Why Are Fidelity Margin Rates So High for Traders in 2026?

Why Are Fidelity Margin Rates So High? Goat Funded Trader reveals the real reasons behind 2026's costly margin fees and better alternatives.

.png)

Margin interest can significantly erode trading profits, especially when pursuing Capital Growth Trading strategies with borrowed funds. Fidelity's margin rates typically range from 7% to over 12%, depending on account balance tiers, and these fees compound daily regardless of market performance. Understanding these costs and exploring alternatives can help traders protect their capital while maintaining growth opportunities.

Traders can access substantial capital without daily interest charges through evaluation-based funding models. After demonstrating trading skills through an assessment process, traders can focus on strategy execution rather than watching interest fees accumulate, making this an attractive alternative for those seeking growth opportunities without the burden of traditional margin costs through a prop firm.

Key Takeaways

- Margin trading magnifies both gains and losses while adding daily interest charges that compound until you repay the loan or close the position. Fidelity enforces a 30% maintenance requirement above the 25% FINRA minimum, meaning your equity must stay at least 30% of your total position value at all times, or you face forced liquidation. These stricter thresholds create a narrow margin for error where a 10% market dip can trigger automatic sell-offs that lock in losses at the worst possible moment.

- Small-account holders pay the highest margin rates at traditional brokerages due to tiered pricing structures that reward scale over accessibility. Fidelity charges 11.825% for balances under $25,000 but drops to 7.50% once borrowing exceeds $1 million, creating a four-percentage-point spread that penalizes newer traders. Borrowing $25,000 at Fidelity's base rate costs about $3,041 annually compared to $1,273 at discount brokers offering 4.90% rates, a $1,768 gap that drains returns before accounting for any market performance.

- Most traders who use margin don't actually understand how it works, which creates catastrophic risk when volatility strikes. A FINRA Foundation survey found that only 15% of margin traders answered a basic question about margin mechanics correctly, compared to 31% of non-margin traders. This knowledge gap means users borrow before they grasp the consequences of leverage, interest accrual, and forced liquidation rules that activate during market stress.

- Pattern day trading restrictions impose a $25,000 minimum equity requirement on accounts that execute four or more day trades within five business days. Drop that threshold below, and brokers freeze your ability to open new positions, creating a frustrating middle zone where you have margin access but can't use it as active strategies demand. This regulatory barrier forces traders to either park capital they might need elsewhere or abandon short-term tactics entirely.

- Interest costs on margin loans compound daily and post monthly, turning tactical leverage into a structural drag on performance when positions stay open longer than planned. A 10% return on a leveraged trade can shrink to 6% after interest, especially when rates rise, or borrowed amounts fall into higher-tier brackets. Shorter holding periods minimize this expense, but the rate disadvantage remains unless you scale borrowing into tiers where institutional pricing finally becomes competitive.

