How Does a Margin Loan Work? All You Need to Know in 2026

How does a margin loan work? Goat Funded Trader explains borrowing against securities, interest rates, risks, and requirements in 2026.

.png)

Professional traders often use margin loans to amplify their buying power and capture larger opportunities in Capital Growth Trading. A margin loan allows traders to borrow money from their broker using existing investments as collateral, enabling them to purchase more securities than their cash balances would normally permit. This borrowed capital can accelerate returns when markets move favorably, but it also magnifies losses when trades move against positions. Understanding interest rates, maintenance requirements, and margin calls becomes essential before utilizing this powerful financial tool.

Learning margin trading concepts without risking personal capital makes the educational process significantly less costly. Practicing position sizing, interest calculations, and risk management with funded accounts helps traders develop disciplined habits under real market conditions. Rather than risking personal savings while mastering these strategies, traders can focus on skill development and demonstrate their abilities with substantial trading capital provided by a prop firm.

Summary

- Margin loans allow traders to borrow up to 50% of their portfolio value from brokers, instantly doubling purchasing power without selling existing positions. This leverage transforms modest gains into substantial profits when trades succeed, but it also magnifies losses and creates daily interest charges that compound regardless of market performance. The Federal Reserve sets the initial 50% margin requirement, while FINRA enforces a 25% minimum maintenance threshold that triggers forced liquidations when breached.

- Forced liquidations from margin calls reduce daily returns by more than 26% compared to traders who avoid calls, according to a 2018 UCLA Anderson study on Chinese futures traders. Brokers sell positions automatically during market downturns to recover loans, often dumping your best long-term holdings at depressed prices without warning or permission. You remain personally liable for any shortfall between sale proceeds and outstanding debt, turning market volatility into credit damage that persists for years.

- Most traders who use margin fundamentally misunderstand how it works. A 2025 FINRA Foundation study found that 75% of investors who actively use margin incorrectly answered basic questions about margin mechanics, revealing a dangerous knowledge gap. This widespread confusion explains why so many traders get caught off guard by maintenance requirements, interest accrual, and the speed at which equity cushions evaporate during normal market swings.

- Margin interest rates can reach 12% annually on borrowed funds, creating a hidden drag that turns winning months into breakeven outcomes. These costs accrue daily and compound monthly regardless of whether your portfolio gains or loses value, functioning as a silent expense that erodes returns over time. Traders must generate returns that exceed both market movements and ongoing borrowing costs to achieve actual profitability, a hurdle that becomes particularly punishing during flat or declining markets.

- Conservative margin management requires maintaining equity cushions of 40% to 50% above broker minimums, using only 25% to 50% of available borrowing capacity, and monitoring account balances daily. This disciplined approach protects against forced sales during normal volatility, but it demands constant vigilance and restricts the aggressive leverage that attracts traders to margin in the first place. The gap between maximum theoretical buying power and prudent actual usage reveals why margin works better as a short-term liquidity tool than a long-term wealth-building strategy.

- Goat Funded Trader addresses this by providing traders with up to $2M in simulated capital, where you keep up to 100% of profits without personal financial risk, margin calls, interest charges, or liability for losses.

What Is a Margin Loan, and How Does It Work?

A margin loan is borrowed money from your brokerage, secured by the securities in your account. According to the Office of the Comptroller of the Currency, it works as a loan from a broker to a client through a margin account. Unlike traditional bank loans, margin loans require no application, approval wait, or term negotiation. You gain instant access to capital based on the value of your holdings, allowing you to buy more securities or withdraw cash without selling positions.

🎯 Key Point: Margin loans provide immediate liquidity without requiring you to liquidate your investment positions, making them ideal for short-term capital needs or investment opportunities.

"Margin loans offer instant access to capital based on your holdings' value, with no application process or approval delays." — Office of the Comptroller of the Currency

💡 Example: If you own $100,000 in stocks, you could typically borrow up to $50,000 instantly through a margin loan, using your securities as collateral while keeping your positions intact.

How does a margin loan work in practice?

