Why Is Schwab Margin Rate So High For Traders in 2026?

Why Is Schwab Margin Rate So High? Goat Funded Trader reveals the hidden fees and better alternatives for smart traders in 2026.

.png)

Charles Schwab's margin rates often catch traders off guard, especially those expecting competitive pricing from such a major brokerage. Many discover that interest charges steadily erode their profits, prompting questions about what drives these costs and whether better alternatives exist. Understanding Schwab's margin structure helps traders make informed decisions about how to leverage their positions.

Traders seeking substantial buying power without interest charges have another option worth considering. Prop trading firms provide access to significant capital without the burden of margin costs or personal financial risk. Goat Funded Trader offers accounts that let traders use firm capital while keeping a generous share of profits, creating a path to growth without the hidden costs of traditional margin accounts.

Summary

- Margin trading amplifies both gains and losses while adding daily interest charges that compound over time. A stock that rises 15% over three months might net you only 8% after interest and transaction costs, especially if you borrowed at higher rates during volatile periods. The mechanics seem straightforward until you face a margin call at the worst possible moment, when brokers liquidate positions at current market prices and lock in your losses.

- Schwab enforces a 30% maintenance margin for most long equity positions, meaning your equity must stay at or above 30% of total market value. House requirements climb higher for concentrated bets or volatile names, so your 30% floor becomes 40% or 50% without warning when Schwab's risk model flags your holdings. Traders often discover this reality too late, facing forced liquidations during temporary downturns that they might have recovered from with more patience.

- Smaller balances face steep borrowing costs at Schwab, with rates reaching 11.825% for balances under $25,000 compared to 10.375% for balances between $50,000 and $99,999.99. The tiered structure reflects Schwab's funding costs and operational model, not an arbitrary markup. Brokers source margin capital from banks through the call money market, a short-term lending system that moves with Fed policy, creating a rate floor no retail lender can undercut without subsidizing loans.

- Retail investor accounts show troubling performance patterns with leveraged trading. 70% of retail investor accounts lose money when trading CFDs with providers, according to Capital.com, a pattern that extends to margin trading, where leverage can turn small mistakes into account-destroying events. The mental stress of managing personal margin puts you in panic mode when positions move against you, leading to revenge trading, oversized bets, and the discovery of your limits through financial ruin rather than through controlled learning.

- Every dollar borrowed on margin carries interest that compounds daily, plus the risk of liquidation when equity falls below maintenance thresholds. Margin works for short-term trades with clear exits, not long-term holds, because the interest expense erodes returns over time. Traders who chase the lowest rate often discover limits during market stress, when discount brokers tighten requirements or restrict volatile positions faster than established firms.

- Goat Funded Trader provides access to simulated capital up to $2 million after passing structured challenges, with traders keeping up to 100% of profits in some plans while the firm absorbs losses and eliminates margin interest entirely.

What is Margin Trading, and How Does It Work?

Margin trading lets you borrow money from your broker to buy securities beyond your cash balance. You put up a portion as collateral while the broker lends the rest, letting you control a larger position than your own funds allow. This leverage amplifies both gains and losses and incurs interest charges on borrowed amounts.

🎯 Key Point: Margin trading is essentially using borrowed capital to increase your buying power - but remember that leverage works both ways, magnifying your potential profits and your potential losses equally.

"Margin trading allows investors to purchase more securities than they could with cash alone, but it also significantly increases risk exposure." — Financial Industry Regulatory Authority

💡 Example: If you have $5,000 in cash and your broker offers 2:1 leverage, you could control up to $10,000 worth of securities. However, you'll pay interest on the borrowed $5,000 daily until you close the position.

Key Margin Trading Components

- Initial Margin

- Description: Minimum cash you must deposit to open a margin position

- Your responsibility: Pay the required amount upfront

- Borrowed Funds

- Description: Money lent to you by the broker

- Your responsibility: Pay daily interest on borrowed capital

- Maintenance Margin

- Description: Minimum account value you must maintain after opening trades

- Your responsibility: Monitor account levels constantly

- Margin Call

- Description: Broker demand for additional funds or collateral

- Your responsibility: Respond immediately to avoid forced liquidation

How do you apply for margin account approval?

