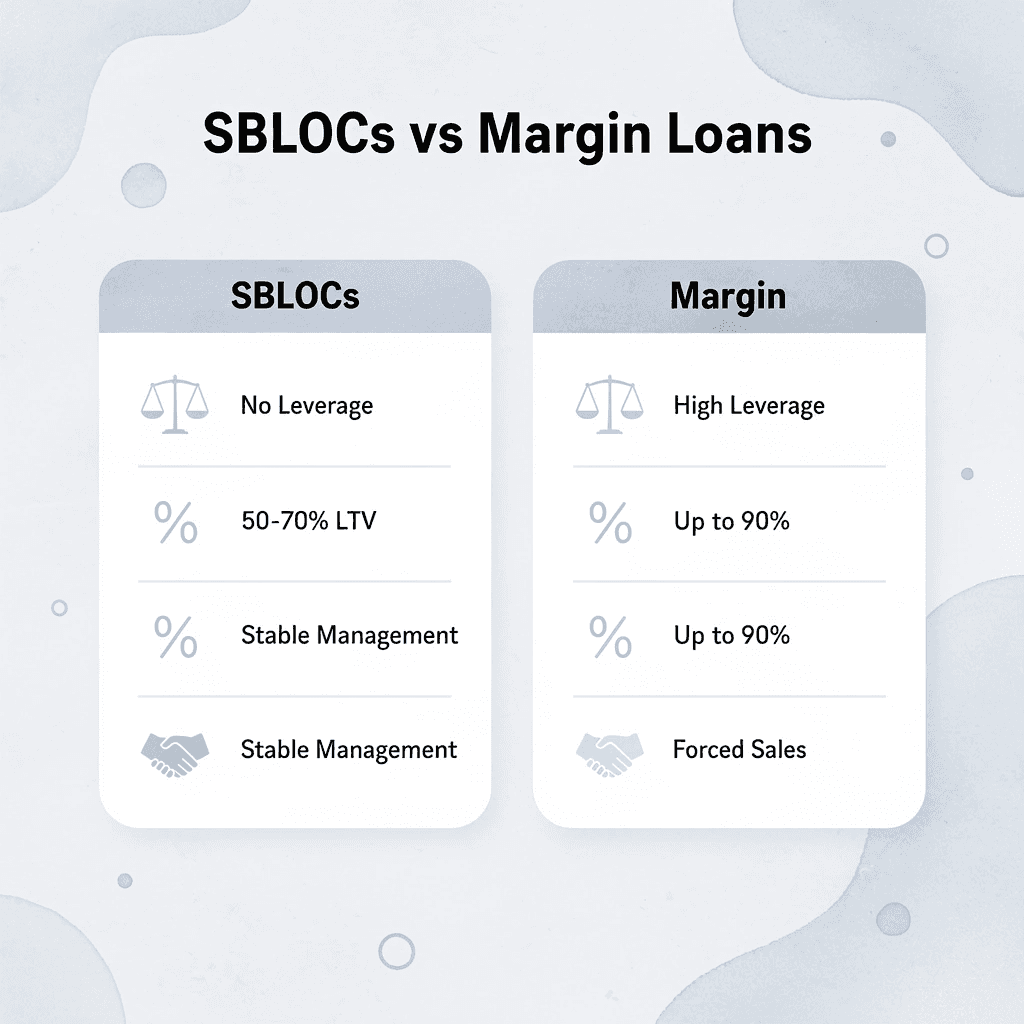

"Securities-based lending typically uses 50-70% loan-to-value ratios compared to margin lending's up to 90% ratios, creating a more conservative borrowing structure." — Financial Industry Analysis

⚠️ Warning: Margin loans can trigger forced liquidations during market volatility, while SBLOCs offer more stable collateral management practices.

How do margin loans amplify your market losses?

Margin loans amplify your market position. Borrow $50,000 against a $100,000 portfolio to buy another $50,000 in stocks, and you hold $150,000 in securities with only $100,000 of your own capital. A 20% market decline drops your portfolio to $120,000, but you still owe $50,000 plus interest. Your equity collapses from $100,000 to $70,000—a 30% loss on a 20% market decline. Brokerages monitor these ratios daily, and leverage amplifies losses exponentially.