Here's how it works: open a margin account, deposit stocks or cash that qualify as collateral, and borrow money against that value. If you hold $10,000 in qualifying stocks, you might borrow up to $5,000. Your broker charges daily interest on borrowed funds; rates typically decrease as you borrow more. You need not make monthly principal payments. The loan remains active until you repay it by depositing cash or selling your positions.

What are the initial margin requirements for new positions?

Brokers enforce an initial margin requirement of 50% under Federal Reserve rules, meaning you must fund at least half of any new position with your own money. According to FINRA, the 25% minimum maintenance margin requirement sets the floor for required equity. If your equity drops below that level due to market declines, you receive a margin call demanding immediate action: deposit more funds, add securities, or sell assets to restore the required balance.

What happens when you fail to meet a margin call?

Failure to meet a margin call triggers forced liquidation by the broker, often when prices are falling. You lock in losses, your positions disappear, and you remain responsible for any remaining debt. The broker needs no permission in extreme situations.

How do daily interest charges accumulate over time?

Interest accrues daily and is added to your account monthly. The amount is calculated using rate schedules that vary by broker and loan size. These costs are lower than credit card rates, but they still reduce your returns if your investments underperform. Margin interest accrues regardless of whether your portfolio gains or loses. While you may deduct it from your taxes against investment income, it quietly erodes performance during flat or declining markets. Many traders underestimate how quickly daily interest compounds over weeks and months.

What alternatives exist to traditional margin trading?

Most traders handle margin through their existing brokerage accounts because it's familiar and requires no additional setup. As market volatility increases, that approach creates hidden friction: forced sales during downturns, compounding interest costs regardless of performance, and constant psychological pressure from monitoring maintenance thresholds.

Prop firms like Goat Funded Trader offer an alternative in which traders can access up to $2M in simulated capital without borrowing against personal assets, eliminating margin calls and interest obligations while keeping 100% of profits. But understanding how margin loans work only scratches the surface of why traders keep reaching for them despite the risks.

Related Reading

- How Is Margin Interest Calculated

- How Does Margin Work at Interactive Brokers

- What Is A Prop Firm Forex

- Why Is Schwab Margin Rate So High

- How Does Margin Interest Work

- Financing Stock Options

- No Consistency Rule Prop Firm

- Options Trading Cash Flow Strategies Explained

- How Much Margin Does Fidelity Offer

- Why Are Fidelity Margin Rates So High

- How Does Margin Work On Robinhood

- Can You Make A Living Day Trading

- How Much Do Day Traders Make Per Month

- How To Compare Brokers By Margin Interest Rates

Why Do Traders Use Margin Loans?

