How Does Margin Interest Work? All You Need to Know in 2026

How does margin interest work? Goat Funded Trader breaks down rates, calculations, and costs to maximize your trading profits in 2026.

.png)

Borrowing money to amplify trading positions can quickly turn profitable strategies into losing propositions when margin interest charges accumulate month after month. Many traders underestimate how daily interest on borrowed funds erodes their returns, especially during extended holding periods or when positions move against them. Understanding how brokers calculate these charges and when borrowing costs exceed potential gains separates successful traders from those who learn expensive lessons.

Smart traders recognize that risking personal capital while paying interest on borrowed funds creates unnecessary obstacles to profitability. Trading with firm capital eliminates margin interest concerns entirely, allowing traders to focus on strategy development and consistent execution without worrying about accumulating borrowing costs. This approach provides access to substantial trading accounts while avoiding the margin interest trap that catches many retail traders using a prop firm.

Summary

- Margin interest accrues every single day on your borrowed balance using a 360-day calculation, not the 365-day standard, which means brokers charge slightly more than the stated annual rate suggests. The fee applies from the moment you borrow until settlement clears, typically two business days after a sale, so even quick trades trigger interest charges during that gap. Brokers calculate interest daily on your debit balance and compound it before posting monthly, turning a seemingly small percentage into a measurable drag that erodes returns faster than most traders anticipate when opening leveraged positions.