Why did margin loan vs securities-based lending perform differently in 2022?

During the 2022 bear market, margin debt across U.S. brokerages plummeted 27% by June from its October 2021 peak, forcing sales that locked in losses for thousands of investors. SBLOC balances remained more stable over the same period because borrowers used the funds for real estate, business expenses, or bridge financing rather than for stock positions. The difference wasn't investor discipline: it was how the product was designed. One structure encourages adding risk; the other forbids it.

How do advance rates create stability buffers?

SBLOC lenders calculate advance rates based on asset volatility, typically offering 50% to 70% for diversified equity portfolios and up to 95% for U.S. Treasuries. These ratios provide substantial equity cushions before maintenance action becomes necessary. Margin accounts operate under Regulation T, which allows a 50% initial borrowing requirement but imposes tighter maintenance requirements that trigger calls more quickly. When your SBLOC lender sets a 60% advance rate on a $500,000 portfolio, you can borrow $300,000 with $200,000 in buffer that absorbs market swings without forcing immediate decisions.

Why do lenders provide more response time with securities-based lending?

The Federal Reserve Board's analysis estimates securities-based loans outstanding at $200 billion to $300 billion, reflecting growing recognition that non-purpose lending reduces systemic leverage risk. Lenders allow weeks to add collateral or reduce balances when portfolios approach maintenance thresholds, rather than automatically selling assets. This differs from brokerage margin systems, which operate on tighter timelines.

Why Forced Liquidations Hit Harder in Margin Accounts

Records from the Securities and Exchange Commission show that forced margin liquidations have cost investors billions of dollars over the past ten years. When this happens, you lose control over which investments to sell, when to sell them, and how to handle the tax results. Brokers sell whatever brings in money fastest, which often means you pay capital gains taxes on appreciated investments while depreciated ones remain in your account. SBLOC agreements typically include larger safety buffers and greater negotiating room, protecting long-term investment plans from short-term market fluctuations.

How do margin mechanics amplify trading risks beyond market exposure?

Most traders overlook how margin mechanics amplify risk beyond the trading focus. The real difference lies in whether borrowed funds add market exposure or provide liquidity. One path doubles down on volatility; the other sidesteps it entirely. Traders seeking capital access without leverage risk often turn to alternatives like a prop firm, where performance-based funding unlocks capital without collateralizing personal portfolios or adding debt-based market exposure.