You apply for margin approval with your brokerage, which evaluates your financial situation, trading experience, and risk tolerance. Once approved, you sign a margin agreement outlining borrowing terms, interest rates, and the broker's rights to liquidate your holdings if account equity drops below a certain threshold. Unlike a cash account, securities become collateral for the loan, and your broker can sell them without permission if market conditions turn against you.

Why do many traders misunderstand margin mechanics?

According to a FINRA Foundation survey, only 15% of margin traders correctly answered a basic question about how margin works, compared to 31% of non-margin traders. This reveals a significant knowledge gap regarding margin mechanics and associated risks.

Initial Margin and Leverage Mechanics

According to Charles Schwab, the 50% initial margin requirement means you must deposit half the trade value upfront and borrow the rest. Buying $20,000 worth of stock requires $10,000 of your capital and $10,000 borrowed, creating 2:1 leverage that magnifies every percentage move. A 10% gain delivers 20% return on your deposited capital (minus interest), while a 10% loss wipes out 20% of your equity before interest. The debt remains regardless of the asset's performance.

Maintenance Margin and Forced Liquidation

Your account equity—the market value of your holdings minus the loan balance—must stay above the maintenance margin threshold, typically 25% to 30% of total position value. When prices fall below this level, your broker issues a margin call requiring you to add cash or securities immediately. If you cannot meet the call by the deadline, your broker sells your positions at current market prices, locking in losses and potentially leaving you with outstanding debt if the sale proceeds fall short.

Interest Costs and Holding Period Impact

Brokers charge daily interest on margin loans, with rates that vary with the loan amount and market conditions. Unlike mortgages or car loans with set payments, margin debt has no repayment schedule: interest compounds daily and compounds over weeks or months, eroding profits even on winning trades.

A stock that rises 15% over three months might yield only 8% profit after interest and transaction costs, particularly when rates are higher during unstable market periods. Shorter holding periods reduce these costs but require precise timing and constant monitoring.

What happens when margin calls occur at the worst moment?

The mechanics seem straightforward until you face a margin call at the worst possible moment. But how much leverage can you access, and what limits do brokers place on your borrowing capacity?