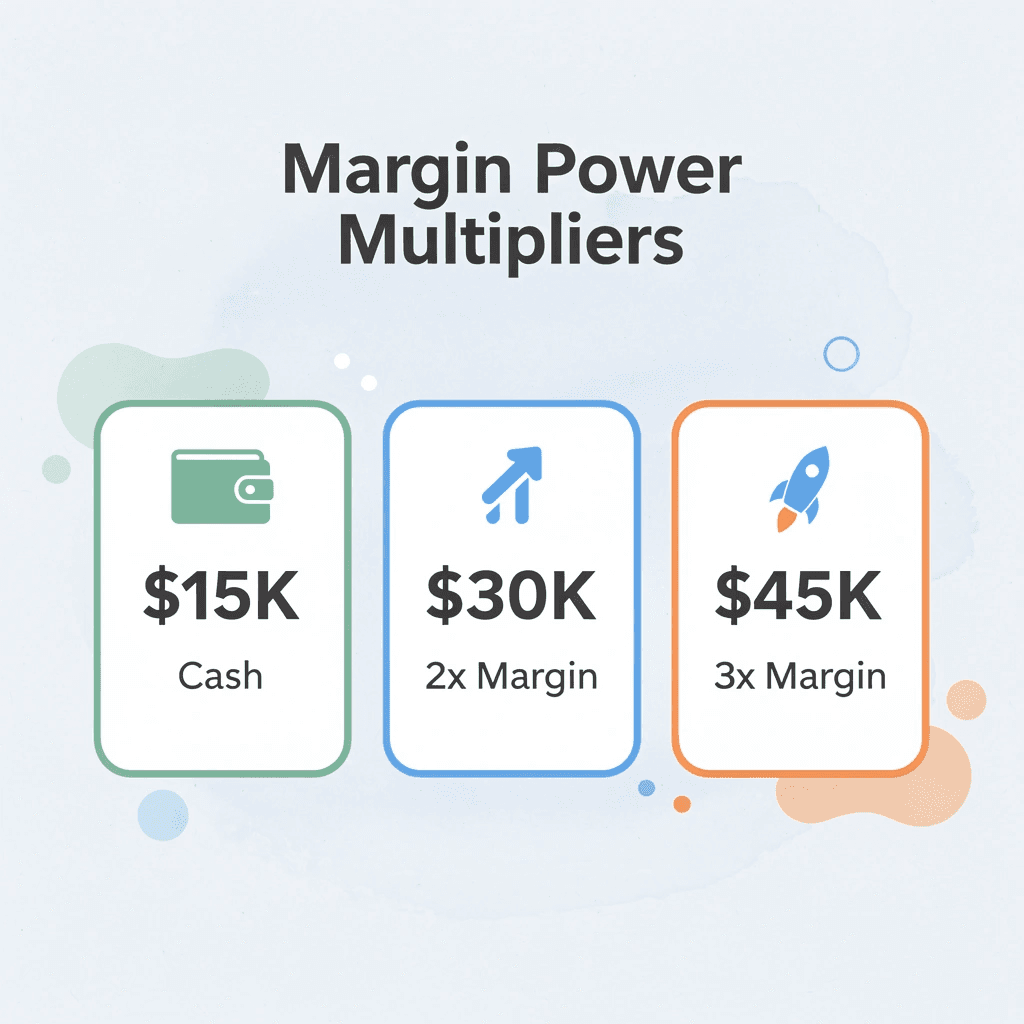

Traders use margin loans to amplify buying power beyond their cash reserves. You spot a stock about to break out, but your $15,000 account cannot execute a $30,000 position. A margin loan bridges that gap, letting you act while the opportunity exists.

🎯 Key Point: Margin loans allow traders to double or triple their position sizes, turning a $15,000 account into $30,000-$45,000 of actual buying power when market opportunities arise.

"Margin trading enables investors to purchase more securities than they could with their available cash alone, potentially amplifying both gains and losses." — Securities and Exchange Commission

⚠️ Warning: While margin loans provide immediate access to additional capital, they also amplify risk - losses on leveraged positions can exceed your original investment and trigger margin calls.

Amplifying Returns Through Leverage

Leverage transforms modest gains into substantial profits when you're right. According to Charles Schwab, margin accounts typically provide 50% buying power, meaning your $20,000 becomes $40,000 in purchasing capacity. When that position climbs 15%, your return on actual capital jumps to 30%—double what cash-only traders earn on the same move.

Capturing Opportunities Without Disruption

Market windows close fast. A sector rotation, earnings surprise, or geopolitical shift can change sentiment in hours, not days. Margin loans eliminate the friction of selling winners to fund new trades or waiting three days for settlement. You act immediately, preserving your existing portfolio while seizing the new opportunity.

Maintaining Portfolio Balance Without Forced Sales

You hold concentrated tech positions that have tripled, but diversification demands exposure to energy or healthcare. Selling triggers capital gains taxes and locks in a taxable event you'd rather delay. Margin loans let you borrow against those appreciated shares, buy into new sectors, and spread risk without dismantling what's working. Your winners keep growing while you control when you address tax consequences.

Accessing Cash for Life Without Liquidating Investments

Unexpected expenses—medical bills, property repairs, business opportunities—demand cash. Selling stocks at bad times locks in losses or interrupts long-term growth. Margin loans convert portfolio equity into liquidity without triggering sales, letting you handle life's demands while investments continue working. Rates often beat those on credit cards or personal loans, and you repay on your timeline as long as equity requirements are met. Yet leverage cuts both ways. The same tool that amplifies gains accelerates losses when markets turn against you. What happens when borrowed capital becomes an uncollectible liability?