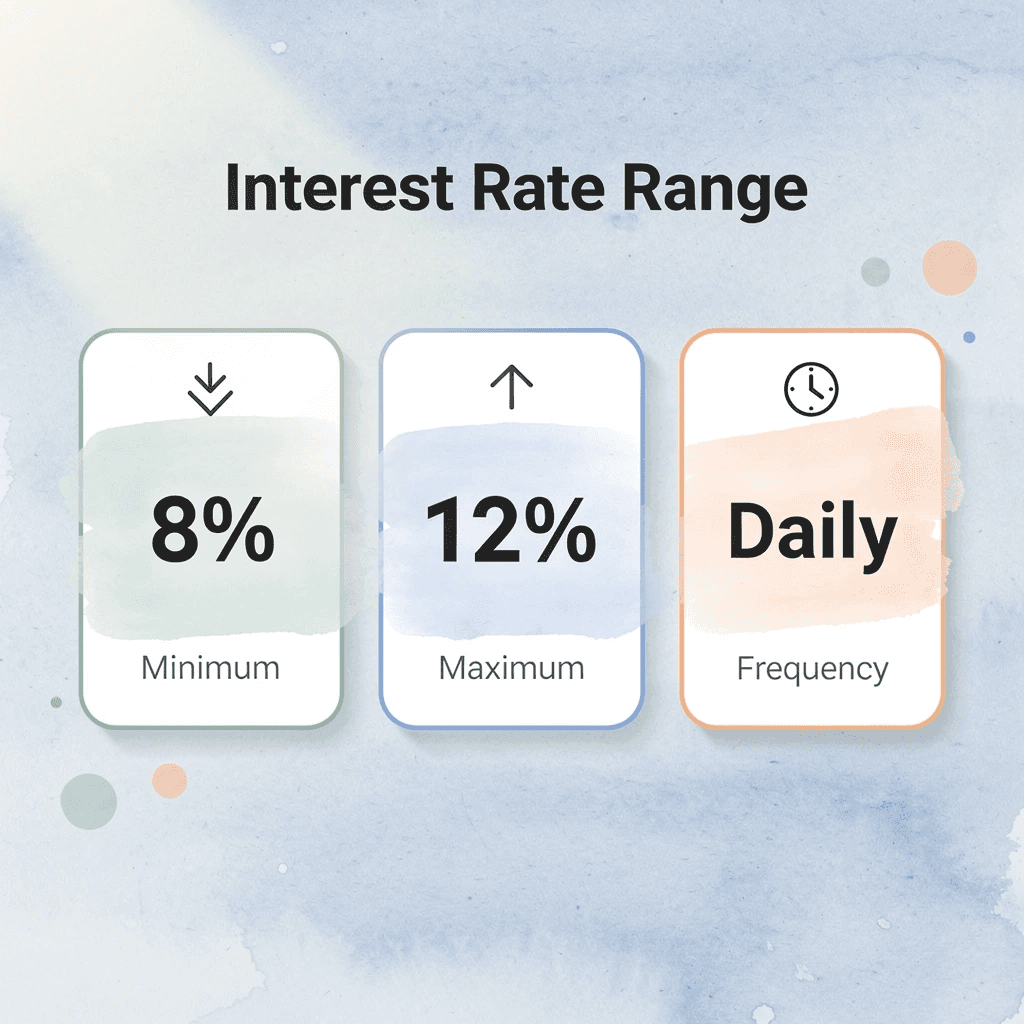

- Broker margin rates in 2026 range from around 3.99% at competitive platforms like M1 Finance to over 11% at traditional firms for smaller account balances, creating a cost spread that can exceed $1,400 annually on a $20,000 debit. Larger balances unlock lower-tiered rates, often dropping to 5%-7% for six- or seven-figure loans, while retail accounts with typical borrowing levels face the highest effective rates. Shopping brokers based on your expected debit balance and reviewing rate schedules quarterly as Fed policy shifts, can save hundreds to thousands in financing costs over a year of active trading.

- A study of Chinese futures traders using detailed brokerage records found that higher leverage produced a net annualized underperformance of 13% after costs, with borrowing expenses and frequent trading erasing gains and amplifying losses even for active accounts. The daily interest expense persists whether your trades win or lose, and it compounds faster than most traders calculate before entering positions. Profitable trades lose momentum when held through consolidations, and losing trades become significantly more expensive purely through the accumulation of financing charges that operate independently of market direction.

- Only 15% of margin traders correctly answered a basic question about how margin works in a 2015 FINRA-linked investor survey analyzed in an SEC staff working paper, compared to 31% of non-margin traders. This literacy gap leads traders to underestimate ongoing costs, confuse margin interest with margin requirements, and ignore the compounding effect of daily charges that continue accruing during settlement periods, weekends, and market closures. Understanding the mechanics before borrowing prevents expensive surprises when monthly statements reveal interest totals that turn breakeven trades into net losses.

- Margin interest cannot be avoided once you borrow money in a margin account because it accrues continuously on your outstanding debit balance, regardless of trade outcomes or market movements. The only way to stop the expense is to bring that balance to zero through cash deposits or security sales, and even then, interest continues running until the settlement clears two business days later. Traders who treat margin as permanent capital rather than a temporary, expensive tool watch silent daily charges compound over weeks and months, turning what seemed like cheap leverage into a measurable performance drag that requires aggressive paydown discipline to control.

- Goat Funded Trader provides simulated capital accounts up to $2M without margin loans or maintenance requirements, allowing traders to focus on performance and profit splits (80% to 100%) instead of tracking daily interest charges, debit balances, and compounding costs that erode returns in traditional margin accounts.

What Is Margin Interest in Trading, and How Does It Work?

Margin interest is the daily cost you pay to borrow money from your broker to trade securities. Interest accrues daily on the money you owe, regardless of whether your trade profits or loses money. The interest compounds before appearing in your account as a monthly charge.

🎯 Key Point: Margin interest accrues continuously from the moment you borrow funds, regardless of your trading performance. This means even profitable trades can become net losses if held too long with borrowed capital.

💡 Example: If you borrow $10,000 at 8% annual margin rate, you'll pay approximately $2.19 per day in interest charges, which compounds until you repay the borrowed amount.

"Margin interest is charged daily and compounds, making it one of the most significant hidden costs in leveraged trading." — Financial Industry Regulatory Authority (FINRA)

What Margin Interest Actually Is

Margin interest is the fee charged on money your broker lends you to buy stocks, options, or other securities in a margin account. Your existing portfolio serves as collateral, allowing you to control larger positions with less capital. Brokers set these rates based on their base rate, often tied to the broker call rate, plus a markup that adjusts with market conditions. You pay this interest for as long as the borrowed balance remains outstanding.

How Margin Loans Work in Practice

You open a margin account and meet the starting requirements, typically 50% of the purchase price under Regulation T. For a $10,000 stock position, you deposit $5,000 and borrow the rest. The broker holds your securities as collateral. As long as your account equity stays above maintenance levels (often 25-30%), you keep the borrowed funds. Interest accrues daily and is added to your account monthly. You reduce or eliminate the loan by depositing cash or selling positions.