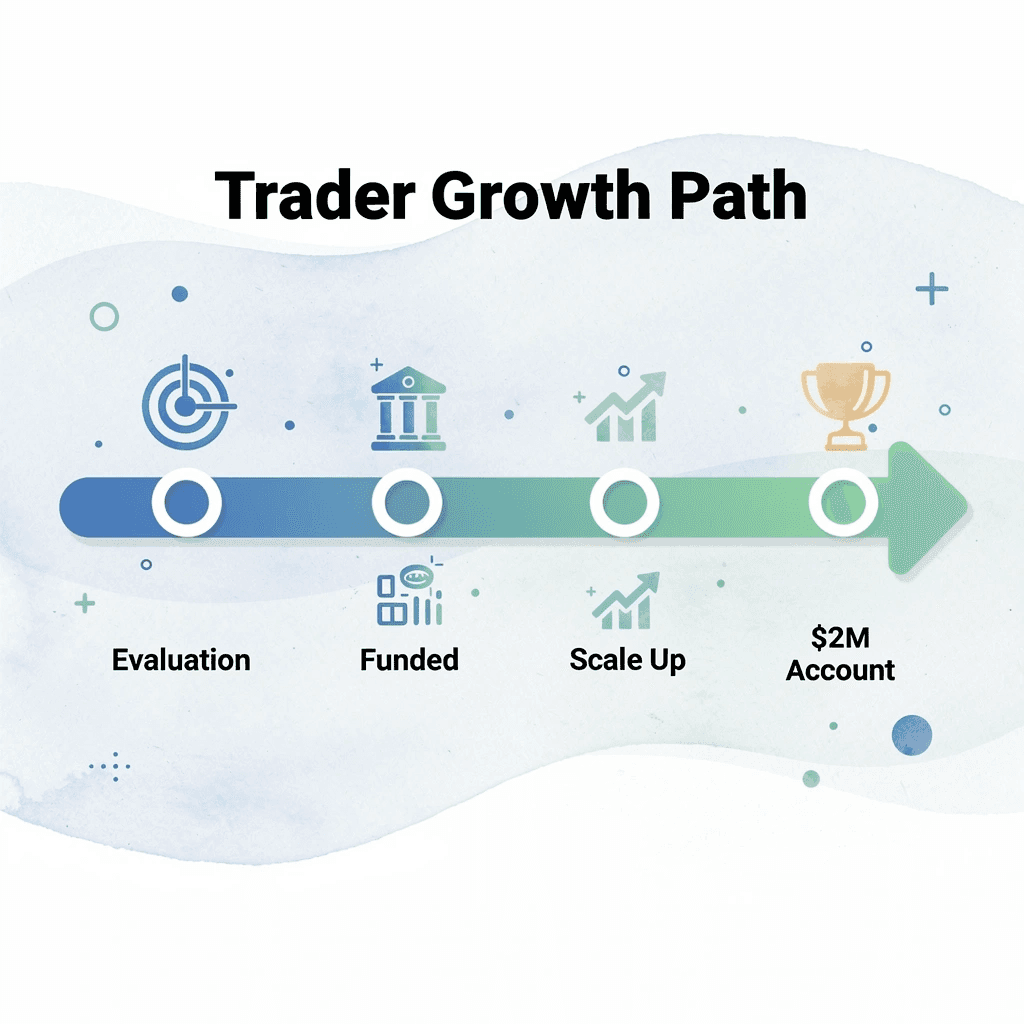

- Goat Funded Trader addresses this by providing simulated trading capital up to $2 million with no margin interest, no personal capital at risk, and 100% profit splits that let traders scale position sizes without the daily cost bleed or liquidation threats that come with traditional margin accounts.

What is Margin Trading, and How Does It Work?

Margin trading lets you borrow money from your broker to buy stocks and bonds beyond your cash balance. You deposit part of the purchase price as collateral while the broker funds the remainder. This lets you control a larger position than your capital alone could support. This leverage magnifies both gains and losses, and adds daily interest charges that compound until you repay the loan or close the position.

🎯 Key Point: Margin trading is essentially using borrowed funds to amplify your buying power, but remember that leverage works both ways - it can multiply your gains just as easily as your losses.

"Margin trading allows investors to purchase securities worth more than their available cash, but it significantly increases both potential returns and potential risks." — Securities and Exchange Commission

💡 Example: If you have $5,000 in cash and want to buy $10,000 worth of stock, you could use 50% margin to borrow the remaining $5,000 from your broker, putting up your existing $5,000 as collateral.

The Mechanics Behind Borrowing to Trade

You open a margin account with your brokerage and deposit cash or securities as collateral. When you spot an opportunity, the broker extends credit for the balance beyond your contribution. Charles Schwab requires a 50% initial margin on most stock purchases, so a $10,000 trade means you supply $5,000 while borrowing the other half. Your holdings serve as collateral for the loan, and the broker continuously monitors their value. If the position rises, you sell, repay the borrowed funds plus accrued interest, and keep the larger profit. If it falls, your equity shrinks faster than in a cash account, and significant declines trigger forced actions from the firm.