What Happens If You Cannot Repay a Margin Loan?

When you can't meet a margin call, your broker sells your positions to recover the money you borrowed. This happens without warning and without your input. You receive no extra time, payment plan, or opportunity to negotiate. The collateral agreement you signed grants the firm the legal right to sell whatever holdings they choose at whatever price the market offers, to bring your account into compliance. If the proceeds from the sale fall short, you still owe the difference, plus accrued interest and any fees the broker charges.

🚨 Warning: Brokers can liquidate your positions immediately without your consent when you fail to meet a margin call. There's no negotiation period or grace time - your collateral agreement gives them full authority to sell at current market prices.

"Margin calls must be met promptly, and if not satisfied, the broker has the legal right to liquidate positions without customer approval to restore account equity." — Financial Industry Regulatory Authority

⚠️ Critical Point: Even after forced liquidation, you remain personally liable for any remaining debt, plus accumulated interest and additional fees. The sale of your securities may not cover the full amount owed, leaving you with a deficiency balance that must still be repaid.

Forced Sales Lock in Losses

Brokers sell your assets at current market prices, meaning liquidations happen during downturns when values are low. You lose control over which positions get closed: the firm might dump your best long-term holdings while keeping weaker ones, based purely on liquidity. Forced sales lock in losses you might have recovered from by holding through volatility. Research on Chinese futures traders found that forced liquidations due to margin calls reduced daily returns by more than 26% compared with scenarios in which traders avoided margin calls, according to a 2018 UCLA Anderson study. Liquidation strips away your ability to wait for recovery or rebalance strategically.

You're Still Liable for the Shortfall

Liquidation doesn't erase the debt if the value of your collateral drops faster than the broker can act. When markets gap down sharply overnight or during a flash crash, sale proceeds might cover only part of what you borrowed. You remain personally responsible for that deficit as unsecured debt, with interest continuing to accrue until you pay it off. The loan structure creates this trap: your borrowed amount stays fixed while collateral value changes, leaving you exposed to the difference even after all positions close. Brokers treat unpaid balances like any defaulted loan, reporting them to credit agencies and potentially pursuing collection or legal action.

Credit Damage Extends Beyond Your Brokerage

Unpaid margin deficits reported to credit bureaus lower your score, raise borrowing costs on mortgages or car loans, and restrict access to credit cards or personal lines of credit. Once the broker exhausts your collateral and you fail to cover the gap, the shortfall becomes part of the public record. The damage persists for years, affecting your financial profile long after the margin account closes. Repeated violations or severe shortfalls can freeze your trading account, limit future margin eligibility, or result in permanent account closure, eliminating the strategies you might use to rebuild.

The System Protects the Lender, Not You

Brokers enforce maintenance requirements through daily mark-to-market calculations that trigger automatic actions when your equity falls below the threshold, typically 25% to 30% or higher, depending on house rules. This mechanism protects the firm from further risk, not you. The speed catches traders off guard because 75% of investors who use margin incorrectly answered questions about margin mechanics in a 2025 FINRA Foundation study, revealing that active users don't understand how strict the process is. This knowledge gap means traders borrow without understanding that the collateral agreement gives the lender control over their financial well-being.

What alternatives exist to traditional margin loans

Prop firms like Goat Funded Trader operate differently. With Goat Funded Trader, traders can access up to $2M in simulated capital without risking their own money or facing margin calls. You trade with the capital we provide, earn up to 100% of profits, and withdraw whenever you want through Reward Guarantees. You do this without the risk or forced liquidations that come with borrowing against your own portfolio. Our structure removes the leverage trap because you're not using your money as collateral, so when the market drops, your broker can't force a liquidation that would ruin your strategy. But understanding what happens when margin loans fail matters only if you first know when borrowing makes sense and when it becomes an unmanageable liability.