How Brokers Calculate Margin Interest

Brokers calculate interest daily on the settled debit balance using: (Borrowed amount × Annual rate) ÷ 360 × Number of days. They apply tiered rates with lower percentages for larger balances and compound daily before monthly billing.

How do rate fluctuations affect your margin costs?

Interest rates change based on the broker's base rate and your average daily capital usage. Smaller accounts incur higher rates than six or seven-figure accounts.

What does current margin debt data reveal about interest costs?

U.S. margin debt reached $1.22 trillion in March 2026, up 38.7% year-over-year, according to FINRA data analyzed by Advisor Perspectives. This increase reflects growing use of leverage to finance trades. However, it highlights a concerning trend: when markets shift, investors face higher interest charges on borrowed funds. Many traders discover how these charges work only after seeing them on their statements.

Why do margin rates differ between brokers and account sizes?

Brokers compete on rates, with low-balance charges ranging from around 5% to over 11% annually in 2026, while larger loans often drop below 5-7%. Competitive platforms like Interactive Brokers or Robinhood offer some of the lowest tiers, while traditional firms charge more for smaller accounts. Your specific rate depends on the debit balance tier, and brokers may change base rates without notice. Comparing brokers based on your expected usage saves significantly over time.

How does margin interest work when trades extend longer than planned?

The familiar approach is to use margin as a temporary boost, planning to close positions quickly before interest accrues. As positions stretch from days into weeks or months, and market volatility forces you to hold longer than expected, interest charges compound quietly in the background.

Profitable trades lose momentum fast, and losing trades become significantly more expensive. While navigating these costs, Goat Funded Trader offers simulated trading accounts with up to $2M in capital, allowing you to focus on performance and profit splits rather than managing margin costs and personal capital exposure. You trade with substantial backing, earn profit splits up to 100%, and withdraw on demand without worrying about daily interest on borrowed funds. Understanding margin interest is only half the equation. The real confusion starts when traders mix up what they owe with what they must maintain.