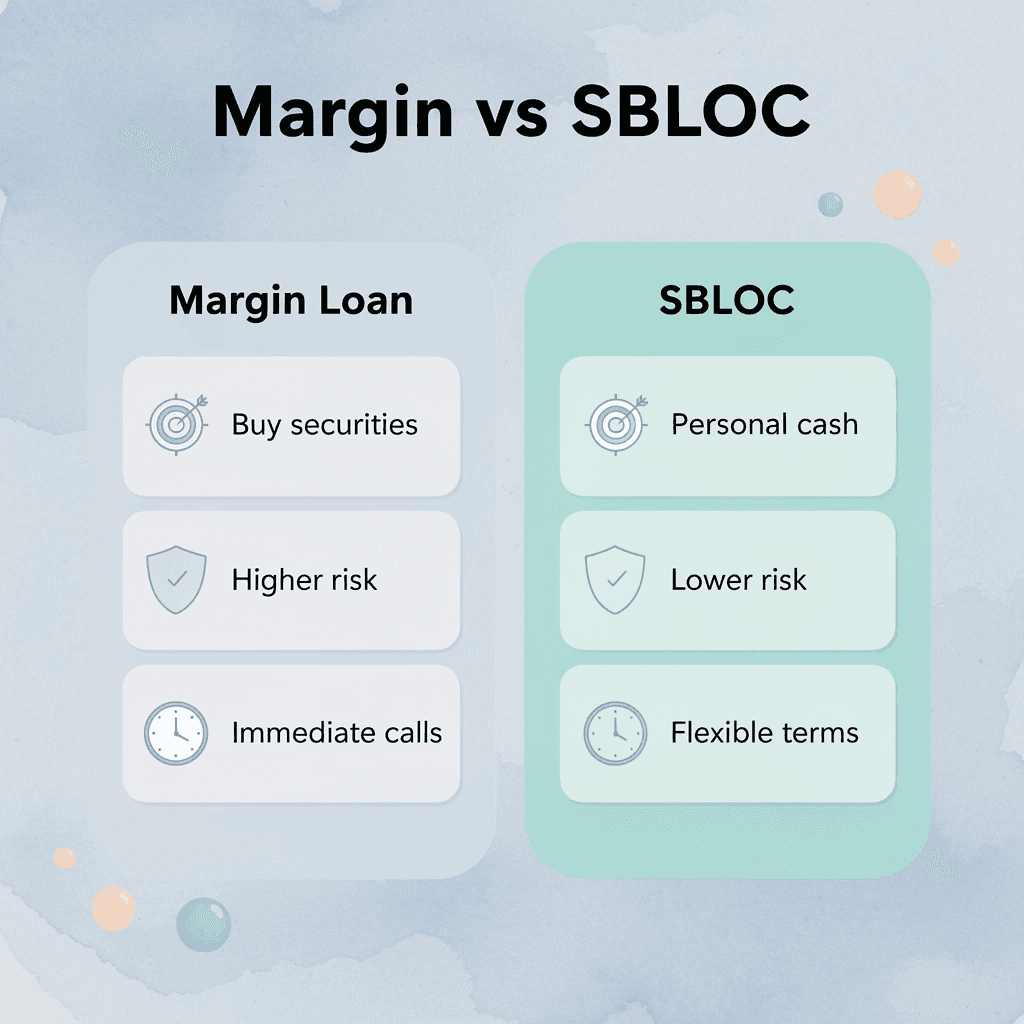

Margin Loan vs Securities-Based Lending: Key Differences

The most important difference comes down to purpose and risk tolerance. A margin loan lets you buy more securities to increase your market position, while an SBLOC provides cash for almost anything except adding investment leverage. This distinction affects how much risk you carry, how lenders respond during market downturns, and how much time you have before forced liquidation. Margin loans integrate with your brokerage to support trading, while SBLOCs remain separate to preserve your original investment strategy.

Margin Loan vs Securities-Based Line of Credit (SBLOC)

- Primary purpose

- Margin loan: Buy more securities

- SBLOC: Cash for personal use

- Risk level

- Margin loan: Higher leverage risk

- SBLOC: Lower overall risk

- Liquidation timeline

- Margin loan: Immediate margin calls possible

- SBLOC: More flexible terms before action is taken

- Investment strategy

- Margin loan: Integrated directly with trading activity

- SBLOC: Separate from portfolio strategy

- Use restrictions

- Margin loan: Funds must be used for securities purchases

- SBLOC: Can be used for most purposes except additional leverage/investing

🎯 Key Point: Margin loans are designed for aggressive portfolio expansion, while SBLOCs provide flexible liquidity without disrupting your core investment strategy.

"Securities-based lending allows investors to access up to 95% of their portfolio value while maintaining their long-term investment positions intact." — Financial Industry Research, 2024

🔑 Takeaway: Choose margin loans when you want to amplify your market exposure, but select SBLOCs when you need cash flexibility without the immediate pressure of margin calls and forced selling.

Purpose and Allowed Uses

SBLOCs work as loans without a specific purpose, so you can get money for almost any legal reason except buying more stocks or paying back existing margin debt. This rule preserves your original portfolio strategy without additional borrowed money. Margin loans, by contrast, are made specifically to buy or hold stocks, which increases your market exposure and potential gains or losses.

Borrowing Limits and Advance Rates

SBLOC lenders offer higher advance rates, commonly 50% to 95% of portfolio value, depending on asset stability and size, with built-in buffers for volatility. Stable portfolios with bonds or blue-chip equities tend to be on the higher end. Margin loans are subject to stricter Regulation T rules that limit initial borrowing to 50% of the purchase price and require maintenance margins of 25% to 40%. This gives SBLOC borrowers more room before action becomes necessary, while margin accounts react faster to price swings.