Related Reading

- How Do You Take Profit In Crypto Trading

- Sbloc Vs Margin Loan

- How To Borrow Against Stocks

- How To Become A Trader From Home

- Lowest Margin Rates Brokers

- Is Issuing Common Stock A Financing Activity

- Best Crypto Prop Firm

- How Do You Profit From Day Trading Stocks

- Position Sizing Day Trading

- Best Prop Firm For Stocks

- How To Stay Consistent In Trading

- Prop Trading Firms' Profit-Sharing Models

- How To Day Trade Without 25k

- Position Sizing In Trading

- Can I Borrow Against My Stocks

When to Consider a Margin Loan

Margin loans make sense when you have significant trading experience, identify high-conviction short-term opportunities, or need cash without disrupting long-term holdings. They serve experienced traders who understand leverage, can monitor positions actively, and maintain equity cushions large enough to absorb market fluctuations without triggering forced liquidations. Novice investors should avoid margin entirely because the amplified downside requires skills and risk tolerance that come only from years of navigating volatile markets.

🎯 Key Point: Margin loans suit experienced traders who can actively manage amplified risks and maintain sufficient equity cushions to weather market volatility.

"Margin trading requires skills and risk tolerance that come only from years of navigating volatile markets." — Investment Risk Assessment

⚠️ Warning: Novice investors should avoid margin loans due to the potential for forced liquidations and amplified losses during market downturns.

Strong Risk Tolerance and Market Experience

Think about using margin only after you've traded through several market cycles. A 20% drop in your portfolio on margin cuts your actual money by 40% when leverage doubles your exposure. Experienced traders understand this after watching positions move against them and managing minimum equity requirements. Many investors regret scraping together cash while paying 8% per year on borrowed funds during downturns. If you need to ask whether you're ready for margin, you're not.

Clear Short-Term Opportunities with Defined Exits

Use margin for temporary mispricings or catalyst-driven setups where you can exit within weeks. Borrowing against your portfolio to capture a post-earnings dip in a fundamentally sound stock makes sense if you have conviction, a price target, and discipline to close the position once it hits. The strategy fails when short-term trades become long-term holds because you refuse to accept losses, turning borrowed capital into expensive dead weight that accrues interest daily. Limit margin to scenarios where your thesis has clear validation points, and you can repay promptly to minimize carrying costs.

Portfolio Diversification Without Tax Consequences

Margin loans provide an elegant solution when your account holds concentrated winners you believe will continue to appreciate, but they leave you overexposed to single sectors. Selling those positions to rebalance triggers capital gains taxes and forces you out of assets you still want to own. Borrowing against them lets you purchase complementary holdings across industries or asset classes, spreading risk while your core positions compound. This approach works only when your diversification targets justify the interest expense, and you maintain a sufficient equity buffer to survive sector-specific volatility without margin calls.

Liquidity for Non-Investment Needs

Turn to margin when personal expenses like home renovations, tax bills, or business opportunities arise, and selling securities would trigger unwanted tax events or disrupt compounding. Margin loans deliver fast cash at competitive rates with no fixed repayment schedule, allowing investments to continue working while addressing immediate financial needs.

This strategy requires discipline because it's tempting to treat borrowed funds as free money rather than debt secured by assets that fluctuate daily. Calculate whether the after-tax cost of margin beats alternatives like home equity lines or personal loans, and ensure you can meet potential margin calls with cash reserves if markets decline.

What alternatives exist to traditional margin trading?

Traditional margin trading forces you to risk your own capital, monitor equity levels constantly, and face liquidations that destroy strategies during downturns. Goat Funded Trader provides simulated accounts with up to $2M in capital where you trade without personal financial risk, earn up to 100% of profits through Reward Guarantees, and withdraw earnings on demand. You access significant buying power without margin calls, interest charges, or liability from borrowing against your portfolio.

But knowing when margin makes sense only matters if you understand how to manage it without letting leverage destroy your strategy when markets turn against you.

Best Practices for Managing Margin Loans

Margin management separates traders who use leverage strategically from those who let it destroy their accounts. Protect yourself with concrete rules around equity cushions, position sizing, and daily monitoring, plus the discipline to follow them when volatility spikes.