Maintenance Requirements and Forced Exits

Once you hold a leveraged position, you must keep your account equity above a minimum threshold. Charles Schwab enforces a 25% minimum maintenance requirement, meaning your equity cannot drop below one-quarter of the total market value of your securities. When volatility pushes your equity below that floor, you receive a margin call demanding immediate cash or collateral deposits. If you fail to respond, the broker automatically sells your positions to cover the loan, locking in losses at the worst moment. A 10% market dip can trigger this cascade when leverage is high.

Interest Costs That Compound Quietly

Margin debt carries daily interest charges that vary by broker, account size, and current rates. Unlike mortgages with fixed payments, margin loans lack a set repayment schedule. You owe interest until you sell securities or deposit enough cash to cover your debt. Positions held for weeks or months accumulate interest that reduces your gains. A 10% return on a leveraged trade can shrink to 6% after interest, particularly when rates rise, or you've borrowed substantially.

Why Traders Accept the Risk

Leverage turns moderate conviction into portfolio impact. If you believe a stock will jump 15% next week but only have $5,000 available, margin lets you control $10,000 worth, doubling your absolute gain if correct. It also enables strategies like short selling and lets you capitalize on time-sensitive opportunities without liquidating other holdings. With strict stop losses and position limits, it becomes a tool for growing returns without waiting years to accumulate additional capital.

Why do most traders misunderstand margin mechanics?

Most traders open margin accounts confident they understand the rules, only to discover how margin actually works when a margin call arrives. According to a FINRA Foundation survey on U.S. investors, only 15% of margin traders correctly answered a basic question about how margin works, compared to 31% of non-margin traders.

This gap shows how many people borrow money before understanding the consequences of leverage, interest, and forced liquidation. The traditional model asks you to assume all risk and cost, while the broker collects daily interest. Prop firms restructure this arrangement—Goat Funded Trader, for example, provides simulated capital up to $2M after you pass an evaluation. This eliminates margin interest and personal capital requirements while you keep 100% of profit splits. You trade with substantial buying power, but the downside risk remains with the firm, not your savings account.

How does access to leverage determine the success of a strategy?

Understanding how something works is only half of what you need to know; knowing how much leverage you can access determines whether the strategy fits your goals.

Related Reading

- Capital Growth Trading

- How Does Margin Work On Robinhood

- Can You Make A Living Day Trading

- How Much Do Day Traders Make Per Month

- How Much Margin Does Fidelity Offer

- How To Compare Brokers By Margin Interest Rates

- How Is Margin Interest Calculated

- How Does Margin Interest Work

- No Consistency Rule Prop Firm

- Options Trading Cash Flow Strategies Explained

- Financing Stock Options

- Why Are Fidelity Margin Rates So High

- How Does Margin Work at Interactive Brokers

- Why Is Schwab Margin Rate So High

- What Is A Prop Firm Forex

How Much Margin Does Fidelity Offer?