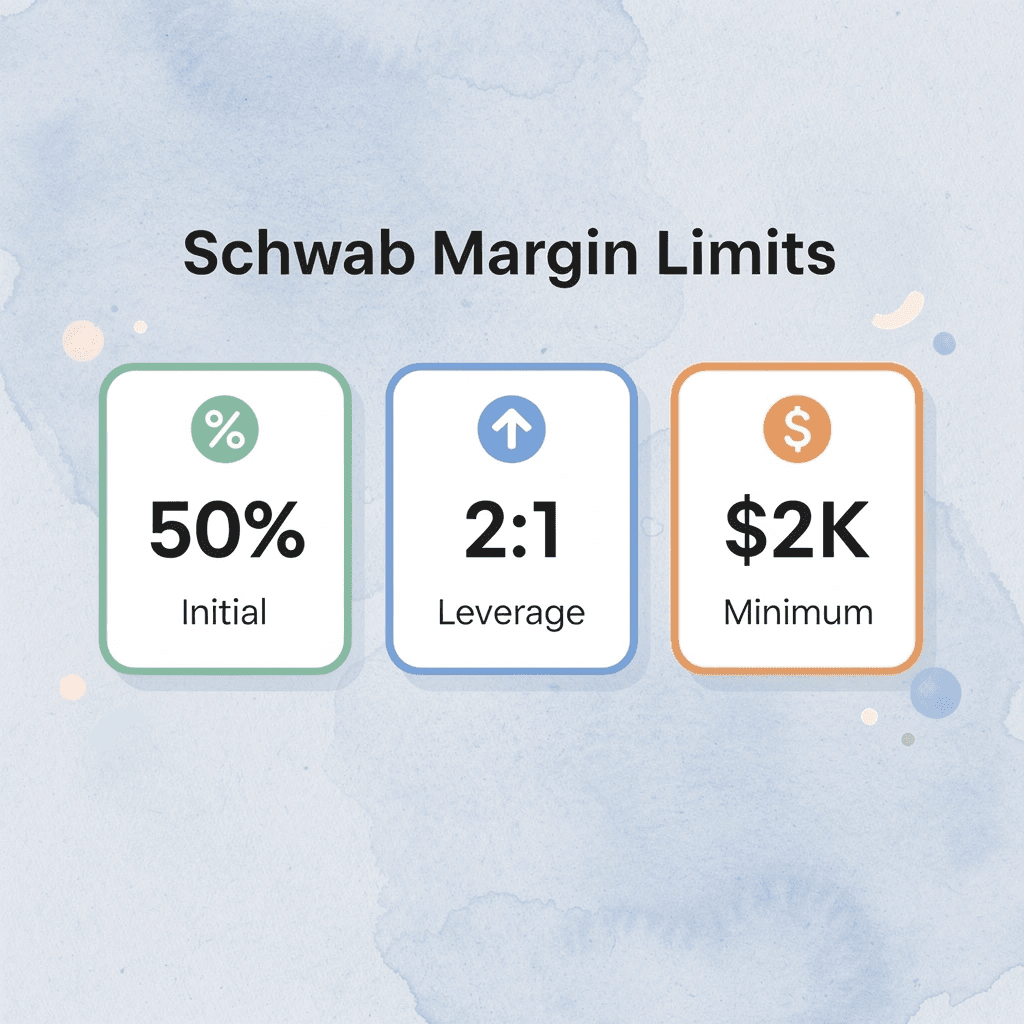

How Much Margin Does Schwab Offer?

Schwab lets approved clients borrow up to 50% of the purchase price on eligible stocks, providing 2:1 leverage with a $2,000 minimum account equity. Maintenance margins and interest rates vary by balance size and portfolio risk: smaller balances incur higher borrowing costs, while concentrated or volatile positions require higher house requirements, reducing effective leverage.

🔑 Key Takeaway: Schwab's margin requirements are more restrictive than the standard 25% maintenance margin for high-risk positions, meaning your actual borrowing power may be considerably less than the advertised 50% initial margin.

"Schwab provides up to 50% margin on eligible securities with 2:1 leverage potential, but actual borrowing capacity varies based on portfolio composition and account balance." — Schwab Margin Requirements, 2024

Margin Account Tiers Overview

- $2,000 – $25,000

- Typical interest rate range: Higher rates

- Effective leverage: 1.5:1 – 2:1

- $25,000 – $100,000

- Typical interest rate range: Moderate rates

- Effective leverage: 1.8:1 – 2:1

- $100,000+

- Typical interest rate range: Lower rates

- Effective leverage: Up to 2:1

💡 Important Note: Concentrated positions in volatile stocks often trigger house requirements above the standard 50% initial margin, effectively reducing your maximum leverage to as low as 1.3:1 or 1.5:1, depending on the specific securities in your portfolio.

Starting with the $2,000 Floor

Your margin journey at Schwab begins when your account reaches $2,000 in cash or marginable securities. Below that amount, you trade only in cash. Approval requires a brief application reviewing your trading background and financial situation. Once cleared, you can borrow against half your stock purchases. However, $2,000 provides minimal exposure even with leverage, and any quick loss can drop you below the threshold.

When Maintenance Margins Bite Harder

Schwab enforces a 30% maintenance margin for most long equity positions, meaning your equity must stay at or above 30% of total market value. A $20,000 position dropping 15% shrinks your $10,000 equity to $7,000, pushing your equity ratio to 41%—still safe but closer to the edge. Another 10% drop triggers a margin call demanding immediate cash or securities. House requirements climb higher for concentrated bets or volatile names, so your 30% floor becomes 40% or 50% when Schwab's risk model flags your holdings.

How do Schwab's margin rates scale with your balance?

Schwab's base margin rate sits at 10.00%, but your actual rate depends on your borrowing amount. Borrowing $0–$24,999.99 at 11.825% (base plus 1.825%) erodes profits quickly. At $50,000–$99,999.99, the rate drops to 10.375% (base plus 0.375%), but daily compounding still adds high cost. Even the lowest rates can turn a promising trade into a breakeven when held for weeks.

Why is the Schwab margin rate so high compared to the prop firm alternatives?

Most traders borrow money to increase returns without considering interest costs or the speed of margin calls. Traditional brokers like Schwab structure margin accounts to protect themselves first: you absorb losses, pay compounding interest, and face forced liquidation during market volatility. Prop firms like Goat Funded Trader eliminate these constraints by providing simulated capital after you pass their test, removing personal borrowing costs and margin calls while you keep up to 100% of profits. You trade with more capital and zero interest expense, allowing you to focus on strategy rather than maintenance thresholds.