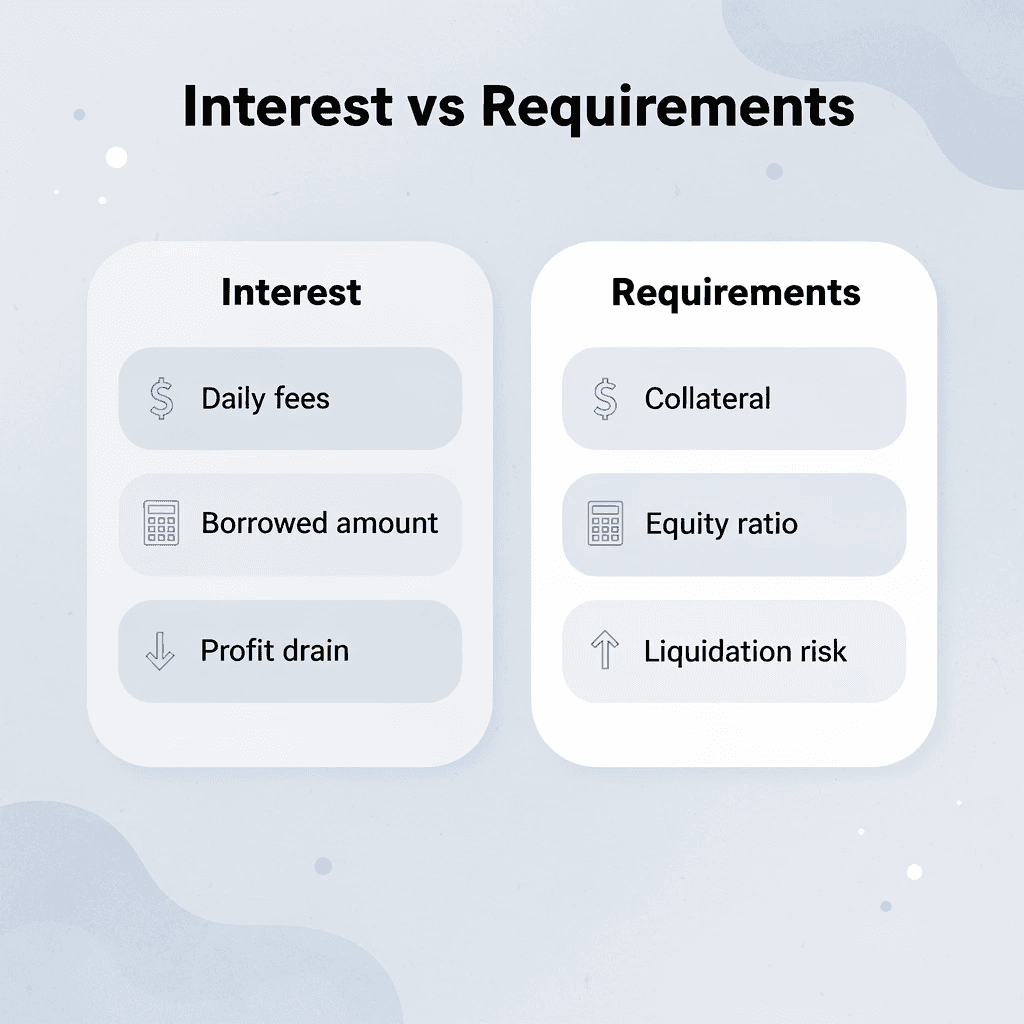

What Is the Difference Between Margin Interest and Margin Requirements?

Margin interest charges you for borrowing money; margin requirements determine how much collateral you must maintain. Interest drains your account through daily fees on the borrowed balance, while requirements trigger forced liquidations when your equity ratio drops below regulatory or broker-set thresholds.

🔑 Key Takeaway: Margin interest is the cost you pay for leverage, while margin requirements are the safety net that protects both you and your broker from excessive losses.

"Margin interest can significantly impact returns, with rates typically ranging from 8% to 12% annually on borrowed funds." — Financial Industry Analysis, 2024

⚠️ Warning: Many traders focus only on margin requirements but forget that daily interest charges can quickly erode profits, especially in volatile markets where positions may be held longer than anticipated.

Why the Distinction Matters During Market Volatility

When markets drop sharply, both systems activate simultaneously, compounding the problem. Your equity shrinks as positions lose value, pushing you closer to maintenance thresholds while interest accrues on the full borrowed amount. Traders often focus only on interest rates, overlooking the more dangerous risk that a 20% decline could trigger a margin call, forcing immediate liquidation at the worst possible moment. Forced sale locks in losses and leaves you owing the broker the remaining debt plus accumulated interest.

How Initial Requirements Cap Your Leverage from Day One

Charles Schwab requires a 50% initial margin requirement on most securities, meaning you must put down half the purchase price upfront. To buy $40,000 in stock, you contribute $20,000 and borrow the rest. This rule limits your maximum buying power from the start. Brokers may require more cash on volatile or low-priced stocks, sometimes demanding 75% or 100% cash, which can block margin use entirely on risky positions.

How Maintenance Requirements Force Action During Declines

After you open a position, maintenance margin requires your equity to stay above a minimum percentage of the current market value. FINRA sets a 25% minimum, though most brokers enforce house rules of 30% to 40%. If your $40,000 position falls to $28,000 while you owe $20,000, your equity drops to $8,000 (28.5% of market value). At a 30% house requirement, the broker issues a margin call demanding $400 or forces liquidation of your positions.

Why Interest Compounds the Problem Quietly

Margin interest accrues daily on borrowed funds, regardless of price movements. A $20,000 loan at 12% annual interest costs approximately $6.58 per day, or $197 per month.

How does margin interest work to erode profits over time?

If you hold a position that doesn't move for six months, you pay $1,184 in interest alone. This reduces your net returns even if the stock eventually rises. Traders holding leveraged positions during consolidations watch this silent expense erase weeks of gains, turning breakeven trades into net losses due to borrowing costs alone.

What alternatives eliminate margin interest costs completely?

Platforms like prop firm solve both problems by providing simulated capital accounts up to $2M without margin loans or maintenance requirements. With Goat Funded Trader, you trade with substantial backing, earn profit splits up to 100%, and withdraw whenever you want without daily interest or forced liquidations during drawdowns.

Related Reading

- Capital Growth Trading

- How Does Margin Work On Robinhood

- Can You Make A Living Day Trading

- How Much Do Day Traders Make Per Month

- How Much Margin Does Fidelity Offer

- How To Compare Brokers By Margin Interest Rates

- How Is Margin Interest Calculated

- How Does Margin Interest Work

- No Consistency Rule Prop Firm

- Options Trading Cash Flow Strategies Explained

- Financing Stock Options

- Why Are Fidelity Margin Rates So High

- How Does Margin Work at Interactive Brokers

- Why Is Schwab Margin Rate So High

- What Is A Prop Firm Forex

Can Margin Interest Be Avoided?