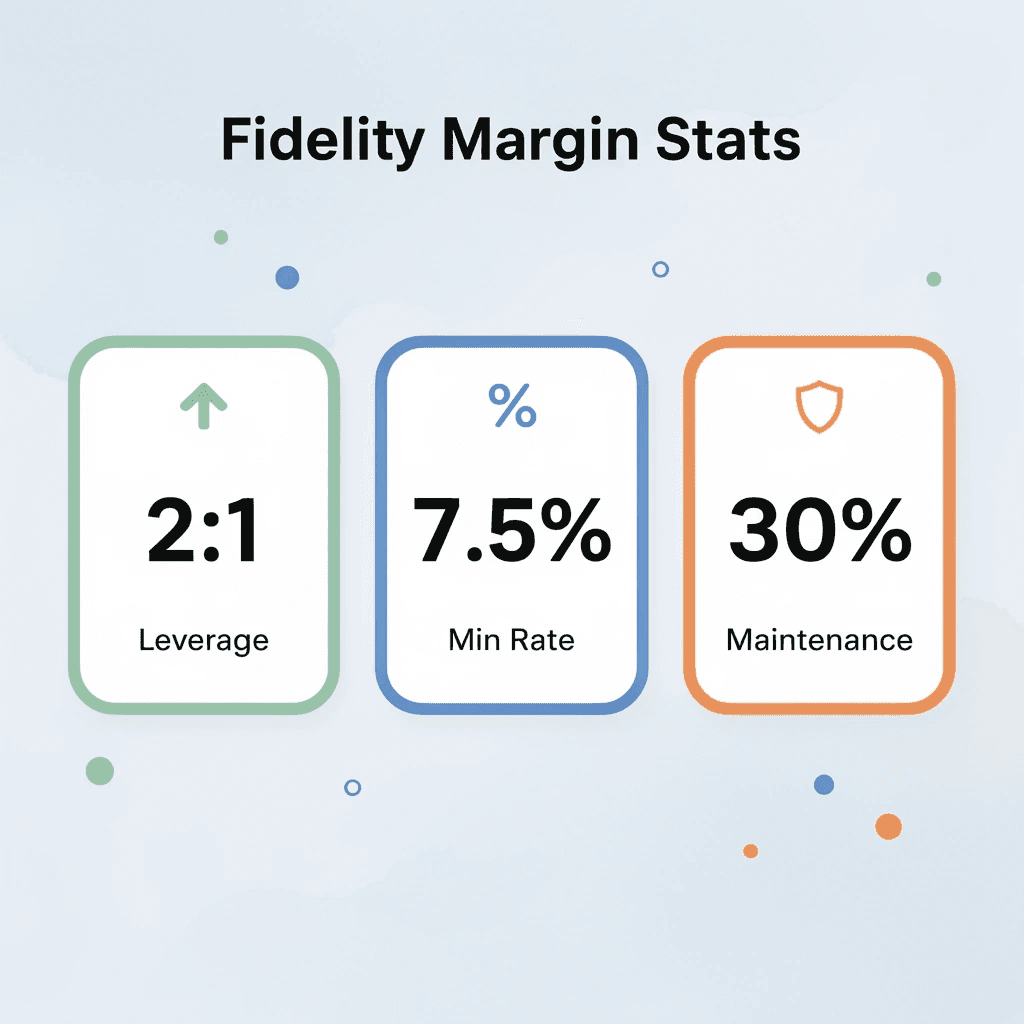

Fidelity offers standard 2-to-1 leverage on most securities through its margin program. With $10,000 in your account, you can access $20,000 in buying power because Fidelity lends you the remainder at rates ranging from 7.50% to 11.825%, depending on your debit balance. This follows Regulation T's 50% initial margin requirement, but Fidelity enforces a stricter 30% maintenance threshold to prevent forced liquidations.

"With $10,000 in your account, you can access $20,000 in total buying power through Fidelity's 2-to-1 leverage margin program."

🔑 Key Takeaway: Fidelity's 30% maintenance threshold is more conservative than many brokers, providing additional protection against market volatility but requiring closer monitoring of your positions.

⚠️ Warning: The interest rates ranging from 7.50% to 11.825% can significantly impact your returns, especially on longer-term margin positions where borrowing costs accumulate over time.

The $2,000 Floor and the $25,000 Wall

You need at least $2,000 in equity to qualify for margin borrowing at Fidelity. If you execute four or more day trades within five business days, your account gets flagged as a pattern day trader, triggering a $25,000 minimum equity requirement that persists as long as you maintain that trading pattern. If you drop below $25,000, Fidelity restricts new positions, freezing your strategy mid-execution. This creates a frustrating middle zone where you have margin access but cannot use it as active traders need.

What are Fidelity's maintenance requirements, and how do they change

Fidelity's 30% house maintenance requirement exceeds the 25% FINRA minimum, meaning your equity must remain at least 30% of your total position value. When a stock drops and your equity falls below that threshold, you receive a margin call demanding immediate cash or securities to restore the balance. Fidelity adjusts these requirements dynamically for concentrated positions, volatile stocks, or options strategies. A position that met the requirements yesterday can trigger a call today based on a real-time risk assessment, not on price movement alone.