What is portfolio margin for experienced accounts?

Qualified clients with at least $125,000 in equity and options approval can access portfolio margin, which calculates requirements based on overall portfolio risk rather than fixed percentages. This approach can push leverage to 6.6 to 1 on diversified positions, far beyond standard margin limits. Portfolio margin demands deeper experience since Schwab's system recalculates risk dynamically: your leverage shrinks when markets turn choppy, and you need backup liquidity to avoid forced exits during stress.

Why is the Schwab margin rate so high, even with portfolio margin?

Even with better leverage ratios, you still pay interest on every dollar borrowed and face liquidation risk when equity drops below certain levels.

Related Reading

- What Is A Prop Firm Forex

- Financing Stock Options

- How Is Margin Interest Calculated

- Can You Make A Living Day Trading

- How Much Margin Does Fidelity Offer

- Why Are Fidelity Margin Rates So High

- No Consistency Rule Prop Firm

- How Does Margin Work On Robinhood

- Options Trading Cash Flow Strategies Explained

- How To Compare Brokers By Margin Interest Rates

- How Does Margin Interest Work

- How Much Do Day Traders Make Per Month

- How Does Margin Work at Interactive Brokers

Why Is Schwab Margin Rate So High For Traders?

Schwab's margin rates show the costs of borrowing and how the company is strategically organized. When you borrow on margin, Schwab borrows at the broker call rate (which follows federal policy rates), then adds extra charges for credit risk, infrastructure, and regulatory capital. Smaller accounts pay around 13.825% for balances under $25,000, while larger borrowers get the base lending rate minus 1.00% for balances of $1,000,000 or more. The tiered structure gives larger borrowers better deals, with base costs tied to wholesale funding markets.

🎯 Key Point: Schwab's margin rates aren't just about borrowing costs—they reflect a strategic business model that rewards larger accounts while managing credit risk across different customer segments.

"Smaller accounts pay around 13.825% for balances under $25,000, while larger borrowers get rates as low as base lending rate minus 1.00% for balances of $1,000,000 or more." — Schwab Margin Rates, 2024

Margin Rate Tiers by Account Balance

- Under $25,000

- Margin rate: 13.825%

- Rate structure: Highest tier

- $25,000 – $49,999

- Margin rate: Base rate + premium

- Rate structure: Mid-tier pricing

- $1,000,000+

- Margin rate: Base rate − 1.00%

- Rate structure: Lowest tier (preferred pricing)

🔑 Takeaway: The dramatic difference between small account rates (13.825%) and large account rates (base minus 1.00%) shows how Schwab prioritizes high-net-worth clients while using margin pricing as a profit center for smaller traders.

Why Broker Funding Costs Drive the Rate Floor

Brokers obtain margin capital from banks through the call money market, a short-term lending system tied to Fed policy. When the federal funds rate is at 4.5%, the broker call rate hovers near that level, creating a floor below which retail lenders cannot operate profitably. Schwab adds a spread to cover default risk, margin call administration, and regulatory capital buffers for leveraged accounts. Brokers cannot offer 3% margin rates without accepting losses or restricting access during volatility.

How Business Model Differences Explain Rate Gaps

Some platforms advertise rates below 5%, but those offers come with tradeoffs. Interactive Brokers and Public.com operate as low-margin, high-volume lenders with stripped-down service models and stricter risk controls. Schwab provides broader account features, research tools, and relationship pricing that add operational costs. Traders chasing the lowest rate often hit limits during market stress, when discount brokers tighten requirements or restrict volatile positions more quickly than established firms.

What Traders Miss About Rate Negotiation

Published rates are starting points, not fixed prices. Clients with six-figure balances or strong account histories can negotiate lower rates through relationship pricing or pledged-asset lines. Schwab adjusts terms for borrowers who show volume, stability, or use multiple products. This flexibility rarely appears in marketing materials, but it changes the real cost for serious traders. The key is asking: firms want to keep profitable clients, and margin interest is negotiable when the relationship justifies it.