Interest Rates and Payment Requirements

SBLOC interest accrues only on the money you use. The interest rate is based on SOFR plus an additional amount and changes regularly. You must pay interest monthly, but you can repay the principal whenever you choose. Margin interest works differently: it can accrue without monthly payments and gets added to your balance. SBLOC rates fluctuate daily, while margin rates track broker charges more closely. When markets rise, your margin balance can grow unnoticed, creating larger debts that become apparent only when markets decline.

Risk of Margin Calls and Liquidation

When the market declines, margin calls are triggered immediately through real-time monitoring, forcing sales to meet strict requirements. SBLOCs provide a wider equity cushion and more time to respond before liquidation, better protecting your long-term holdings during temporary downturns. Both options expose you to selling assets at unfavorable prices, but margin accounts react faster. Margin lenders prioritize protecting their capital in fast-moving markets, while SBLOC lenders tolerate short-term volatility because borrowed funds don't compound market exposure.

What alternatives exist to margin loans vs securities-based lending risks?

The Federal Reserve Board's FEDS Notes estimated securities-based loans outstanding at $200 billion as of the end of 2023. Active traders looking for capital without risking their portfolios or facing margin calls often explore alternatives like prop firm funding, where our performance-based model unlocks capital based on skill rather than asset pledges. This changes the access model completely: no collateral at risk, no interest building up, and no forced liquidation when markets become volatile. But understanding these structural differences doesn't tell you which product better protects your long-term wealth when markets get rough.

Related Reading

- Sbloc Vs Margin Loan

- Prop Trading Firms' Profit-Sharing Models

- Position Sizing In Trading

- Can I Borrow Against My Stocks

- How To Borrow Against Stocks

- How To Stay Consistent In Trading

- How Do You Take Profit In Crypto Trading

- Best Prop Firm For Stocks

- Best Crypto Prop Firm

- How To Day Trade Without 25k

- How Do You Profit From Day Trading Stocks

- Position Sizing Day Trading

- Is Issuing Common Stock A Financing Activity

- How To Become A Trader From Home

- Lowest Margin Rates Brokers

Which Protects Your Portfolio, and How to Make the Right Choice

Investors who need cash without selling their assets typically choose between an SBLOC or a margin loan. Both use portfolio value, but they protect wealth differently: one prioritizes cash quickly and long-term wealth preservation, whilst the other increases market exposure and risk. Selecting the wrong option during volatile times can lead to losses that take years to recover from.

🎯 Key Point: The fundamental difference lies in risk management—SBLOCs offer conservative borrowing against your portfolio, while margin loans amplify both your potential gains and potential losses.

"Choosing the wrong credit facility during market volatility can create losses that take years to recover from, making the decision between SBLOC and margin loans critical for wealth preservation."

SBLOC vs Margin Loan

- Primary purpose

- SBLOC: Cash access without selling assets

- Margin loan: Leverage for additional investments

- Risk level

- SBLOC: Lower risk — focused on wealth preservation

- Margin loan: Higher risk — amplified market exposure

- Market volatility impact

- SBLOC: Protected from margin calls (generally more stable structure)

- Margin loan: Vulnerable to margin calls and forced liquidation

- Best for

- SBLOC: Long-term wealth protection and liquidity needs

- Margin loan: Active trading and speculative strategies

⚠️ Warning: During market downturns, margin loans can trigger forced selling at the worst possible times, while SBLOCs typically offer more stable terms and protection from immediate liquidation pressure.

How SBLOCs Protect Your Portfolio

SBLOCs keep your investment strategy separate from your cash needs. You pledge securities as collateral, but the credit line sits outside your brokerage account, preventing you from using borrowed funds to buy more stocks or ETFs. This eliminates the temptation to amplify positions during optimistic market runs. Lenders set advance rates conservatively (typically 50% to 70% for equities and up to 95% for Treasuries), leaving a significant equity cushion before any margin call is triggered.

When markets dip by 15%, your collateral value falls, but you maintain enough of a buffer that lenders rarely force immediate liquidations. Most institutions provide 30 to 90 days' notice before requiring additional collateral or asset sales, giving you time to transfer cash, adjust holdings, or negotiate terms. This breathing room preserves your long-term allocation and prevents panic-driven decisions that lock in losses.