How do traditional margin costs compound as strategies scale

The traditional approach borrows against your portfolio to increase position sizes, accepting daily interest charges and margin calls as costs of leverage. As your strategy grows and volatility increases, interest costs accumulate while maintenance requirements tighten, forcing constant equity monitoring or risking forced liquidations that lock in losses. Platforms like Goat Funded Trader eliminate that structure by providing simulated capital of up to $2M with no margin interest, no personal capital at risk, and 100% profit splits that reward performance rather than penalize leverage.

Tiered Interest Rates That Penalize Small Accounts

Fidelity's margin rates follow a tiered structure tied to your debit balance, with the base rate at 10.575%. Balances under $25,000 incur a 11.825% rate, while those over $1 million drop to 7.50%. This four-percentage-point spread means smaller traders pay nearly 60% more in interest costs than larger accounts. Since interest accrues daily and compounds monthly, these charges erode your returns continuously.

The friction stems from the way Fidelity prices the margin.

Why Are Fidelity Margin Rates So High?

Fidelity structures margin rates around a tiered model that rewards scale. The base rate is 10.575% (as of December 2025), rising to 11.825% for accounts under $25,000. This pricing reflects operational costs, regulatory capital reserves, and Fidelity's full-service infrastructure: research tools, live support, and platform stability. Leaner discount brokers skip these offerings. The rates reveal who Fidelity wants to serve and how it funds those services.

🔑 Key Point: Fidelity's margin rates are structured to favor larger accounts while covering the costs of their premium infrastructure that budget brokers don't provide.

"The base rate is 10.575% (as of December 2025), rising to 11.825% for accounts under $25,000." — Fidelity, 2025

⚠️ Warning: Smaller accounts pay over 1% more, making Fidelity's margin less competitive for retail traders with limited capital.

The Real Funding Mechanism

Fidelity borrows short-term capital at the broker call rate, which was around 7.25% in late 2024 and early 2025, according to Federal Reserve-linked analyses. It then adds 3 to 5 percentage points to cover regulatory requirements, customer service, and risk management. Fidelity applies this markup through published tiers rather than hiding fees in fine print. The structure encourages efficient capital use because every dollar below $25,000 is subject to the steepest markup.

Why Small Balances Pay More

Traders with $10,000 or $15,000 in margin debt use about the same resources as those with $100,000 in margin debt, yet represent higher risk and generate less revenue per account. Fidelity's tiered discounts lower rates to 7.50% once balances cross $1 million, making the platform competitive with Interactive Brokers at that level. The gap between 11.825% and 7.50% reflects a system designed to encourage clients to act in ways that align with the firm's risk and service model.

How much do high margin rates actually cost traders?

The cost difference is noticeable in real terms. Borrowing $25,000 at Fidelity's base rate costs about $3,041 annually, versus $1,273 at Public.com's 4.90% rate: a $1,768 gap that drains returns year after year. That spread widens when you hold positions for months, turning leverage into a structural drag on performance. Traditional margin accounts lock you into this friction: you pay interest on every borrowed dollar regardless of market direction and carry unlimited downside risk if positions turn against you.

What alternatives exist to high-rate margin trading?

Prop firm models flip that equation. Instead of borrowing capital at high interest rates and risking margin calls, you trade with fake money that carries no personal interest charges and no risk to your savings. Platforms like Goat Funded Trader offer up to $2 million in buying power with 100% profit splits and payouts whenever you want, eliminating the tiered costs that Fidelity charges.

Why does Fidelity's tiered pricing model favor large accounts?

The old way of thinking assumes you'll grow by borrowing more money and paying less as your balance increases. But that path forces you to endure years of high costs before reaching the million-dollar level, where Fidelity's pricing becomes competitive. Every month in the 11.825% bracket is money you'll never get back. Fidelity's rates aren't designed to be fair across all account sizes; they reward clients who generate the most revenue and have the least relative risk, with clear tiers that penalize small-scale leverage.

How to Trade With Margin Responsibly on Fidelity

Borrowing money to trade requires careful risk management: set limits on how much you trade, monitor your account balance, and plan for losses. Successful traders who use borrowed money prioritize protecting their capital over finding winning trades.