Why does margin borrowing cost more than capital access

Every dollar you borrow on margin costs you daily interest and exposes you to losses if your account value falls below certain levels. You pay for leverage, risk management, regulatory compliance, and the broker's capital allocation. Margin works best for short-term trades with a clear exit plan, not for long-term holdings. Interest charges erode profits over time, and forced sales during market drops lock in losses you might have recovered by waiting. Borrowing to make larger bets only makes sense when you expect returns exceeding interest costs and can tolerate price swings without panic-driven decisions.

How do funded trading accounts avoid margin interest entirely?

A prop firm like Goat Funded Trader sidesteps margin interest by funding traders with simulated capital after they pass evaluation accounts. Instead of paying 11% or 13% to borrow, traders keep up to 100% of profits without risking personal funds or incurring debt. The model shifts the equation from leverage cost to skill validation, giving traders more capital and less financial stress than traditional margin.

How do you use margin without career-ending mistakes?

But even if you secure better rates or explore funded accounts, one question remains: how do you use margin without turning a manageable loss into a career-ending mistake?

How to Trade With Margin Responsibly on Schwab

Using margin responsibly on Schwab starts with knowing your real limits, not just what the broker allows. Ask for margin approval through your account settings and ensure you have at least $2,000 in equity before borrowing. Charles Schwab requires a 50% initial margin, meaning your $10,000 in cash can control $20,000 in positions. Review Schwab's concentration model, which increases requirements for volatile stocks or those representing a large portion of your portfolio. This prevents your buying power from dropping when you need it most.

🎯 Key Point: Always maintain a cash cushion beyond Schwab's minimum requirements. Market volatility can trigger margin calls faster than you expect, especially with concentrated positions.

"Margin trading amplifies both gains and losses - a 2:1 leverage ratio can double your returns but also double your risk exposure." — Securities and Exchange Commission, 2023