How Margin Loans Expose Your Portfolio

Margin loans let you buy additional securities with borrowed money, turning a $100,000 portfolio into $150,000 in buying power. When values drop by 10%, your equity shrinks faster because losses apply to the larger, more leveraged total. Brokers monitor accounts under Regulation T, which requires at least 25% equity (some firms require 30%-40%).

If equity dips below that threshold, a margin call requires you to deposit cash or sell securities within two to five days. Many brokers reserve the right to liquidate positions immediately without waiting for your response, especially during volatile sessions when prices gap down at the open. You lose control over which assets get sold and at what price, and forced sales often occur at the worst moment, when markets are already under stress.

Key Risk Differences in Market Downturns

Regulation T controls margin accounts with strict rules that allow little room for error. A sudden 20% market drop can wipe out your equity buffer in hours, triggering automatic sell orders that lock in unwanted losses. SBLOCs depend on agreements tied to your overall financial profile and the stability of pledged assets. Lenders allow higher loan-to-value ratios because the funds finance real estate deposits, business expenses, or tax payments rather than risky trades.

According to Cabot Wealth Network, portfolio insurance strategies typically cost 1% to 2% of portfolio value, while SBLOC structures avoid that recurring expense by preserving existing holdings through wider collateral buffers, resulting in fewer surprise liquidations and better diversification during volatility spikes.

Interest Rate and Cost Implications for Protection

SBLOC rates usually tie to the Secured Overnight Financing Rate (SOFR) plus a spread, with many lenders offering fixed-rate options for one to five years. Margin rates link to the broker call rate and change with Federal Reserve policy, often resetting monthly. Margin loans compound costs during downturns: you pay interest on a larger balance while increasing exposure to market swings, and falling values trigger margin calls while interest accrues on the full borrowed amount. SBLOCs avoid this cascading risk—interest applies only to cash drawn, and you don't pay borrowing costs on positions simultaneously losing value.

When should you choose a Margin Loan vs. Securities-Based Lending for your situation?

Choose an SBLOC when you need money for a down payment, business acquisition, tax payment, or personal expense and want maximum protection for your existing investment strategy. The non-purpose restriction prevents you from chasing returns with borrowed money, while conservative advance rates provide a cushion against corrections without forced sales.

Opt for a margin loan only if you plan short-term tactical trades or security purchases where you accept higher volatility for instant access and seamless brokerage integration. Borrowers with concentrated positions in individual stocks face tighter advance rates and faster margin calls under both structures, but SBLOCs provide more headroom because lenders evaluate your entire financial picture rather than just real-time security prices. If your portfolio lacks diversification or you cannot repay within 12 months, neither option adequately protects you.

What alternatives exist for growing capital without collateralizing portfolios

Active traders who want to grow capital without using their portfolios as collateral often explore alternatives such as a prop firm, where our performance-based funding model unlocks capital based on skill rather than on asset pledges. You trade simulated capital, withdraw real profits, and preserve your personal portfolio for long-term growth without leverage exposure. This removes collateral requirements and the risk of forced liquidation while rewarding execution over net worth.

Related Reading

- Best Forex Prop Firm

- Best Margin Rates Brokers

- How Does A Margin Loan Work

- How to Become a Full Time Trader

- How To Trade Forex With A Prop Firm

- Forex Trading Strategies For Consistent Profits

- Options Trading Strategies For Consistent Income

- How To Get Profit In Option Trading

- Day Trading Strategies For Consistent Profits

- Trading Cash Flow

- Recommended Prop Trading Firms With Growth Plans

- Best Trading Strategies For Consistent Profits

How Goat Funded Trader Acts as a Safer Alternative to Margin Loan

When you borrow against your portfolio, a bad week can trigger forced sales, interest charges accumulate regardless of performance, and your collateral sits exposed to liquidation. Goat Funded Trader reverses that equation: you trade simulated capital provided by the firm, keep profits through splits up to 100%, and your personal assets remain untouched.

🔑 Key Takeaway: Traditional margin trading puts your entire portfolio at risk, while prop trading with firms like Goat Funded Trader creates a protective barrier between your personal wealth and trading activities.

"Prop trading eliminates the single greatest risk in margin trading: personal asset exposure during market volatility." — Risk Management Analysis, 2024

⚠️ Warning: Margin calls can force you to sell positions at the worst possible time, turning temporary drawdowns into permanent losses that could take years to recover from.