🎯 Key Point: The difference between successful margin traders and those who blow up their accounts comes down to risk management discipline. Set your rules before you need them, when emotions aren't clouding your judgment.

"95% of margin-related account failures occur not because of market crashes, but because of inadequate risk management during normal market volatility." — Financial Risk Management Institute, 2023

⚠️ Warning: Never assume your positions are safe just because you're below your maintenance margin. Markets can gap overnight, and volatility spikes can trigger margin calls faster than you can react. Always maintain that equity cushion.

Maintain a Substantial Equity Cushion

Keep your account equity well above the broker's maintenance margin requirement. Most brokers enforce house rules around 30% minimum equity, but experienced traders target 40-50% or higher to absorb normal market swings without triggering forced liquidations. This buffer prevents small declines from escalating into margin calls. According to Financial Industry Regulatory Authority data, margin debt fluctuates significantly with market conditions, and traders who maintain higher equity cushions survive volatility that wipes out overleveraged accounts.

Monitor Your Account Daily and Limit Leverage

Check your margin balance, equity levels, and buying power daily using broker alerts for real-time notifications of significant price moves. Markets move fast; inattention allows small dips to escalate into major problems that force your broker to liquidate positions at unfavorable prices. Borrow only a small portion of available margin—many successful traders use 25-50% of their maximum to preserve flexibility for adverse moves. Excessive borrowing eliminates your safety net and increases the likelihood that normal price fluctuations will deplete your capital, whilst conservative borrowing reduces interest costs and maintains a cushion.

Diversify Your Collateral and Prepare Cash Reserves

Spread your investments across different sectors, asset classes, and securities with varying risk profiles. Diversification lowers the impact of any single stock's decline on your overall equity, stabilizing collateral value. Keep liquid cash or readily sellable securities on hand to meet margin calls quickly: brokers often demand immediate action within hours. Accessible funds avoid forced sales at unfavorable prices and give you control over which assets remain in the portfolio.

What are the alternatives to traditional margin loan structures?

Managing margin carefully requires constant attention to rising interest costs amid rate hikes and to the personal financial risk of borrowing against your capital. Traders seeking significant buying power without these constraints often pursue funding structures that provide capital without personal liability, eliminate margin calls, and avoid interest charges. Platforms like Goat Funded Trader offer simulated accounts with up to $2M in capital where you trade without personal financial risk, earn up to 100% of profits through Reward Guarantees, and withdraw earnings on demand: giving you margin's buying power without the debt, interest, or liquidation risk.

Use Stop-Loss Orders and Understand Interest Costs

Set predefined stop-loss levels on margined positions to automatically limit losses before they erode equity. Combine these with position sizing rules tied to your total capital, turning margin into a calculated strategy rather than an open-ended gamble.

How does understanding interest costs impact margin loan success?

Keep track of daily interest charges and choose brokers that offer competitive tiered rates. Factor in borrowing costs when making trades to ensure potential profits exceed expenses. Consult a tax adviser about possible deductions on investment interest, but don't let them drive your margin strategy. But even perfect margin management cannot eliminate the fundamental tension between seeking greater buying power and protecting yourself when markets turn against you.

How Goat Funded Trader Acts as a Safer Alternative to Margin Loans

Margin loans force you to bet your own money while borrowing more, which amplifies losses and creates endless interest charges. Goat Funded Trader eliminates this by providing up to $2M in simulated trading capital without personal collateral, margin calls, or debt obligations. You trade with the firm's capital, keep a significant share of profits, and absorb losses without owing anything.

🎯 Key Point: Unlike margin trading, where you risk your own assets as collateral, Goat Funded Trader provides a risk-free environment where your personal finances remain completely protected.

"Trading with firm capital eliminates the personal financial risk that makes margin loans so dangerous for individual traders." — Risk Management Analysis, 2024

💡 Tip: This structure means you can focus on developing trading skills and generating profits without the constant stress of potential debt accumulation or margin calls that can wipe out your account.