Margin interest cannot be avoided once you borrow in a margin account. It accrues daily on the money you owe using a 360-day calculation and stops only when you bring that balance to zero through deposits or selling securities. Your broker lends you money backed by your securities, and that loan costs you money daily, regardless of how the market moves or your trades perform.

🎯 Key Point: Unlike other trading costs that are one-time fees, margin interest is a continuous expense that accumulates 24/7 until your borrowed balance reaches zero.

"Margin interest accrues daily using a 360-day year calculation, making it a persistent cost that continues regardless of market performance." — Financial Industry Standards

⚠️ Warning: Many traders underestimate the cumulative impact of daily interest charges, especially during volatile market periods when positions may be held longer than anticipated.

Why Traders Believe They Can Sidestep the Cost

The assumption feels reasonable at first: pay off the loan fast, hold positions for a few hours, or switch to a platform advertising rock-bottom rates, and the expense should disappear or shrink to nothing. Traders treat margin interest as negotiable rather than a fixed result of leverage. This thinking collapses when monthly statements arrive showing hundreds or thousands in charges that accumulate while positions stay open. Standard margin accounts require 50% of your portfolio value as collateral, but that threshold does nothing to stop interest accruing on the borrowed half.

The Daily Compounding Reality

Interest accrues daily from when you borrow money, even for overnight positions. When you sell stocks, your principal decreases only after the sale settles (usually two business days), so the money you owe continues to accrue interest during that waiting period. Brokers charge these fees monthly, and they accumulate over time: a $50,000 debt at 10% costs you $5,000 per year in charges that short-term trades rarely overcome after taxes and price changes. An SEC staff working paper examining a 2015 FINRA-linked investor survey found that only 15% of margin traders could correctly answer a basic question about how margin works, compared to 31% of traders who don't use margin. This gap in understanding leads traders to underestimate these ongoing costs.

When the Expense Actually Stops

Margin interest persists until your debit balance reaches zero. You can sell positions, deposit cash, or transfer securities to eliminate the loan entirely. Until then, interest accumulates daily, adding to your cost basis with each day you use borrowed money. This requires treating borrowed funds as temporary, expensive capital. Prop firms like Goat Funded Trader eliminate borrowing by providing simulated capital accounts up to $2M without margin loans, letting you focus on performance and profit splits instead of tracking daily interest charges that reduce your returns before the position closes.

The Hidden Drag on Performance

A study of Chinese futures traders using detailed brokerage records found that higher leverage produced a net annualized underperformance of 13% after costs. Broker rate comparisons in 2026 show standard margin rates at major firms ranging from 5% to over 11% for typical balances, with many retail accounts facing 10%+ tiers. This fixed drag persists whether your trades win or lose and compounds faster than most traders calculate before entering positions. Understanding how to measure an interest's true impact on every trade is essential.

6 Smart Strategies to Manage Margin Interest Efficiently

Managing margin interest efficiently means treating borrowed funds like a meter that keeps running. You control costs by choosing the right broker tier, limiting how long you keep the borrowed money, and paying down balances faster than interest builds up. These six strategies turn borrowing from something that eats into profits into a tool you can plan for.

🎯 Key Point: The difference between profitable margin trading and costly mistakes often comes down to how actively you manage your interest expenses rather than letting them accumulate unchecked.

"Margin interest can turn a winning trade into a losing proposition if traders don't actively manage their borrowing costs and repayment timeline." — Financial Trading Research, 2024

⚠️ Warning: Many traders focus only on entry and exit points while ignoring the ongoing cost of their borrowed capital – this oversight can eliminate profit margins even on successful trades.

1. Select Brokers with the Lowest Tiered Rates

Broker margin rates vary based on loan size. M1 Finance charges as low as 3.99% on larger balances, Interactive Brokers Pro accounts around 5.33%, and Robinhood near 5.05%, while traditional brokerages charge 10% or higher for smaller loans.

How does margin interest work when comparing broker costs?