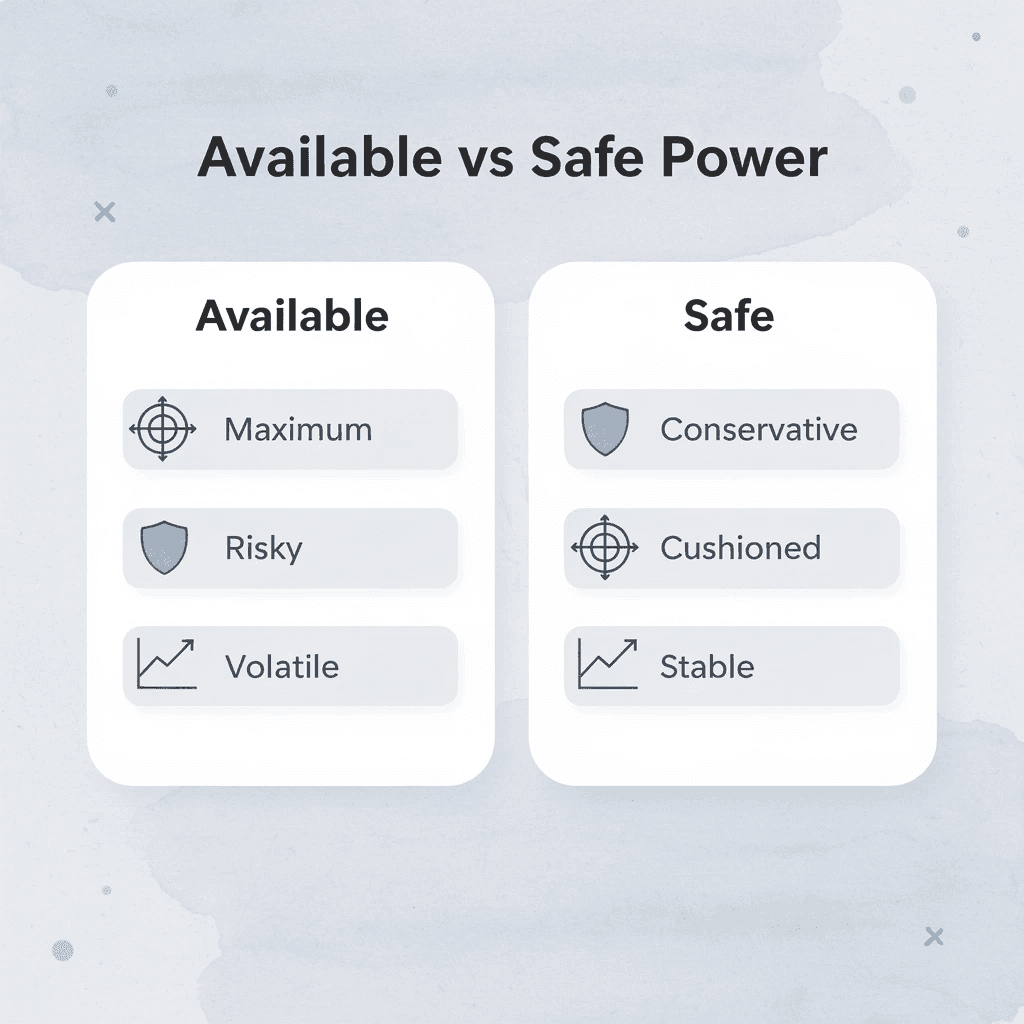

⚠️ Warning: Don't confuse available buying power with safe buying power. Schwab's concentration model can reduce your margin availability by 25-50% for volatile stocks without warning.

Margin Requirements & Buying Power

- 50% (Standard)

- Your cash: $10,000

- Total buying power: $20,000

- Risk level: Moderate

- 75% (Volatile stock)

- Your cash: $10,000

- Total buying power: $13,333

- Risk level: High

- 100% (Restricted)

- Your cash: $10,000

- Total buying power: $10,000

- Risk level: Low

Set Personal Risk Rules Before Trading

Create your own safety cushion higher than Schwab's 30% maintenance requirement. A personal floor of 40% or 50% provides extra protection when markets drop, preventing forced sales during temporary downturns. Decide on position sizes that never exceed a fixed percentage of your total account value, write those limits down, and stick to them before making any leveraged trade. This structure transforms margin from an emotional trap into a controlled advantage.

Diversify and Monitor Daily

Spread margin borrowing across multiple uncorrelated securities so that a single-sector drop doesn't trigger a margin call. Borrow well below your maximum available buying power, leaving reserve capacity for adjustments or unexpected volatility. Charles Schwab requires maintaining 50% of your account equity in marginable securities; diversified collateral and conservative usage keep you stable when individual holdings move against you. Check your account equity and margin status daily, especially during volatile periods, and place stop-loss orders based on the portfolio's margin impact, not just price.

Manage Interest Costs Actively

Pay down debt balances quickly since interest compounds daily. Track your tiered rate based on loan size and move larger amounts to lower-rate brackets when possible: a $30,000 balance at 12.575% costs $3,772 annually, while a $100,000 balance at 11.825% costs less per dollar borrowed. Shorter holding periods and on-time repayments reduce interest costs, transforming margin from a permanent loan into a tactical tool you deploy only when the trade setup justifies the expense.

Prepare Contingency Plans for Margin Calls

Keep extra cash or stocks available to borrow against so you can meet margin calls immediately. Create a written plan identifying which positions you will sell first if your account value approaches your personal limit. Fast response and advanced planning can transform potential disasters into manageable adjustments.

When your own money limits margin at Schwab, traders can turn to prop firm funding to access larger trading opportunities without risking personal accounts beyond evaluation fees. Our Goat Funded Trader program provides practice capital up to $2 million after passing structured challenges, with traders retaining up to 100% of profits in some plans while the firm absorbs losses.

Related Reading

- How To Become A Trader From Home

- How To Day Trade Without 25k

- Position Sizing Day Trading

- Sbloc Vs Margin Loan

- How To Borrow Against Stocks

- Best Prop Firm For Stocks

- Can I Borrow Against My Stocks

- How Do You Profit From Day Trading Stocks

- Best Crypto Prop Firm

- Position Sizing In Trading

- How Do You Take Profit In Crypto Trading

- How To Stay Consistent In Trading

- Is Issuing Common Stock A Financing Activity

- Prop Trading Firms' Profit-Sharing Models

- Lowest Margin Rates Brokers

How Goat Funded Trader Helps Traders Use Margin More Effectively

Goat Funded Trader replaces personal margin borrowing with a funded capital model that eliminates interest costs and personal loss exposure. You trade simulated capital after passing evaluation challenges, keeping up to 100% of profits while our firm absorbs drawdowns. This structure provides professional-scale leverage without the debt trap or liquidation risk that destroys retail margin accounts.