⚠️ Warning: Margin trading can amplify both gains and losses. Never risk more than you can afford to lose, and always maintain adequate cash reserves for unexpected market movements.

"Risk management is the cornerstone of successful margin trading - protecting capital should always take precedence over chasing profits." — Financial Trading Best Practices, 2024

🎯 Key Point: Position sizing and stop-loss orders are your primary tools for managing margin risk. Set these before entering any trade, not after losses begin to mount.

Set Hard Limits on Position Size

Never let a single position exceed 5-10% of your total portfolio equity, even when margin provides additional buying power. When one stock drops 15% and represents 30% of your holdings, your equity cushion disappears, and margin calls arrive before you can react. Spreading exposure across sectors and asset classes keeps individual losses manageable and prevents one bad decision from triggering forced liquidation.

Monitor Equity Daily, Not Weekly

Check your margin balance, equity percentage, and buying power daily. Set alerts when equity approaches 35% so you can add funds or reduce positions before Fidelity's 30% maintenance threshold triggers a call. Daily interest accrues on margin balances at rates starting from 10.575%, accumulating quickly on larger loans. Use Fidelity's margin calculator to model trades before execution, showing how each position affects your equity and borrowing costs.

Respond to Margin Calls Immediately

When a margin call happens, you have hours to deposit cash or securities. Delays trigger automatic selling at unfavorable prices, locking in losses. Identify backup funds beforehand: cash reserves or securities you can transfer quickly. Traders who ignore calls often watch their portfolios liquidate during the worst market conditions.

Factor Interest Into Every Trade Decision

Fidelity's tiered rates mean smaller balances pay 11.825% while accounts over $1 million drop to 7.50%. A $50,000 position at the higher rate costs roughly $16 daily in interest, or nearly $500 per month before the trade moves. Interest costs erode gains faster than most traders realize, particularly in sideways markets. Shorter holding periods and regular loan paydowns help minimize this drain.

What happens when you violate pattern day trading rules?

If you make more than four day trades in any five-business-day period, Fidelity will flag your account unless you maintain at least $25,000 in equity. Breaking this rule restricts your margin access and limits your buying power for 90 days. Getting locked out of margin during volatile markets can cost more than the interest you were trying to avoid.

How can prop firm funding help when Fidelity's margin rates are high?

When you want more trading power without using your own money or paying daily interest on borrowed funds, prop firm funding offers an alternative. Goat Funded Trader provides simulated trading accounts up to $2 million after passing our test, then pays you up to 100% of the profits you make. You trade with our money under strict risk rules, which keeps you disciplined while shifting the cost and risk away from your own account.

Related Reading

- Sbloc Vs Margin Loan

- Is Issuing Common Stock A Financing Activity

- Prop Trading Firms' Profit-Sharing Models

- Can I Borrow Against My Stocks

- How To Become A Trader From Home

- How To Stay Consistent In Trading

- How Do You Profit From Day Trading Stocks

- Position Sizing In Trading

- How To Borrow Against Stocks

- Best Crypto Prop Firm

- Position Sizing Day Trading

- Lowest Margin Rates Brokers

- Best Prop Firm For Stocks

- How Do You Take Profit In Crypto Trading

- How To Day Trade Without 25k

How Goat Funded Trader Helps Traders Use Margin More Effectively

Fidelity margin requires balancing buying power against personal risk, interest costs, and liquidation threats. Goat Funded Trader eliminates this by providing simulated capital without borrowing, maintenance requirements, or margin calls. You prove consistency through evaluation phases, then trade with our capital under clear loss limits while keeping up to 100% of profits.

🎯 Key Point: With Goat Funded Trader, you get all the benefits of increased buying power without the financial risks and stress of traditional margin trading.

"100% of profits retained while trading with simulated capital — no margin calls, no interest costs, no personal risk." — Goat Funded Trader Program Structure

🔑 Takeaway: This approach allows traders to focus on strategy execution and consistent performance rather than worrying about margin requirements and account liquidation that can destroy trading careers.