Check the tier breakpoints at your current broker. Calculate what your typical debit balance would cost at three competitors. Move your account if the savings exceed $500 annually. Rates shift quarterly with changes in Fed policy, so review every three months. The difference between 5% and 10% on a $20,000 debit over 90 days is $250 in pure cost. That gap widens when positions stay open longer, or balances grow.

2. Limit Borrowing to Short-Term Trades Only

Interest accrues daily on borrowed amounts, so holding leveraged positions for weeks converts small percentage costs into substantial dollar losses. Use margin only for trades you plan to execute within days, where expected profits clearly exceed daily interest, slippage, and taxes. Close positions once you reach profit targets and immediately use proceeds to pay down the loan. A $10,000 margin position held for 30 days at 10% costs $83 in interest. The same position closed in three days costs $8. Financing costs multiply tenfold based solely on hold time.

3. Maintain Conservative Leverage and Strong Equity Buffers

Borrowing the maximum allowed leaves no room for market changes or risks, or for margin calls that force sales at bad prices. Fund 70% to 75% of positions with your own capital and borrow only 25% to 30%, which lowers daily interest and keeps equity well above maintenance requirements. Set personal equity alerts at least 10% higher than broker minimums and monitor daily. This buffer absorbs volatility without triggering forced liquidations, reduces interest costs, and prevents the compounding crisis in which falling equity and rising interest rates collide during drawdowns.

4. Pay Down Debit Balances Aggressively After Every Sale

When you settle a sale, the money automatically reduces your margin loan. You can also make extra cash deposits to pay down the loan faster. Check your account daily and move any extra cash or profits directly against the loan, rather than using borrowed money for your next trade. Paying down the loan regularly shrinks the daily interest calculation and can move you into a lower rate tier, creating a positive cycle that protects your profits. Don't keep using the same amount of leverage out of habit; doing so lets interest build up on the same borrowed amount month after month.

5. Diversify Collateral and Use Stop-Loss Discipline

A concentrated portfolio on margin amplifies single-stock risk and triggers margin calls more quickly when holdings decline. Spread positions across uncorrelated assets so a decline in one area doesn't threaten the entire account's equity ratio. Pair this with strict stop-loss orders placed at entry to exit losing trades before they erode equity and increase borrowing costs. Disciplined exits keep the debit balance lower, and diversification prevents a single bad position from forcing liquidation across the entire account.

6. Leverage Prop Firm Funding for High-Volume Trading Without Personal Interest Costs

Prop firm funding gives traders access to large amounts of simulated money with strict risk rules, eliminating margin interest costs. Traders demonstrate consistency on simulated accounts with set drawdown limits, then receive real profit splits (often 80% to 100%) while the firm funds the capital. Our model lets traders scale positions without margin costs. This setup lets skilled traders control large positions, capture significant gains, and grow their trading without paying ongoing margin interest.

What funding levels are available without personal capital risk?

Goat Funded Trader funds qualifying accounts up to $800,000 or more in advanced tiers with no personal capital at risk. You focus entirely on execution and risk management rather than calculating daily interest drag or managing broker rate tiers.

How does margin interest work as a controlled business expense?

Learn how to use margin strategies and handle interest changes. Rather than viewing margin as an unavoidable burden, treat it as a manageable business cost. Track your daily debt, calculate interest before each trade, and manage borrowed money carefully. Your investments will perform better over time when you control leverage instead of letting it control you.

Related Reading

- Prop Trading Firms' Profit-Sharing Models

- How To Stay Consistent In Trading

- How Do You Take Profit In Crypto Trading

- How To Borrow Against Stocks

- Is Issuing Common Stock A Financing Activity

- Best Crypto Prop Firm

- Best Prop Firm For Stocks

- How To Day Trade Without 25k

- How Do You Profit From Day Trading Stocks

- Lowest Margin Rates Brokers

- Position Sizing Day Trading

- How To Become A Trader From Home

- Can I Borrow Against My Stocks

- Position Sizing In Trading

- Sbloc Vs Margin Loan

How Goat Funded Trader Helps Traders Manage Margin Interest Efficiently

Borrowed money often creates more financial problems than market movements themselves. According to Goat Funded Trader, traditional margin accounts require a minimum of $2,000 equity to borrow and charge daily interest that compounds regardless of trade performance. Interest accrues continuously, even on winning positions, quietly reducing returns before withdrawal.