🎯 Key Point: With funded trading, you get institutional-level leverage without risking your own capital or paying margin interest fees that can compound into thousands of dollars annually.

"Funded trading eliminates the personal financial risk while providing up to 100% profit sharing — giving traders professional-scale capital without the traditional margin debt burden." — Goat Funded Trader Model

🔑 Takeaway: This capital structure transforms margin from a costly personal liability into a risk-free opportunity to trade with significant leverage while keeping all the upside potential.

Eliminating Interest Drag That Kills Returns

Schwab margin charges compound daily, turning marginal winners into break-even trades and slowly draining account equity even when your directional calls prove correct. Every position held on borrowed funds accrues interest, reducing net profit before withdrawal. Goat Funded Trader removes this burden completely—you trade our capital with zero interest charges. Your performance determines your payout, not your ability to service debt, so every profitable trade flows directly to your bottom line without erosion.

Providing Structure That Prevents Emotional Blowups

The mental stress of managing personal margin puts you in panic mode when positions move against you, leading to revenge trading, oversized bets, and account-destroying mistakes. Traditional margin offers no guardrails until the margin call arrives, forcing liquidation at the worst possible moment. Goat Funded Trader builds discipline into the system with fixed 4% daily loss and 6% maximum drawdown limits that stop you before catastrophic damage occurs. These rules instill consistency and risk management that separate professionals from gamblers, creating a safer environment where you learn to trade size responsibly rather than discover your limits through financial ruin.

Scaling Capital Without Scaling Personal Risk

When you lack substantial capital, trading larger amounts becomes difficult, even when you identify good opportunities. According to Goat Funded Trader, our scaling program provides traders access to up to $2,000,000 in capital. Your account size grows based on consistent trading performance, not existing funds.

How do funded accounts compare to high-margin rates like Schwab's?

You start with smaller, funded accounts, prove your edge within their rules, and gradually unlock larger capital allocations without additional personal investment or liability. Most traders using personal margin discover too late that bigger positions magnify mistakes.

Funded trading through platforms like Goat Funded Trader pairs leverage of up to 10:1 with mandatory loss limits and performance tracking, giving you access to capital for larger positions while the firm enforces discipline. After completing the evaluation process and demonstrating consistency within defined risk parameters, you trade the firm's capital without margin calls or personal savings at risk.

Delivering Fast Payouts Without Liquidation Fear

Goat Funded Trader offers your first payout on demand within 24 hours or adds $1,000 to your account, with a full payout guarantee in two business days through bank transfer, crypto, or local methods. You withdraw real cash from consistent performance while the firm manages capital and absorbs drawdowns, eliminating the stress of watching your personal margin equity fluctuate and risking liquidation before your trading idea plays out. Accessing this structure and scaling to meaningful capital requires understanding our evaluation and funding process.

Get 25-30% off Today - Sign up to Get Access to Up to $800K Today

Margin trading at Schwab adds interest charges daily. One bad week can force you to sell positions and lose money that took months of careful work to build. These costs remain constant regardless of your skill level.

Goat Funded Trader solves this problem by giving you access to up to $2 million in practice money with zero of your own money at risk and no interest charges. Pass simple evaluations, then trade under clear 4% daily and 6% maximum loss rules while keeping up to 100% of your profits. The firm covers losses and pays you within 24 hours (or grants an extra $1,000), letting you grow your accounts without risking your own money. Use code FIRSTGFT for 50% off your first account, and receive your money back if you don't pass.

Related Reading

- How To Become A Full-Time Trader

- Trading Cash Flow

- Recommended Prop Trading Firms With Growth Plans

- How To Get Profit In Option Trading

- Best Forex Prop Firm

- Forex Trading Strategies For Consistent Profits

- Margin Loan vs. Securities-Based Lending

- How To Trade Forex With A Prop Firm

- Best Margin Rates Brokers

- Options Trading Strategies For Consistent Income

- Best Trading Strategies For Consistent Profits

- Day Trading Strategies For Consistent Profits

- How Does A Margin Loan Work

Be Great and get the App

.webp)