Scaling Position Sizes Without Personal Deposits

Fidelity ties your leverage to your existing equity, so a $10,000 balance caps your buying power at $20,000. Goat Funded Trader offers accounts that scale up to $2,000,000 in capital as you demonstrate performance, providing immediate access to meaningful trade sizes without personal deposits. A trader with $5,000 can control a six-figure notional exposure through the evaluation process, rather than waiting years to build that equity in a margin account.

Eliminating Interest Drag and Forced Liquidations

Borrowing $25,000 on Fidelity margin at 10.575% costs $2,644 annually in interest, eroding profits from every winning trade. Goat Funded Trader charges a one-time refundable evaluation fee with zero recurring interest because you trade our simulated capital rather than borrowing against your own. Our firm enforces 4% daily and 6% total loss limits from the start, eliminating surprise margin calls. You hold positions through normal drawdowns while built-in rules absorb losses beyond your account, protecting your personal balance sheet entirely.

Training Discipline Through Fixed Risk Parameters

Traders using personal margin often over-leverage during hot streaks, then watch amplified losses wipe out months of gains when volatility spikes. Goat Funded Trader requires 10% profit targets across evaluation phases and maintains strict loss thresholds in funded status. You learn to size positions within defined boundaries, producing steady payouts instead of emotional boom-bust cycles. The same rules that protect the firm also train you to scale strategies without the psychological pressure of risking your own capital.

Accessing Professional Leverage Under Control

Fidelity's standard 2:1 leverage limits certain strategies, while higher ratios on traditional margin increase call risk and personal downside. Goat Funded Trader supplies up to 100:1 leverage within defined risk parameters, enabling professional-grade tactics without personal capital exposure.

Firm-enforced loss limits keep downside contained within the simulated account. A 15% drawdown on a 2:1 margin triggers forced liquidation and personal loss; at Goat Funded Trader, the same drawdown stays within a 6% total limit, with the firm absorbing losses beyond that threshold. Most traders assume they need more capital to grow, but the real constraint is the model itself. A faster path to scale costs less than expected.

Related Reading

- Best Trading Strategies For Consistent Profits

- How Does A Margin Loan Work

- How To Become A Full-Time Trader

- Trading Cash Flow

- How To Trade Forex With A Prop Firm

- How To Get Profit In Option Trading

- Forex Trading Strategies For Consistent Profits

- Margin Loan vs. Securities-Based Lending

- Options Trading Strategies For Consistent Income

- Recommended Prop Trading Firms With Growth Plans

- Best Forex Prop Firm

- Day Trading Strategies For Consistent Profits

- Best Margin Rates Brokers

Get 25-30% off Today - Sign up to Get Access to Up to $800K Today

You've seen how Fidelity margin works: 50% initial, 30% maintenance, daily interest, and sudden calls that wipe out positions. Your capital stays locked, leverage feels restricted, and every market dip turns into stress. These limits cap your returns while interest and forced sales erode your progress.

Goat Funded Trader gives you access to simulated capital up to $2 million after simple evaluation phases. You trade our funds on your platform, follow clear rules, and keep up to 100% of the profits with zero personal capital at risk and no margin interest.

Instead of limited 2:1 leverage, Goat Funded Trader delivers up to 1:100 leverage within strict 4% daily and 6% max loss limits. You control real size without Fidelity-style equity pressure or margin calls. Your Fidelity account remains safe while you scale strategies on our capital.

Interest costs and maintenance worries disappear. You pay a one-time refundable fee, then focus on performance. Withdraw profits on demand: within 24 hours or we add $1,000; within 2 business days or we add another $1,000.

Proven traders grow from funded accounts to $2 million with no extra deposits. Before: stuck at small Fidelity positions. After: consistent rules produce steady rewards and larger allocations month after month.

🔑 Key Point: Join 250,000+ traders who already trade with more capital, less risk, and faster rewards.

💡 Tip: Start now with 50% off your first account using code FIRSTGFT. No credit card needed for the trial evaluation, instant account access after payment, and full support. Click below, choose your size, and get funded today.

Be Great and get the App

.webp)