🎯 Key Point: Goat Funded Trader eliminates the margin interest burden by providing traders with funded accounts that don't require personal borrowing or daily interest charges.

"Traditional margin accounts require a minimum $2,000 equity to borrow, then add daily interest that compounds regardless of trade performance." — Goat Funded Trader, 2024

🔑 Takeaway: By removing margin interest from the equation, Goat Funded Trader allows traders to focus purely on market performance rather than managing compound interest costs that erode profitability.

The Zero-Interest Capital Model

Goat Funded Trader eliminates margin interest by providing simulated funded accounts up to $2 million after passing evaluation programs. You trade the firm's capital with no personal debt balance, daily interest calculations, compounding charges, or monthly billing cycles. A trader who borrowed $50,000 at 8% through a traditional broker paid over $4,000 annually; the same trader using our funded capital keeps 80-100% of gains with zero carrying costs. We absorb simulated losses while you focus on execution strategy instead of calculating how many days you can afford to hold a position before interest erodes your edge.

Fixed Risk Rules Replace Margin Call Pressure

Traditional margin accounts force you to sell positions when your equity drops and charge interest on borrowed funds. Prop firm funding works differently with set limits: a 4% maximum daily loss and a 6% overall maximum loss on simulated capital. With Goat Funded Trader, you know exactly where the limit is before you trade, so you won't face surprise margin calls or emergency deposit requirements. Your personal money stays completely safe regardless of trading outcomes.

Rapid Payouts That Lock In Gains

Interest on borrowed money accrues continuously in regular accounts, reducing your net earnings even during withdrawals. Prop firms offer rewards payable on demand with a guarantee: receive payment within 24 hours or the firm pays you an extra $1,000. Standard payouts take two business days, with the same bonus if delayed. You can withdraw funds via bank transfer, cryptocurrency, Skrill, or local methods without interest charges, reducing your payout.

Flexible Strategy Execution Without Compounding Costs

Weekend holds and news event trading in margin accounts incur interest charges, forcing early exits. Prop firms allow news trading, weekend holding, and unlimited trading periods. With Goat Funded Trader, you run your complete strategy on MT5 with tight spreads and up to 1:100 leverage, capturing opportunities that margin interest penalties would otherwise prevent. The result is higher win rates and larger profitable trades without daily cost calculations limiting traditional margin trading. Accessing this zero-interest structure requires passing a specific evaluation process.

Related Reading

- Best Trading Strategies For Consistent Profits

- How Does A Margin Loan Work

- How To Get Profit In Option Trading

- Day Trading Strategies For Consistent Profits

- Best Margin Rates Brokers

- How To Become A Full-Time Trader

- Options Trading Strategies For Consistent Income

- Trading Cash Flow

- Recommended Prop Trading Firms With Growth Plans

- Margin Loan vs. Securities-Based Lending

- Best Forex Prop Firm

- Forex Trading Strategies For Consistent Profits

- How To Trade Forex With A Prop Firm

Get 25-30% off Today - Sign up to Get Access to Up to $800K Today

You now understand how margin interest works: the daily charges, compounding costs, margin calls, and forced liquidations that destroy profits even on winning trades. Those interest payments drain your account month after month, limiting your position size and capping your true potential.

Goat Funded Trader ends this cycle completely. Our platform provides access to up to $2 million in simulated capital after a simple evaluation. You trade our firm's capital on MT5 with zero personal borrowing, zero debit balances, and zero margin interest. Strict but fair rules—including a 4% maximum daily loss and 6% overall maximum loss—replace traditional broker margin requirements. You face no calls, no forced sales, and no interest drag.

🎯 Key Point: You keep up to 100% of your profits with paid-on-demand withdrawals. Get paid within 24 hours, or we add an extra $1,000. Standard rewards arrive in two business days, or we pay the $1,000 bonus. Scale your account as you perform, all while staying completely protected from losses.

"Join 250,000+ traders who already receive clean payouts without the hidden costs of margin interest." — Goat Funded Trader, 2024

Stop paying retail brokers to lend you money. Start trading like the greatest with Goat Funded Trader today. Use code FIRSTGFT for 50% off your first account with no credit card required, and the fee is 100% refundable.

🔑 Takeaway: Join 250,000+ traders who already receive clean payouts without the hidden costs of margin interest. Visit Goat Funded Trader to get started now.

Be Great and get the App

.webp)