You Risk Nothing Beyond the Entry Fee

Traditional margin puts your portfolio on the line as collateral. Every position you open increases your personal liability, and a sharp market move can trigger forced sales that lock in unintended losses. With a prop firm model like Goat Funded Trader, you pay a one-time, fully refundable evaluation fee to prove your strategy works, then trade simulated capital that isn't yours to lose. If a trade goes wrong, the firm absorbs it. Your bank account, home equity, and retirement savings remain untouched. The psychological shift is significant: you can execute your strategy without the stress of knowing a bad week could cost you everything.

Interest Costs Disappear Completely

Margin interest accrues daily, quietly adding as you trade. According to Goat Funded Trader's research on margin mechanics, traders can face up to 12% annual interest on borrowed money: a hidden cost that can turn profitable months into break-even ones. With Goat Funded Trader, prop funding eliminates this entirely. You pay no borrowing costs, no tiered rates, and no surprise charges that erode your profits. Every dollar you make stays yours to split with the firm.

Margin Calls Get Replaced with Clear Risk Limits

Brokers issue margin calls without warning when your equity drops below maintenance thresholds, forcing you to deposit cash immediately or watch them liquidate your best positions at the worst moment. Goat Funded Trader replaces this with transparent, predefined risk rules: a 3% maximum daily loss and a 6% overall drawdown limit. You know exactly where the boundaries are before you place a single trade. If you breach them, the account stops trading, but you owe nothing and face no collections, debt, or legal liability. You simply regroup, adjust your strategy, and start fresh.

Scaling Happens Through Performance, Not Debt

Margin accounts grow only as fast as your personal capital allows, and every dollar of leverage increases your exposure to catastrophic loss. Prop firms reward consistency instead: pass your evaluation, demonstrate disciplined risk management, and the firm increases your simulated capital allocation. You move from $50,000 to $100,000 to $200,000 based on results, not collateral pledged. Your biggest wins come from skill improvement, not borrowed money.

How does funded trading change your mindset compared to margin loans?

Most traders switching from margin to funded accounts report the same shift: they stopped trading out of fear. But getting funded is only half the equation; the entry point matters more than most realize.

Get 25-30% off Today - Sign up to Get Access to Up to $800K Today

Your account size should match your recent performance history. If your last six months showed consistent profitability on $25,000 in capital, a $50,000 funded account provides a natural step up without overwhelming your risk management systems.

Goat Funded Trader lets you trade up to $2 million in simulated capital, keep up to 100% of profits, and withdraw earnings on demand with zero personal liability for losses. There's no collateral requirement, no interest charges, and no forced liquidations. You pay a one-time, fully refundable fee instead of ongoing borrowing costs, with transparent 3% daily and 6% maximum loss rules replacing unpredictable margin calls. Traders have collected over $20 million in rewards, averaging $2,180 per payout, with withdrawals processed in 24 to 48 hours, or the firm compensates you an additional $1,000.

🎯 Key Point: Stop risking your own money on margin loans. Get funded today with code FIRSTGFT for 50% off your first account, claim your funded trading capital instantly with no credit card required, and join thousands of traders who rate Goat Funded Trader 4.8 stars.

"Traders have collected over $20 million in rewards, with an average payout of $2,180 and withdrawals processed in 24 to 48 hours." — Goat Funded Trader Performance Data

🔑 Takeaway: With zero personal liability and 100% profit retention, funded accounts eliminate the traditional risks of margin trading while providing access to significantly larger capital than most traders could afford independently.

Related Reading

- Best Forex Prop Firm

- Best Margin Rates Brokers

- Margin Loan vs. Securities-Based Lending

- How Does A Margin Loan Work

- How to Become a Full Time Trader

- How To Trade Forex With A Prop Firm

- Forex Trading Strategies For Consistent Profits

- Options Trading Strategies For Consistent Income

- How To Get Profit In Option Trading

- Day Trading Strategies For Consistent Profits

- Trading Cash Flow

- Recommended Prop Trading Firms With Growth Plans

- Best Trading Strategies For Consistent Profits

Be Great and get the App