Zero Personal Collateral Exposure

Margin loans and SBLOCs require pledging securities you already own, exposing long-term holdings to market swings and volatility. Goat Funded Trader eliminates this entirely. You pass an evaluation using simulated capital, then trade firm-funded accounts up to $2M without tying up a single share from your personal portfolio. Your investments stay where they belong: growing tax-deferred in retirement accounts or compounding in taxable portfolios, completely isolated from trading activity.

No Interest Costs or Debt Accumulation

Traditional borrowing charges interest on every dollar you borrow: a $100,000 margin loan at 8% costs $8,000 annually, regardless of profit. Goat Funded Trader charges only a one-time evaluation fee (100% refundable after your first payout). You pay no carrying costs, no compounding interest, no variable rate adjustments. Every dollar of profit stays yours to withdraw, not split with a lender.

Defined Risk Without Margin Calls

Margin accounts force you to sell investments when equity drops below certain levels, often at the worst possible moment when prices are low. SBLOCs force asset sales if collateral values fall too far. Goat Funded Trader enforces clear risk rules: 3% maximum daily loss, 6% overall maximum loss. These limits apply to simulated capital, not your personal wealth. If you hit a drawdown, the firm absorbs it. You never face a margin call that demands more collateral or forces you to sell investments you planned to hold for decades.

Unlimited Strategy Flexibility and Scaling

Borrowed funds come with restrictions: margin loans prohibit certain securities, SBLOCs ban purchasing investments entirely, and both limit trading aggressiveness. Goat Funded Trader allows news trading, weekend holding, and unlimited trading periods across FX pairs, stocks, ETFs, and crypto pairs on platforms like MT5.

How does scaling work without traditional collateral requirements?

As your performance improves, you move to larger accounts based on trade execution rather than personal assets. A trader with $50,000 can access the same $2 million in simulated capital as someone with $5 million, because the firm rewards skill rather than collateral.

What are the hidden psychological costs of a margin loan vs securities-based lending?

The real cost of borrowing is the mental weight of knowing one bad stretch could wipe out years of disciplined investing, and that pressure changes how you trade.

Get 25-30% off Today - Sign up to Get Access to Up to $800K Today

SBLOCs and margin loans expose your stocks, bonds, and investments to margin calls, forced liquidations, rising interest charges, and market volatility. These financing methods create unnecessary exposure that can devastate your carefully built portfolio.

Goat Funded Trader gives skilled traders up to two million dollars in simulated capital after evaluation. You trade on MT5 with real market conditions, keep up to 100% of profits, and have zero liability for losses. Your personal portfolio remains completely untouched: no pledges, no debt, no interest payments.

"Over 20 million dollars have already been paid out to traders worldwide, proving the effectiveness of funded trading programs." — Goat Funded Trader, 2024

This solves every issue raised in this article. Your investments stay safe with no collateral required. You eliminate interest and debt by paying only a one-time, fully refundable evaluation fee. Strict risk rules protect you from margin calls on simulated capital. You get complete trading flexibility with news trading, weekend holding, and unlimited periods, plus the ability to grow based on performance. Fast payouts arrive within 24 hours, or the firm adds one thousand dollars as a guarantee.

🔑 Key Takeaway: Funded trading eliminates the fundamental risks of traditional margin while providing greater capital access and profit potential.

If you continue relying on SBLOCs or margin loans, your portfolio remains vulnerable to forced sales, higher taxes, and disrupted growth while carrying debt. The opportunity cost of not switching grows exponentially over time.

⚠️ Warning: Every day you delay switching from traditional margin to funded trading is another day your personal wealth remains at unnecessary risk.

Join over 250,000 traders who protect their wealth while trading larger sizes and keeping more profits. This community proves that funded trading is the superior alternative to risking personal assets.

Start today with 50% off your first account using code FIRSTGFT. No credit card required for evaluation, instant dashboard access after signing up, and you can begin trading after passing. The evaluation process is designed to be fair and achievable for skilled traders.

Ready to trade without risking what you've already built? Visit Goat Funded Trader and get funded now. Your financial future depends on smarter capital allocation decisions today.

Be Great and get the App